The 2-Minute Version

- 2025 overhauled federal student loans through the One Big Beautiful Bill Act (OBBBA), and most of it takes effect July 1, 2026.

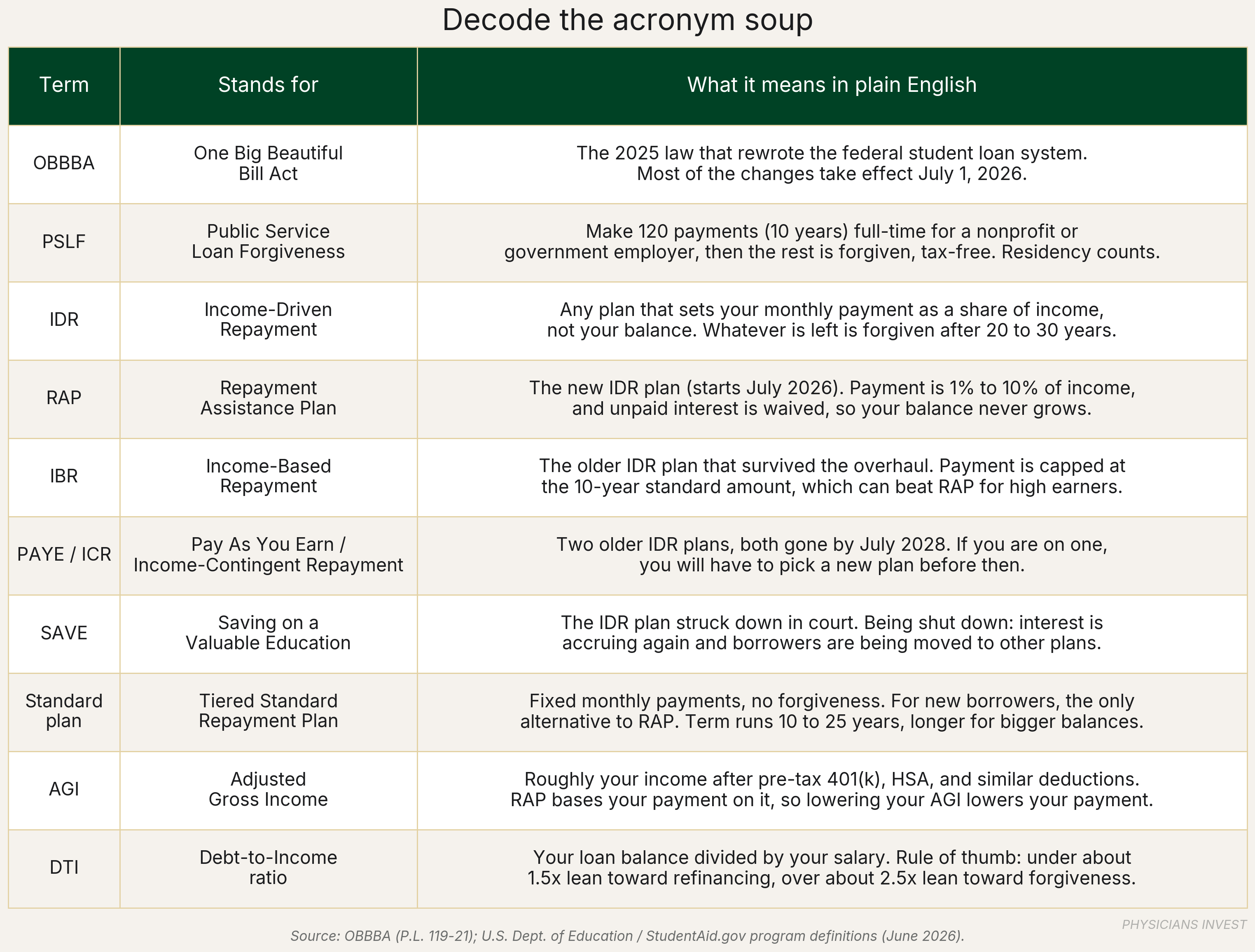

- RAP is the new income-driven plan, while the other income-driven plans are being retired. PSLF is still an option, and residency counts toward it.

- Every physician has a different situation, and unfortunately student loans have no "one-size-fits-all" answer.

The Dollar Math On the new RAP plan, a resident with $300k in loans avoids roughly $24k a year of interest that would otherwise pile onto the balance. Why is this? RAP waives any interest accrual that your payment doesn't cover. Over a four-year residency, that's nearly $100k your balance never grows, money you'd otherwise owe under a plan without RAP's interest waiver.

Almost every physician at some point has had student loans, and the government programs have seemed to only become more complex and bureaucratic over the years. A new system takes effect here in about a week, on July 1, 2026. What do you need to know?

The good news is that most of the changes have reduced decision points for physicians, which we view as a good thing. The bad news is that these changes will require some effort to understand, and those physicians in legacy programs might have some administrative work to do in order to stay in government programs. Before anything else, here's the acronym soup of student loans.

7 Important Student Loan Considerations

-

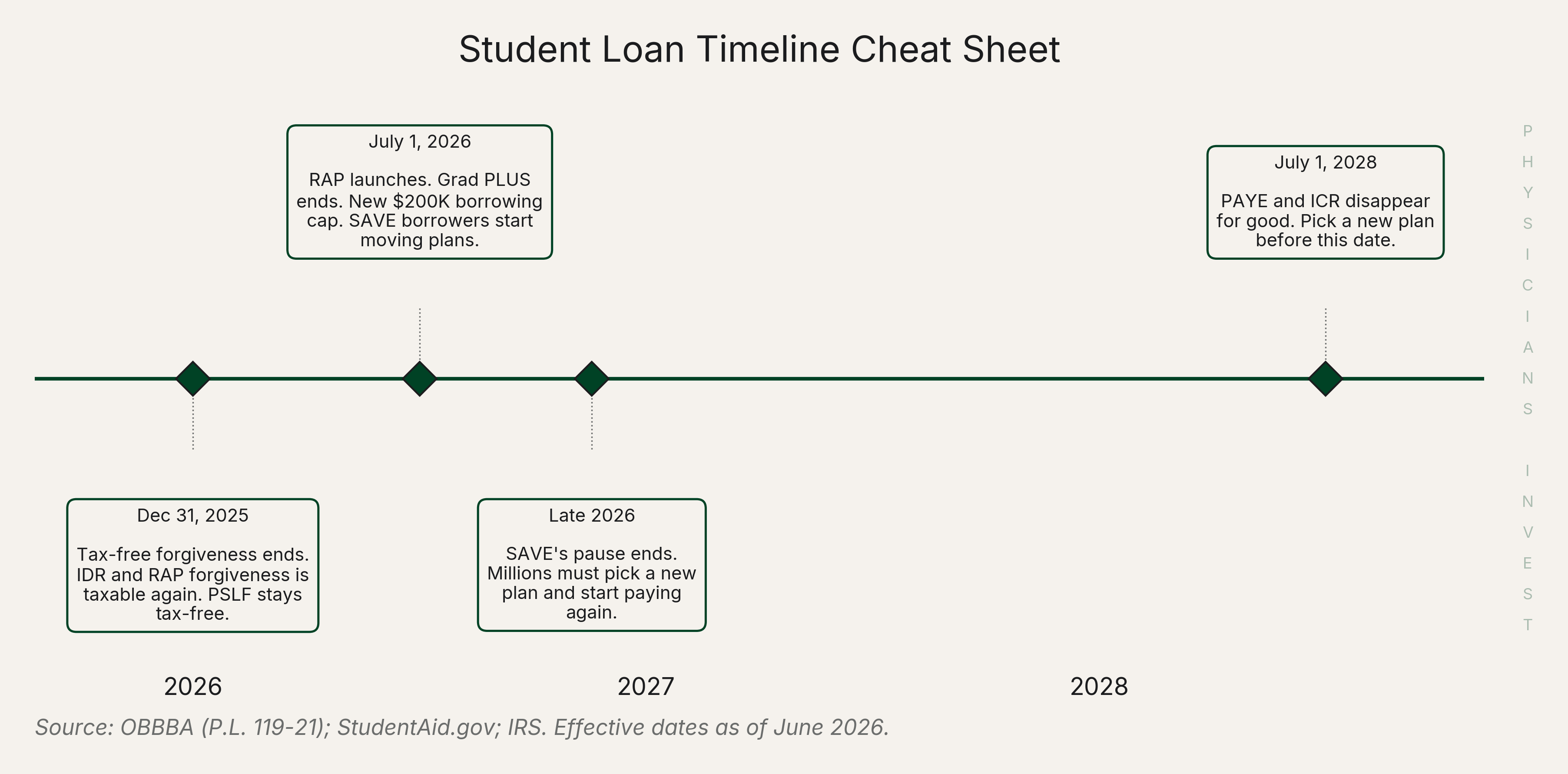

Different rules apply depending on when you took out your loans.

If your loans were granted before July 1, 2026 and you were not on SAVE, you keep access to the older repayment plans...but only up to 2028. If you borrow anything new after July 1, 2026 you lose that access to any and all of the grandfathered plans. The StudentAid.gov OBBBA Updates page has the full breakdown of which plans survive and who qualifies. See the timeline below that shows important student loan dates visually.

-

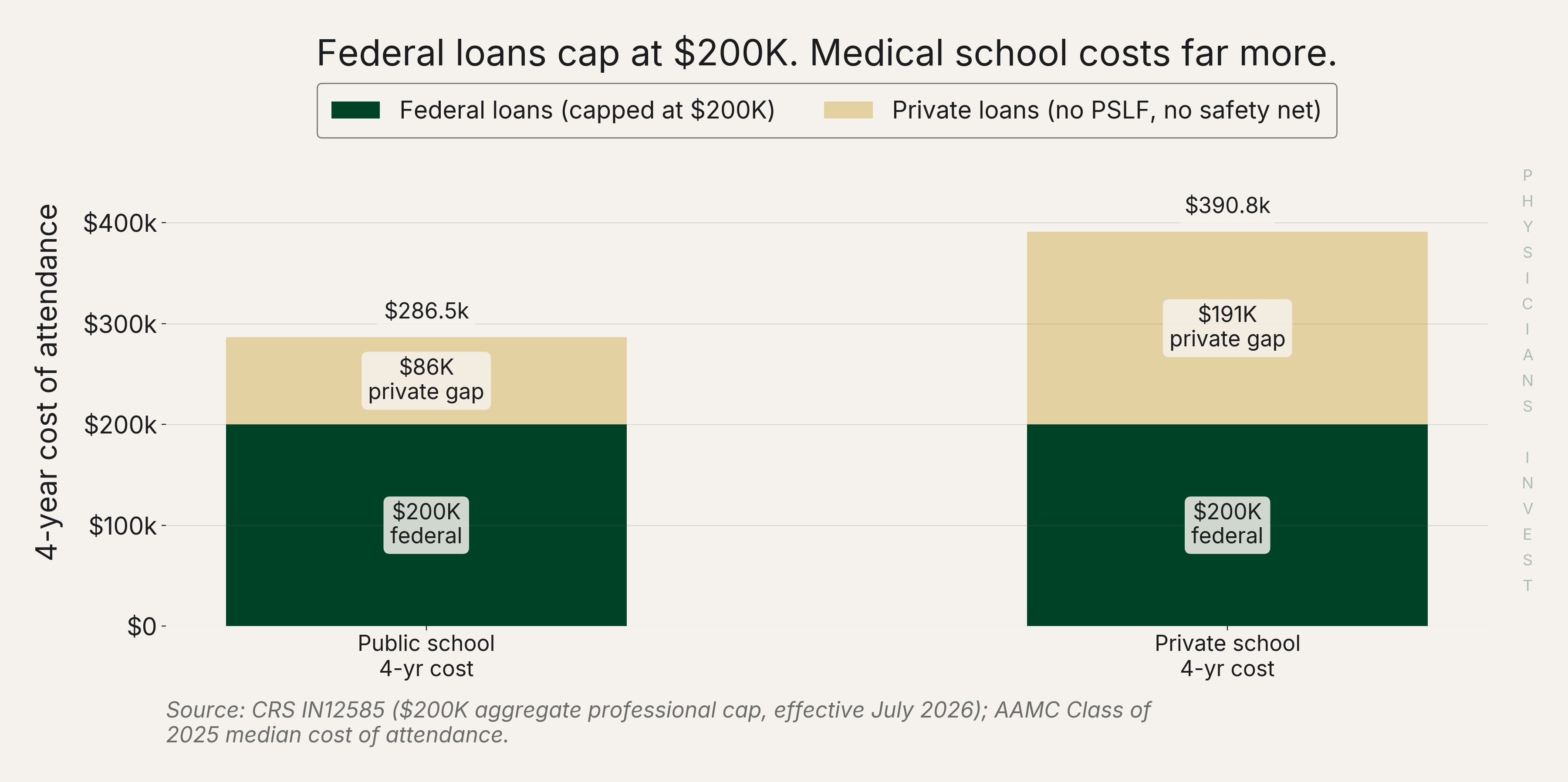

The new federal borrowing cap stops at $200,000.

This is tough news for physicians because the new $200K aggregate cap for professional students (effective for loans first disbursed on or after July 1, 2026) is far less than what most take out to cover all of their education. It forces physicians to use dual lenders: government up to $200k, and then the rest with private lenders. Unfortunately private loans have far fewer protections and perks than you find in the government programs, such as income-based repayment levels. The AAMC Class of 2025 cost-of-attendance data shows median 4-year totals of $286K (public) and $391K (private), and it's easy to see that the government cap of $200k doesn't get there.

-

RAP is the new income-driven plan, and the Standard plan is the only other option for new borrowers. The older plans are sunsetting, and only RAP counts toward PSLF.

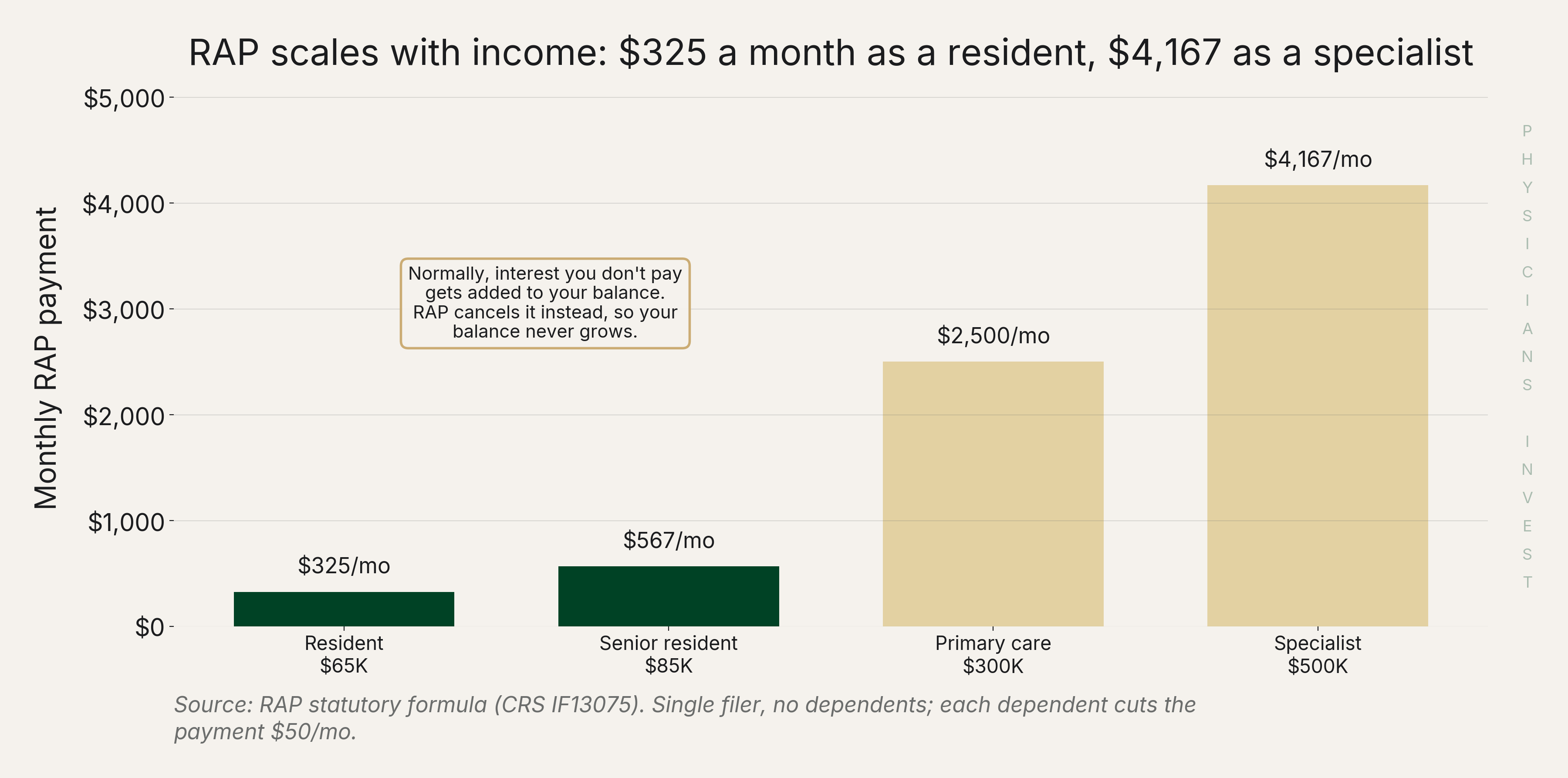

RAP charges 1% to 10% of your income and comes with a very generous perk. It waives the interest your payment doesn't cover, which is great for residents, where the payment often doesn't cover all of their accrued interest. In that situation, the excess interest is waived and never needs to be paid back. The downside of this plan compared to some of those that were sunset is that it has no payment cap. This means a high-earning attending can pay more under RAP than they would've under the older plans. The chart below illustrates how RAP payments vary over a physician's career.

The alternative to RAP is the "Standard plan": it looks more like a traditional fixed-term loan than a government program. Per the NASFAA repayment plan overview, it has fixed payments over 25 years for anyone who owes six figures or more (i.e., most physicians). One important catch: payments on the Standard plan don't count toward PSLF, so if forgiveness is your goal, RAP is the only road.

-

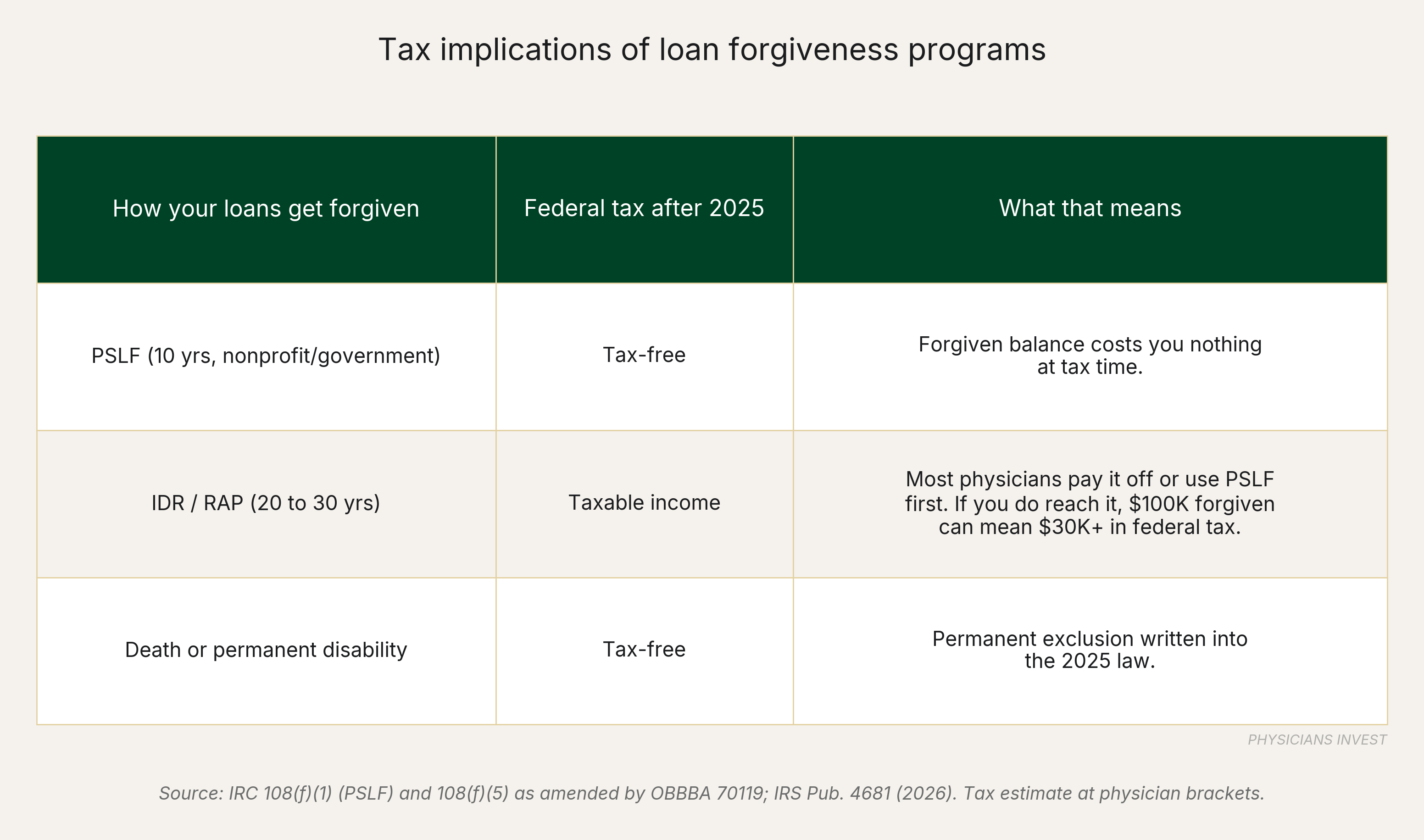

PSLF is still alive and well and residency still counts towards the 10 years.

PSLF requires ten years of payments while working full-time at a nonprofit or government employer. If the 120 qualifying payments are completed (10 years) the remaining balance on the loan is forgiven and is tax-free. Some online sources have mentioned that residency no longer counts toward those ten years with the new bill. That's incorrect. The removal of residency was in the original draft of the OBBBA but got stripped from the final version. Great news. The AAMC documents that the residency exclusion lived only in the House and Senate proposals, not the enacted law. PSLF is still one of the best deals in medicine but you give up optionality to work in the private sector for your first 10 years out of school. More on that in the next bullet.

-

PSLF is also golden handcuffs.

Locking into PSLF means you must stay at a qualifying employer for a decade. If a private-practice or ownership opportunity opens up in year 6, you may not take it because walking away costs you the forgiveness. The forgiveness isn't "free" if it quietly traps you in the wrong job and causes you opportunity cost (the value of the career path you didn't take). This is why we always emphasize that every decision is a calculation and a trade-off when it comes to student loans. There is often not a perfectly clear right answer.

-

PSLF forgiveness remains tax-free. Other forms of loan forgiveness are now taxed.

If a remaining balance is forgiven on a loan, it used to be that it was never taxed. For instance, a physician with $60k forgiven at an illustrative 30% marginal rate (your actual tax depends on your bracket and state) would owe roughly $18k in tax if that provision didn't exist. PSLF was at risk of having its tax-free status stripped. Fortunately, PSLF forgiveness remains tax-free under IRC §108(f)(1), which is a huge win for physicians on the program. Other programs weren't as lucky. The OBBBA §70119 replaced the broad ARPA tax exclusion with a narrower death/disability-only carve-out, meaning IDR and RAP 30-year forgiveness are now taxable as ordinary income. The IRS Taxpayer Advocate confirmed this change as of March 2026. In practice, though, most physicians never face this bill: high earners pay the loan off before any forgiveness kicks in, and nonprofit physicians use PSLF anyway.

- If you're not chasing PSLF, RAP during residency followed by a private refinance is a strategy worth understanding. Here's the logic. While your income is low, RAP's unpaid-interest waiver freezes your balance, and it sets your payment off last year's income, so your first attending year still counts as a resident. Graduate loan interest rates run 7.94% in 2025-26 and 8.07% in 2026-27, so without that subsidy a $300K balance accrues roughly $24K per year in interest during residency. Then, once you're earning attending-level income, refinancing to a private lender can capture a lower rate. You'd be using the government's interest subsidy while your income is low, then shopping private-market rates once it isn't. The catch: refinancing ends any shot at PSLF, so whether this trade-off makes sense depends on your balance, the rate environment, and whether forgiveness was ever your route.

The Move

Student loan decisions are highly nuanced for physicians. Two questions do a decent job of sorting out most of it:

- What career path are you likely to follow? That decides whether PSLF is even on the table. If nonprofit or government, PSLF can make a lot of sense. But you're locked out of private practice for a decade.

- What financial backstop do you have currently? Savings, a high-earning spouse, inherited assets to fall back on, or nothing. Carrying high-interest debt is a very different bet depending on the answer.

For many physicians, the federal programs are genuinely great, especially in the lean early years. Private lenders can be a great option too, though, in the right situations.

The landscape changed fast, and it's worth spending time on before July 1. Two things are especially worth understanding: which side of the July 1 line your loans fall on, and whether PSLF is realistically on the table for you. Refinancing federal loans ends PSLF eligibility permanently, so it's worth sorting that out first. If you want a second set of eyes, we're here to help. We built a student loan flowchart and decision tree for exactly this, available on our website, and we're always around to talk it through.

Sources

Policy

- One Big Beautiful Bill Act, Public Law 119-21 -- governing statute; signed July 4, 2025; source for all OBBBA-driven changes

- CRS IN12585 -- OBBBA student loan provisions -- new $200K professional borrowing cap, Grad PLUS elimination, lifetime limits (July 10, 2025)

- CRS IF13075 -- The Repayment Assistance Plan (RAP) -- RAP formula, unpaid-interest waiver, $50/month principal match, 30-year forgiveness

- ED RISE §685.209 -- RAP regulatory text -- income-driven repayment mechanics (November 6, 2025)

- StudentAid.gov -- OBBBA Updates -- legacy vs. new borrower line, plan access rules (updated June 12, 2026)

- StudentAid.gov -- IDR Court Actions -- SAVE termination, PAYE/ICR sunset timeline (updated March 27, 2026)

- NASFAA -- OB3 Tiered Standard Repayment Plan chart -- Tiered Standard term tiers by balance (2026)

- ED -- PSLF Final Rule press release -- PSLF employer-restriction rule, effective July 1, 2026 (October 31, 2025)

- EO 14235 -- Restoring PSLF (90 FR 11885) -- executive order directing PSLF employer-restriction rulemaking (March 12, 2025)

- 26 U.S.C. §108 -- Cornell LII -- PSLF tax-free status under §108(f)(1); IDR forgiveness taxability after OBBBA §70119

- IRS Publication 4681 -- cancelled debt and forgiveness income rules

- IRS Taxpayer Advocate -- student loan forgiveness and taxes -- tax bomb guidance, March 2026

- FSA Dear Colleague Letter 2025-07-18 -- OBBBA provisions effective on enactment

Data

- AAMC -- Debt, Costs, and Loan Repayment Fact Card, Class of 2024 -- median physician debt, % carrying debt, % owing $300K+

- AAMC -- Proposed changes to federal student loans could worsen the doctor shortage -- Class of 2025 cost-of-attendance: $286K public / $391K private; 63%/88% PSLF planning statistics

- FSA -- Interest rates 2026-27 -- graduate loan rate 8.07% for 2026-27

- FSA -- Interest rates 2025-26 -- graduate loan rate 7.94% for 2025-26

- StudentAid.gov -- PSLF Data Center -- $87.6B discharged, 1,183,600 borrowers, $74,100 average balance forgiven (through September 30, 2025)

Related from Physicians Invest