The 2-Minute Version

- Physicians simultaneously face seven structural financial disadvantages: late start, massive debt, compressed earning window, no bonus structure, lawsuit exposure, burnout risk, and being targeted while financially underexposed.

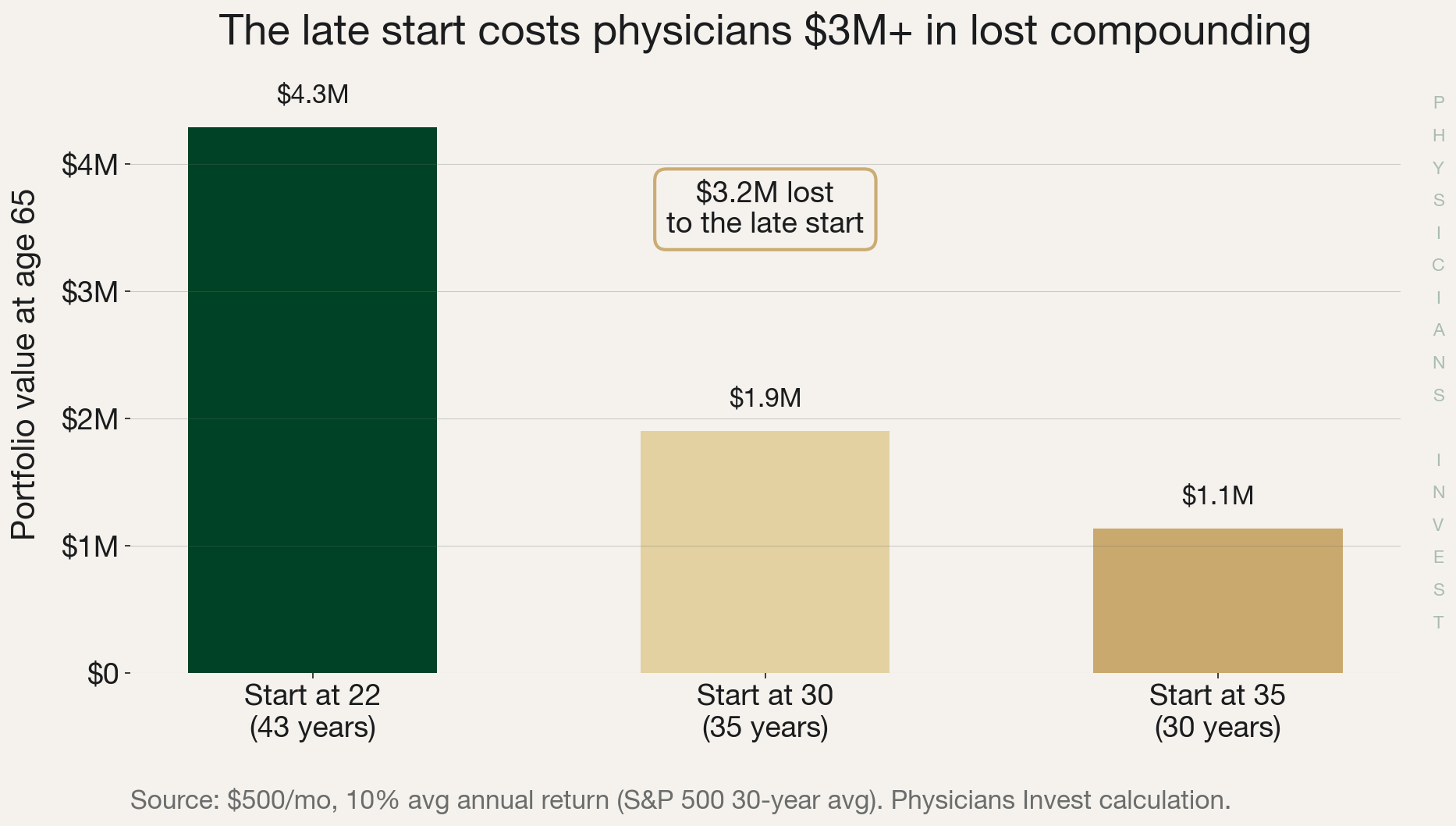

- The compounding cost of starting 13 years late is $3.2 million in wealth that was never created.

- Close the gap with savings rate early, sound investments late, and a self-directed bonus structure that replaces the equity compensation physicians don't get.

$215,000 in debt. A decade of training. And a financial services industry that sees you coming from a mile away.

You trade your twenties (and most of your thirties) for a career that eventually pays well. But "eventually pays well" hides a set of structural financial disadvantages that no other profession faces. Nobody gets hit with all seven of these at once except for physicians.

1. The Late Start

Your college roommate who went into tech has been investing since age 22. You won't make an attending salary until 30 at the earliest. A neurosurgeon? Try 37. That gap isn't just lost income, but more importantly, lost compounding. And compound interest is exponential, not linear.

The math: $500 a month invested at 10% from age 22 grows to $4.3 million by 65. Start at 35? $1.1 million. That's $3.2 million in wealth that was never created.

2. Massive Student Debt (and It's Getting Worse)

Median medical school debt for the Class of 2025 is $215,000. Federal loan rates are running at 7.94% for Direct Unsubsidized and 8.94% for Grad PLUS. And the new federal caps on student loans? The lifetime cap of $200,000 is below the current average medical school debt. Future physicians will be pushed into private loans with fewer protections and higher rates.

3. The Compressed Earning Window

A family medicine physician gets 35 high-earning years. A neurosurgeon gets 27. Your engineering friend gets 43. Fewer years to compound means you need a higher savings rate to reach the same destination. The goal: build an equivalent base as quickly as possible, so compounding works for you instead of against you.

4. The Bonus Problem

Most careers have bonuses built into the pay structure. In tech, it's stock. In law, it's partnership equity. Those bonuses become the savings vehicle. Lifestyle creeps up to your bi-weekly paycheck. That happens to everyone. But in other careers, the bonus is what gets invested.

Physicians don't have that structure. So you need to build your own. Set up a separate account that gets funded automatically every pay period. Don't touch it. At the end of each year, invest the entire balance. That's your self-directed bonus.

5. Lawsuit and Liability Exposure

31% of all physicians get sued during their career. For OB/GYNs, it's 62%. By age 65, 99% of high-risk specialists will have faced a claim. Malpractice premiums run anywhere from $4,000 a year (psychiatry) to $66,000 (OB/GYN in Florida). Very few other professionals carry this kind of liability.

6. Burnout and Career Uncertainty

49% of physicians report burnout. 68% are looking for an employment change or considering early retirement. When over a third of burned-out primary care physicians plan to stop seeing patients within three years, that's not just a wellness issue. That's a financial planning earthquake.

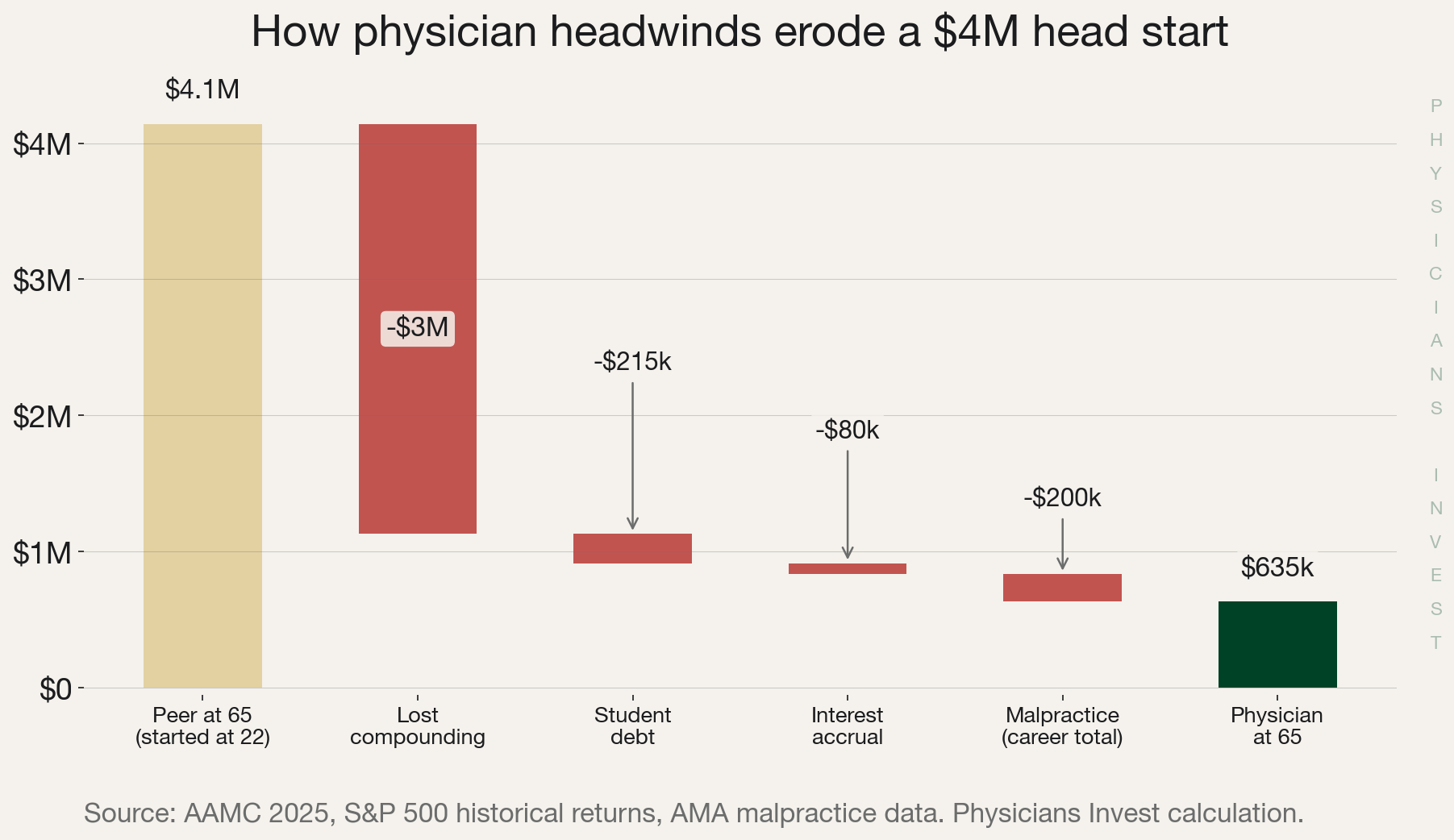

Early retirement at 55 instead of 65 means roughly $3.7 million in foregone gross earnings.

7. Targeted While Financially Underexposed

Physicians aren't financially illiterate. That's the wrong word. They understand the language of finance. What they lack is repetitions. The nuance that only comes from structured exposure to the industry. (Many financial professionals don't take the time to speak to these nuances, which is why physicians are consistently underwhelmed with their financial advisor.)

High income, high debt, accredited investor status, and limited time for due diligence. The bad actors are the ones who sound more compelling on the front end, because they aren't following the SEC rules that prevent overselling. 75% of physicians who buy whole life insurance regret it. The actually good alternatives (institutional-caliber VC, PE, hedge funds, commercial real estate) require a network most physicians don't have access to. Yet.

No Other Profession Faces All Seven

| Headwind | Physicians | Lawyers | Engineers | MBAs |

|---|---|---|---|---|

| Late start (10+ years training) | Yes | No | No | No |

| $200K+ student debt | Yes | Partial | No | Partial |

| Compressed earning window | Yes | No | No | No |

| No bonus/equity savings vehicle | Yes | Partial | No | No |

| Malpractice/lawsuit exposure | Yes | Partial | No | No |

| 49% burnout, 68% considering change | Yes | No | No | No |

| Targeted while underexposed | Yes | No | No | No |

| Total | 7 of 7 | 2 partial | 0 | 1 partial |

The Move

Early in your career, the best way to close the gap is through your savings rate. Not your investments. Late in your career, the best way to stay ahead is by making sound investments that compound the base you've built.

- Build the structure first. Automate savings, debt payments, and retirement contributions so they happen without you thinking about them. (This was the one-word answer when we asked what matters most in year one.)

- Create your own bonus. Set up a separate account that gets funded every pay period. Invest the full balance annually, ideally in an investment that gives you high upside and equity ownership.

- Prioritize savings rate early, investment quality later. Once you hit certain net worth hurdles, shift focus to sound long-term investments. Until then, you make up the compounding gap by saving more, not by chasing higher returns in risky vehicles.

- Get to base as fast as possible. The first $500K is the hardest. After that, compounding starts to work with you instead of against you.

- Be skeptical of anyone pitching you anything. If the investment sounds too compelling, ask why the SEC allows them to market it that way. (They probably don't.)

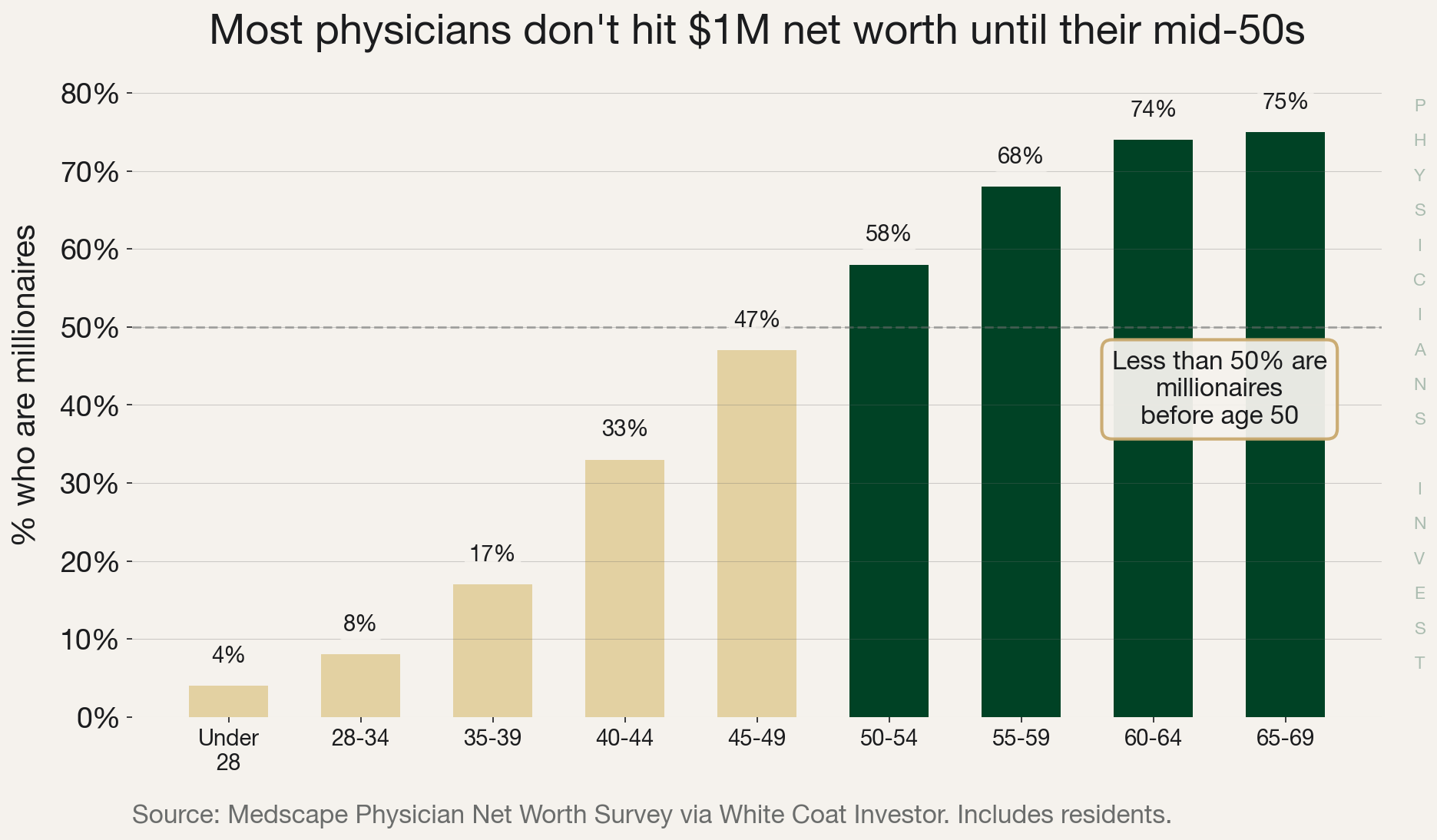

Less than 50% of physicians are millionaires before age 50. That number should be closer to 90%. That's the seven headwinds doing their work. But they're headwinds, not brick walls. The physicians who build the right structure early are the ones who break through.

Sources

Data

- AAMC Physician Education Debt Report, Class of 2025

- Federal Student Loan Interest Rates 2025-26

- Washington University Residency Length by Specialty

- S&P 500 Historical Returns

- White Coat Investor: Physician Millionaires

- Average Cost of Malpractice Insurance by Specialty

Analysis

- AMA: One in Three Physicians Previously Sued

- NEJM: Claims, Errors, and Compensation in Malpractice Litigation

- Medscape 2025 Physician Compensation Report

- Doximity 2025 Physician Compensation Report

- Commonwealth Fund: Burned-Out Primary Care Physicians

- White Coat Investor: Whole Life Insurance

Policy