The 2-Minute Version

- SAVE is dead. Grad PLUS loans disappear July 1. A new plan (RAP) launches with no payment cap. All at once.

- If you're in SAVE forbearance, you're losing PSLF credit every month. Consider moving to IBR.

- PSLF math still works for high-debt physicians. But for moderate debt loads, the juice might not be worth the squeeze.

We know a physician couple who spent five years organizing their lives around PSLF. She stayed at qualifying organizations. They kept their eyes closed to other opportunities, including private practice roles that could have built real equity. The final savings after all that? About $30,000.

That's not nothing. But for five years of stress, location lock-in, and closed doors, it's worth asking: was it worth it?

Three Things Changed at Once

SAVE is gone. The plan that covered 7.6 million borrowers got halted by the courts in February 2025, then killed for good by the One Big Beautiful Bill Act last July. If you're still in SAVE forbearance, your interest started accruing again in August 2025. And those forbearance months? They don't count toward PSLF.

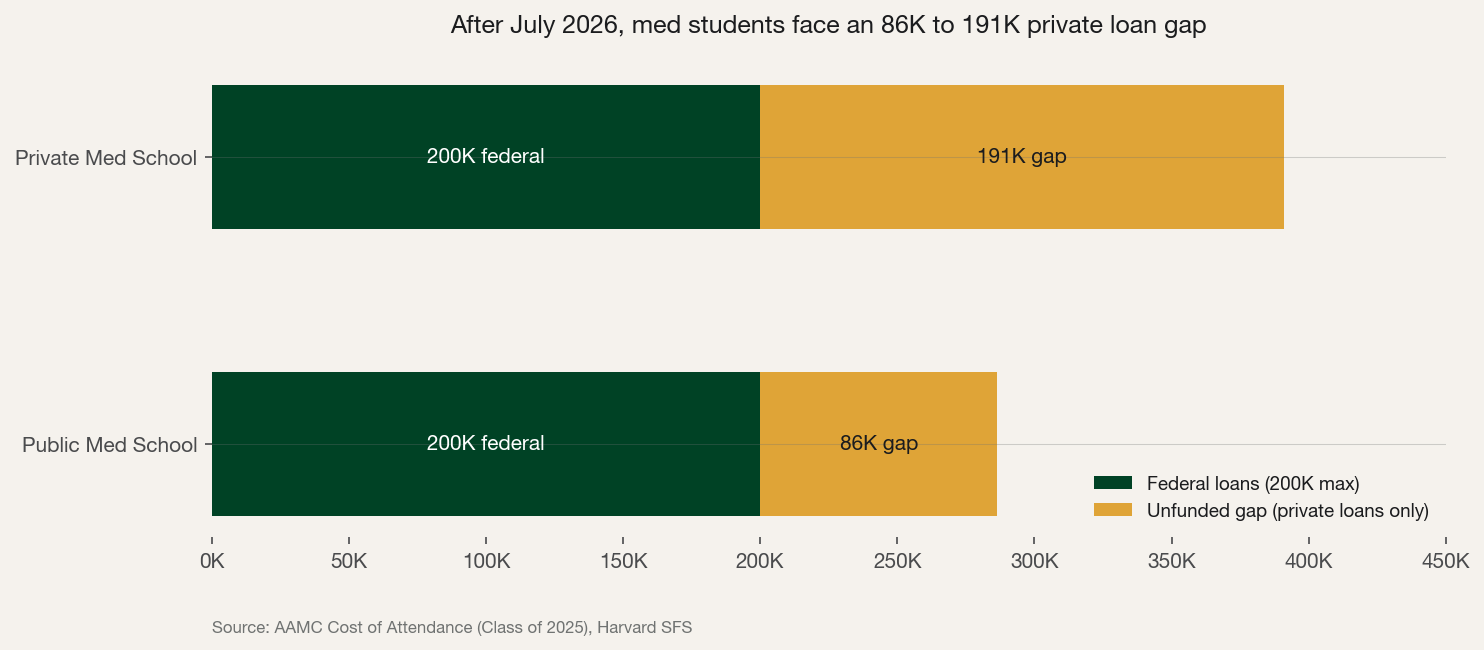

Grad PLUS loans vanish July 1, 2026. No new Grad PLUS for first-time borrowers. The new federal cap is $200,000 lifetime for professional students. The median four-year cost of a public medical school is $286,454 (private: $390,848). That gap ($86K to $191K) shifts entirely to private lenders. No income-driven repayment. No PSLF eligibility. Nothing.

Source: AAMC Cost of Attendance Data (Class of 2025), Harvard SFS

Source: AAMC Cost of Attendance Data (Class of 2025), Harvard SFS

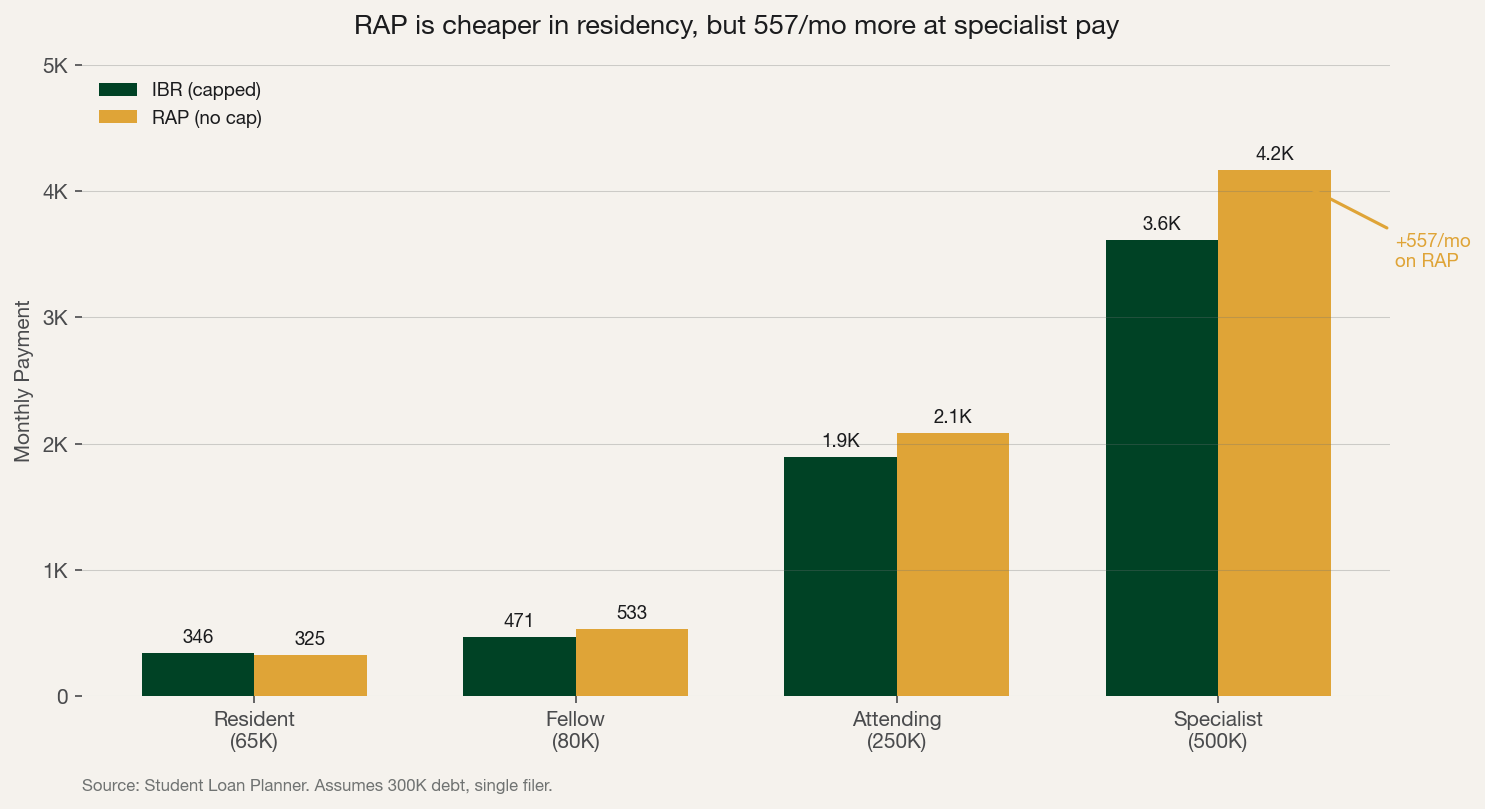

RAP replaces everything. The new Repayment Assistance Plan launches July 1, 2026. It uses your total AGI (not discretionary income like IBR) and has no payment cap. A PGY-2 earning $65K pays $325/month on RAP versus $346 on IBR. Cheaper in training. But the moment attending income hits, the math flips. A specialist earning $500K pays $4,167/month on RAP. On IBR, that same physician is capped at $3,610. Over 10 PSLF years, that's $66,840 more out of pocket on RAP.

Source: Student Loan Planner RAP Calculator, College Investor

Source: Student Loan Planner RAP Calculator, College Investor

And here's the trap: if you're a pre-July-2026 borrower and you take out a single new federal loan after July 2026, you lose IBR access on ALL your loans. Forced onto RAP. (Yes, one loan. One.)

The Real Cost of PSLF

We think PSLF still makes sense for physicians with massive debt loads at academic medical centers. If you owe $350K and you're going to spend your career at a nonprofit hospital anyway, the math works.

But the conventional wisdom overrates it. Nobody talks about what PSLF costs beyond the dollars. The indecision the government has shown over five years of policy whiplash. Three website migrations. Buying back forbearance months you thought counted. Being locked into organizations that might not be the best fit for your family.

Everything has a cost. Some costs are monetary. Some sit at the back of your mind and never fully go away. There's real value in clearing up that brain space. (Ask anyone who's paid off their loans in full.)

For physicians with moderate debt (under $150K), think bigger than being myopically focused on debt forgiveness. If the total PSLF savings is $30K to $50K over a decade of hassle, that might not be worth it. Especially when private refinancing rates for physicians run 4.12% to 4.49% as of early 2026, versus the federal rate of 7.94%.

What to Do This Week

If you're in SAVE forbearance and pursuing PSLF: We'd get out. Consider switching to IBR at studentaid.gov/idr. Every month in forbearance is a month that doesn't count toward your 10-year clock.

If you're a pre-July-2026 borrower: Be very careful about taking a new federal loan after July 2026. One new loan pushes all your debt onto RAP permanently. The deadline to enroll in IBR and preserve access is July 1, 2028.

If you're choosing between PSLF and refinancing: Factor in the non-monetary costs. The freedom to take the job that fits your family instead of the one that fits your loan strategy. The mental bandwidth you get back when you're not tracking rule changes every quarter.

If you're starting med school after July 2026: Federal loans cap at $200K lifetime. The rest is private. Seriously consider the cost gap between a $286K public school and a $391K private school, because that gap now lands directly on your shoulders.

Sources

Policy

- FSA Dear Colleague Letter: OBBBA Provisions

- Harvard SFS: Key Changes to Federal Student Loans

- Congress.gov CRS: Repayment Assistance Plan (RAP)

- Ed.gov: Agreement to End SAVE Plan

- StudentAid.gov: PSLF Buyback

Data

- AAMC: Proposed Changes Could Worsen Doctor Shortage

- FSA: Interest Rates for Direct Loans 2025-2026

- Student Loan Planner: RAP for Medical Residents

Analysis