The 2-Minute Version

- 57.5% of physicians are W-2 employees. The tax playbook for you is different than what most content covers.

- The One Big Beautiful Bill Act changed the game for 2026: SALT cap quadrupled, HSA eligibility expanded, Dependent Care FSA increased.

- The Pareto principle applies: 20% of the tax work (maxing your accounts) gets you 80% of the benefit. Start there.

You just finished your first year as an attending. You're making $350K. Your W-2 lands in January, and the federal tax line makes you physically uncomfortable. You Google "tax deductions for physicians" and every article says the same thing: start a side gig, form an LLC, get a micro-corporation.

That advice isn't wrong. But nobody mentions the overhead. The administrative burden. The huge amount of time and detail required to do it correctly. Most physicians don't have the time or headspace for it.

Here's what nobody tells you: 57.5% of physicians are now W-2 employees, per the AMA's 2024 Practice Benchmark Survey. That number has been climbing about 1.3 percentage points per year since 2012. The tax playbook for a pure W-2 physician is not "limited." It's just different.

What Changed in 2026

The One Big Beautiful Bill Act, signed in July 2025, made several permanent changes that matter this year:

SALT (state and local tax) cap quadrupled. The state and local tax deduction cap jumped from $10,000 to $40,400. If you're a cardiologist in Manhattan or a hospitalist in San Francisco, this is the single biggest dollar-impact change. One catch: the cap phases down starting at $505,000 MAGI. Above $600K, you're back to the old $10K cap.

One thing to know: SALT is an itemized deduction. It only helps if your total itemized deductions exceed the standard deduction of $32,200 for married filing jointly in 2026. For physicians in high-tax states, the increased SALT cap alone may push you well past that threshold. In no-income-tax states like Texas or Florida, you can elect to deduct sales tax instead of income tax. Between property tax and sales tax, many physicians in these states can still build a meaningful SALT deduction.

Higher-earning subspecialists in dual-income households? Many will be phased out. The rules are the rules.

| State | State + Local Tax Paid | Old Cap | New Cap (2026) | Extra Deduction | Federal Tax Savings |

|---|---|---|---|---|---|

| California | ~$30,000 | $10,000 | $30,000 | $20,000 | ~$6,400 |

| New Jersey | ~$28,000 | $10,000 | $28,000 | $18,000 | ~$5,760 |

| New York | ~$26,000 | $10,000 | $26,000 | $16,000 | ~$5,120 |

| Illinois | ~$24,000 | $10,000 | $24,000 | $14,000 | ~$4,480 |

| Texas | ~$8,000 | $8,000 | $8,000 | $0 | $0 |

| Florida | ~$8,000 | $8,000 | $8,000 | $0 | $0 |

"State + Local Tax Paid" includes income tax + property tax. For TX/FL, it's property tax only (from your Form 1098 or county tax bill). The cap phases down at $505K MAGI.

Other OBBBA changes worth knowing:

- HSA eligibility expanded. Bronze plans and Direct Primary Care arrangements are now HSA-compatible.

- Dependent Care FSA increased from $5,000 to $7,500 (if you have kids under 13).

- Employer student loan repayment made permanent at $5,250/year tax-free. Ask your HR if they offer it.

- Charitable deduction now has a 0.5% AGI floor. At $400K income, the first $2,000 of giving produces zero tax benefit. Bunching via a donor-advised fund matters more than ever.

One SECURE 2.0 change catching people off guard: If you're over 50 and earned more than $150,000 in FICA wages, your catch-up contributions to your 401(k) or 403(b) must be Roth. Not optional.

The 80/20 of W-2 Physician Taxes

The Pareto principle applies here. About 20% of the tax work gets you about 80% of the benefits when you just focus on the vehicles.

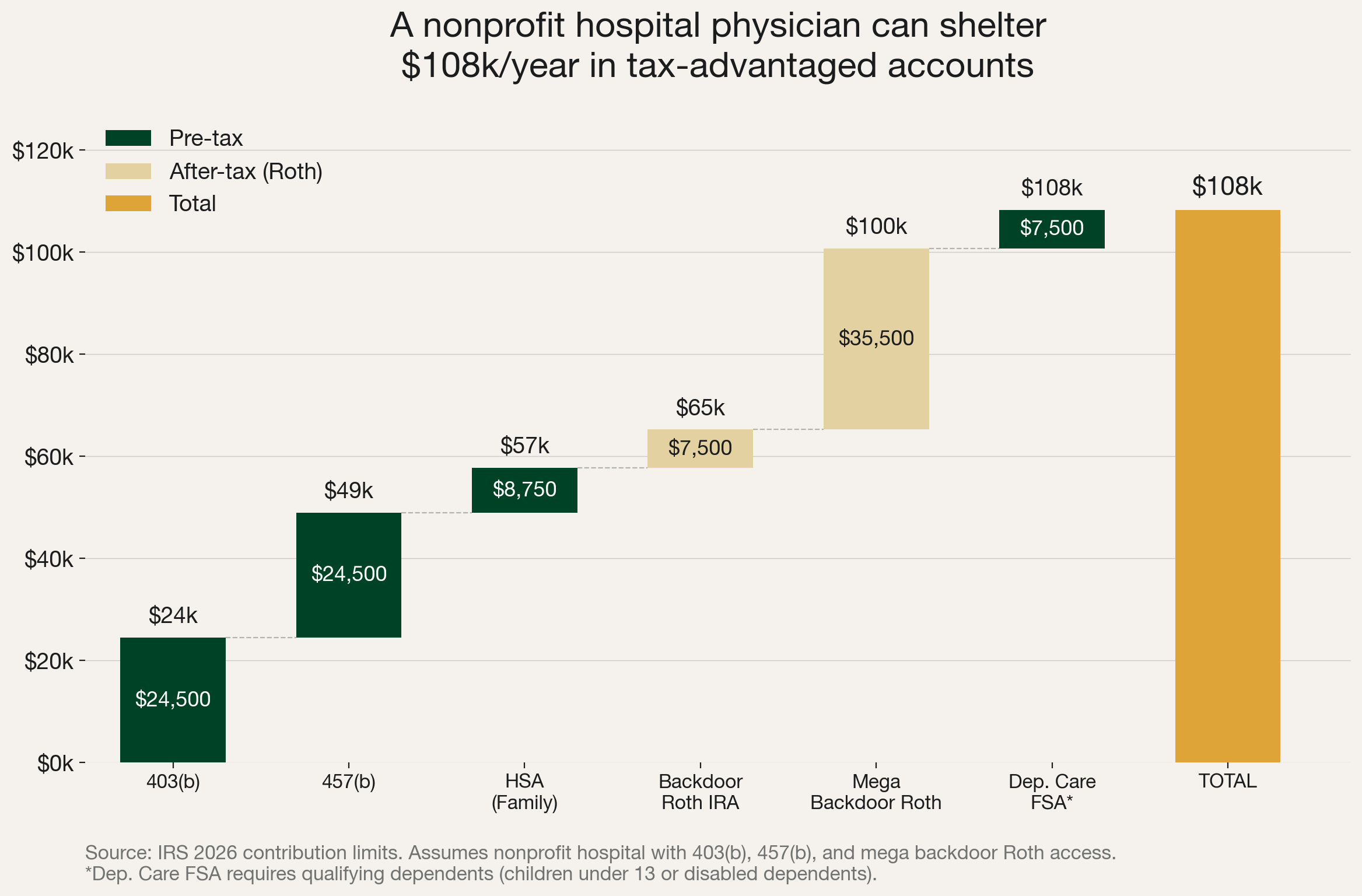

2026 annual contribution limits:

| Account | 2025 Limit | 2026 Limit | Change |

|---|---|---|---|

| 401(k) / 403(b) | $23,500 | $24,500 | +$1,000 |

| 457(b) (nonprofit hospital) | $23,500 | $24,500 | +$1,000 |

| IRA (traditional + Roth combined) | $7,000 | $7,500 | +$500 |

| HSA (family) | $8,550 | $8,750 | +$200 |

| HSA (individual) | $4,300 | $4,400 | +$100 |

| 401(k)/403(b) catch-up (age 50+) | $7,500 | $8,000 | +$500 |

| 401(k)/403(b) super catch-up (age 60-63) | $11,250 | $11,250 | No change |

| Dependent Care FSA (requires qualifying dependents) | $5,000 | $7,500 | +$2,500 |

The IRA limit is the combined total across traditional and Roth. Catch-up amounts are in addition to the base 401(k)/403(b) limit.

Most physicians don't max out all available retirement accounts. That's the single biggest tax mistake we see. The IRA is the one that often gets dropped.

The Moves Most W-2 Physicians Miss

If you work at a nonprofit hospital, you might have access to a 457(b) plan. The 457(b) limit does NOT share a cap with your 403(b). That means you can defer $24,500 into your 403(b) AND another $24,500 into a 457(b). That's $49,000 in pre-tax space before you touch any other account.

Most physicians don't know the 457(b) exists because HR doesn't proactively offer it. Ask.

(One caveat: non-governmental 457(b) plans are unsecured deferred compensation. If your hospital goes bankrupt, you're an unsecured creditor. The size of the organization matters. A major academic medical center carries less risk than a smaller regional hospital. But even large systems aren't immune.)

If your employer's plan allows after-tax contributions with in-plan Roth conversions, you can do a mega backdoor Roth. This uses after-tax dollars. You won't get a tax deduction today. But once the money is converted to Roth, all future growth is tax-free forever. At $35,500 per year for 20 years at 7% growth, that's roughly $1.5M in gains that will never be taxed. The question to ask HR: "Does our plan allow after-tax contributions with in-plan Roth conversions?" One question. Potentially decades of tax-free growth.

Your Investments Are a Tax Decision Too

Here's what gets overlooked in every W-2 tax article: when you can't write off much as a W-2 employee, what happens inside your portfolio matters even more.

Yes, the tax annually hurts from a high W-2 job. But you shouldn't add to that by making your investments unnecessarily tax-heavy.

Once your taxable portfolio crosses $500K or so, the tax drag from high-yield savings, bond funds, and REITs throwing off ordinary income starts adding up fast. A few things we think about:

Long-term buy and hold of index ETFs is still the simplest tax play for taxable accounts. Hold them forever and you never pay capital gains tax on the unrealized appreciation.

Stop buying and selling individual stocks. Every time you sell and rotate into something new, you trigger a taxable event. The physician who buys a total market index ETF and never touches it will almost certainly end up with more after-tax wealth than the physician who's actively picking stocks, even with similar pre-tax returns. Options trading is even worse.

Be skeptical of direct indexing. The pitch sounds great: S&P 500 exposure with tax-loss harvesting on every losing stock. It works for a couple of years. Then all the losing stocks have been sold, there's nothing left to harvest, and getting out means selling hundreds of positions at a massive tax hit. The exit cost can exceed what you saved. Sometimes boring is better.

Tax-loss harvesting is real but don't chase it. We've seen too many physicians end up in mediocre strategies because someone sold them on the tax savings. The savings don't matter if the underlying investment underperforms.

Series I bonds are more interesting than a bond ETF for after-tax money. All interest deferred until redemption. $10,000 per person per year. (Not exciting, but quietly effective.)

Advanced Strategies (With Heavy Caveats)

Oil and gas working interest can offset ordinary income (not just passive income). But the risk is very high. Your source of advice should not be the person who is selling the investment.

Real Estate Professional Status (REPS) can allow rental property losses to offset W-2 income, but it requires a spouse who genuinely meets the 750-hour and material participation tests. We'll do a deep dive on REPS in a future issue.

These are not starter moves.

The Move

If you're a new attending, three tax moves, in order:

1. Max your tax-advantaged accounts. 401(k) or 403(b), IRA, HSA if you're on a high-deductible health plan (deductible of at least $1,700 individual or $3,400 family in 2026). If your employer offers a 457(b), add that too. This is where the 80/20 rule lives.

2. Invest tax-smart. Buy and hold index ETFs. Avoid stacking ordinary-income-generating investments in taxable accounts.

3. Know your deductions. The SALT cap increase alone could save you $4,000 to $6,400 if you're in a high-tax state. You don't need a sophisticated CPA for most of this.

And if you're doing nothing else: just max your retirement accounts. That one move, consistently, accounts for the vast majority of the tax benefit available to you.

Sources

Government / Regulatory

- IRS: One Big Beautiful Bill Provisions

- IRS: 2026 Contribution Limits

- IRS: Roth Catch-Up Rule Final Regulations

- IRS: HSA Guidance Under OBBBA

- TreasuryDirect: Series I Savings Bonds

Analysis

- Bipartisan Policy Center: SALT Deduction Changes

- Tax Foundation: Charitable Deduction Changes

- Tax Foundation: 2026 Tax Brackets

Data