The 2-Minute Version

- Trump Accounts are new tax-advantaged savings accounts for children. Contributions open July 4, 2026. If your child was born 2025-2028, the government puts in $1,000 free.

- The account has a fatal flaw: without a Roth conversion at age 18, withdrawals get taxed as ordinary income (up to 37%). With the conversion, it becomes tax-free for life. That conversion is THE move.

- Open one now. File Form 4547 at form.trumpaccounts.gov. It takes five minutes.

A couple of years ago, Brad Gerstner (founder of Altimeter Capital, a tech-focused investment firm) pitched an idea that stuck with us: most Americans are "renters" in this economy. They work, they spend, they pay taxes. But they don't own equity. And when you don't own assets aligned with the country's future, you stop caring about that future. His solution was to give every American child a stake in the market from birth.

That idea became Trump Accounts. Signed into law July 4, 2025, they give every child a brokerage account invested in the S&P 500. The government seeds $1,000 for kids born 2025-2028. Parents can add up to $5,000 per year. And some serious money is backing it. Michael Dell (yes, the Dell Technologies founder) pledged $6.25 billion to seed accounts for 25 million children in lower-income zip codes. Ray Dalio (founder of Bridgewater, the world's largest hedge fund) pledged $75 million for kids in Connecticut.

The vision is bigger than a savings account. It's about giving every American a piece of the country's economic success. But the financial community has been lukewarm. And they're looking at the wrong thing.

The Tax Problem (and How to Defuse It)

The critics have a point: Trump Account withdrawals get taxed as ordinary income. For a physician's kid who follows you into medicine and lands a $350K attending salary, that's 32-37% federal tax on most of the account. Compare that to a UTMA (Uniform Transfers to Minors Act, basically a custodial brokerage account you open for your kid at any brokerage) where gains face 0-20% capital gains rates. Not great.

But they're missing the move that changes everything.

At age 18, the Trump Account converts to a traditional IRA. And traditional IRAs can be converted to Roth IRAs. If your kid does this during college with zero income, the 2026 standard deduction of $16,100 shelters most of the taxable amount. On a $200,000 account, the total tax bill is roughly $2,600.

That's it. $2,600 to defuse the whole tax time bomb. The entire account grows tax-free for the rest of your child's life. No RMDs (required minimum distributions, where the IRS forces you to withdraw and pay taxes on a set amount every year starting at age 73). No ordinary income tax at withdrawal. Ever.

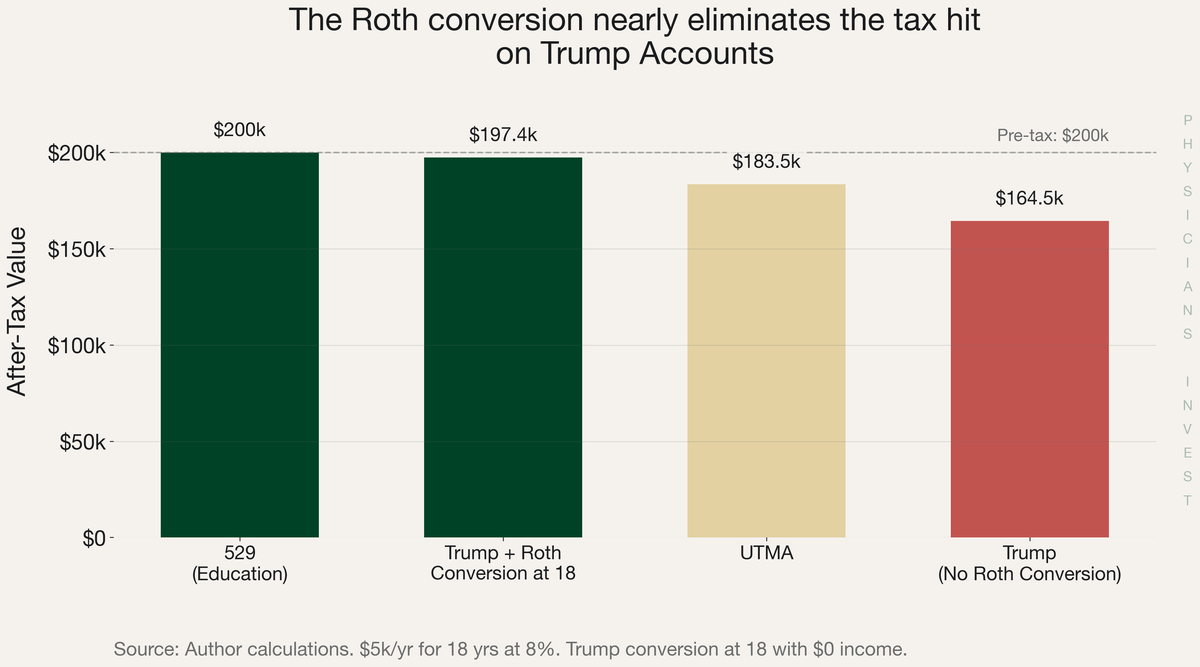

The difference is stark. Here's what happens to the same $200,000 across four account types after taxes:

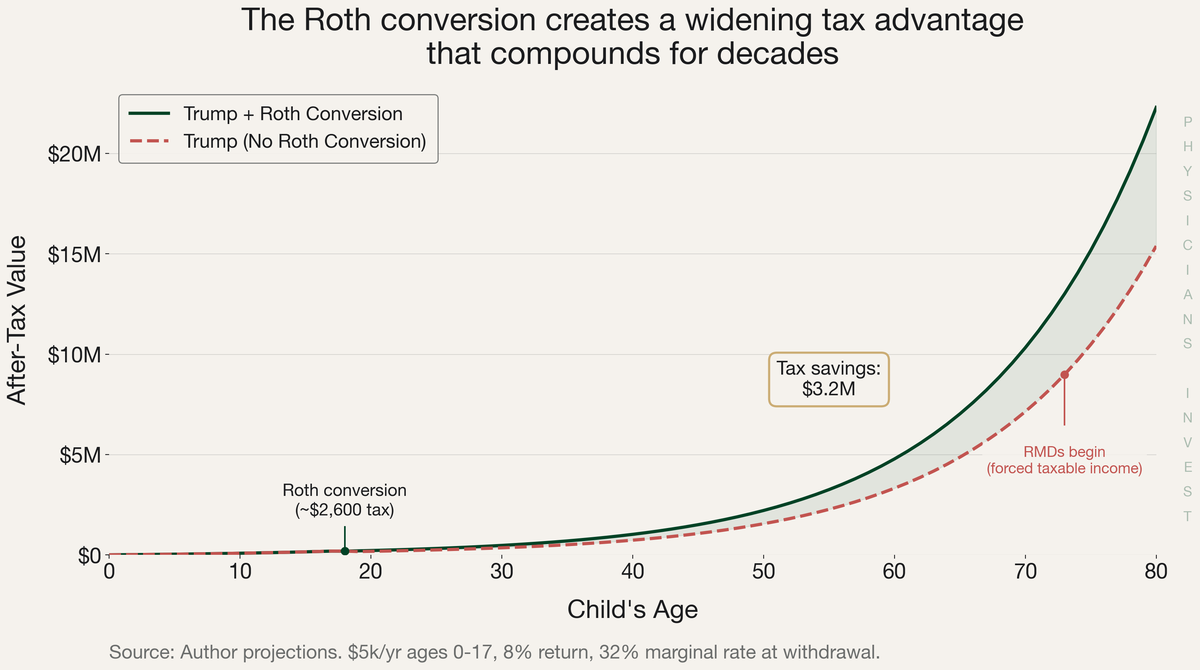

And that gap only widens over time. By the time your child hits 70, the Roth conversion path has created over $3 million in additional after-tax wealth compared to leaving it as a traditional IRA:

The Stacking Play Nobody's Talking About

Trump Account contributions don't eat into your child's Roth IRA limit. If you employ your kid in your practice (routine tasks starting around age 10, customer-facing work by 15), they can max a custodial Roth IRA at $7,500 per year. Combined with $5,000 in the Trump Account, that's $12,500 per year in tax-advantaged retirement savings for your child. At 18, convert the Trump Account into the Roth, and it all becomes one tax-free pile.

We haven't seen anyone else write about this pairing. It's the physician practice owner's edge.

Asset Protection & Guardrails

Here's an angle that should resonate with every physician who's thought about malpractice exposure. Trump Accounts convert to IRAs. IRAs receive creditor protection in most states. A UTMA? Once your kid hits majority, those dollars have zero protection. And zero restrictions.

Charlie Munger's first rule of compounding: never interrupt it unnecessarily. A UTMA hands an 18-year-old unrestricted access to a six-figure account. Less discipline. More status spending. The IRA structure is a guardrail. The money stays invested. Compounding continues.

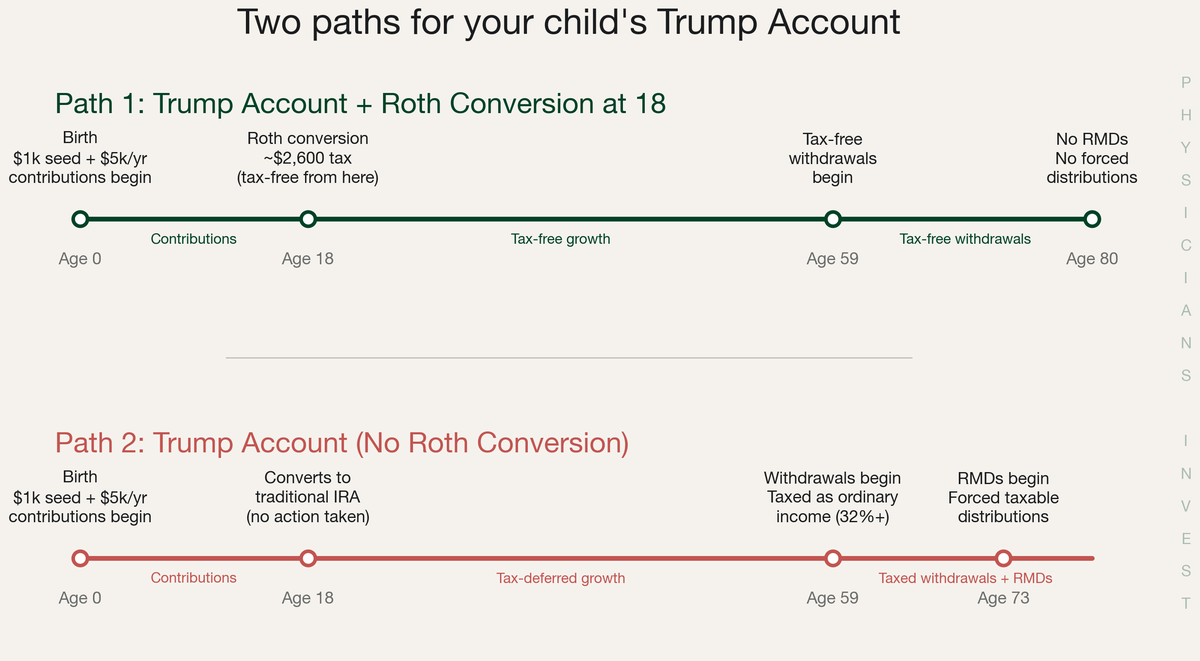

Here's what the two paths look like side by side:

One path ends with tax-free withdrawals and no forced distributions. The other ends with ordinary income tax and RMDs at 73. The choice is straightforward.

The Move

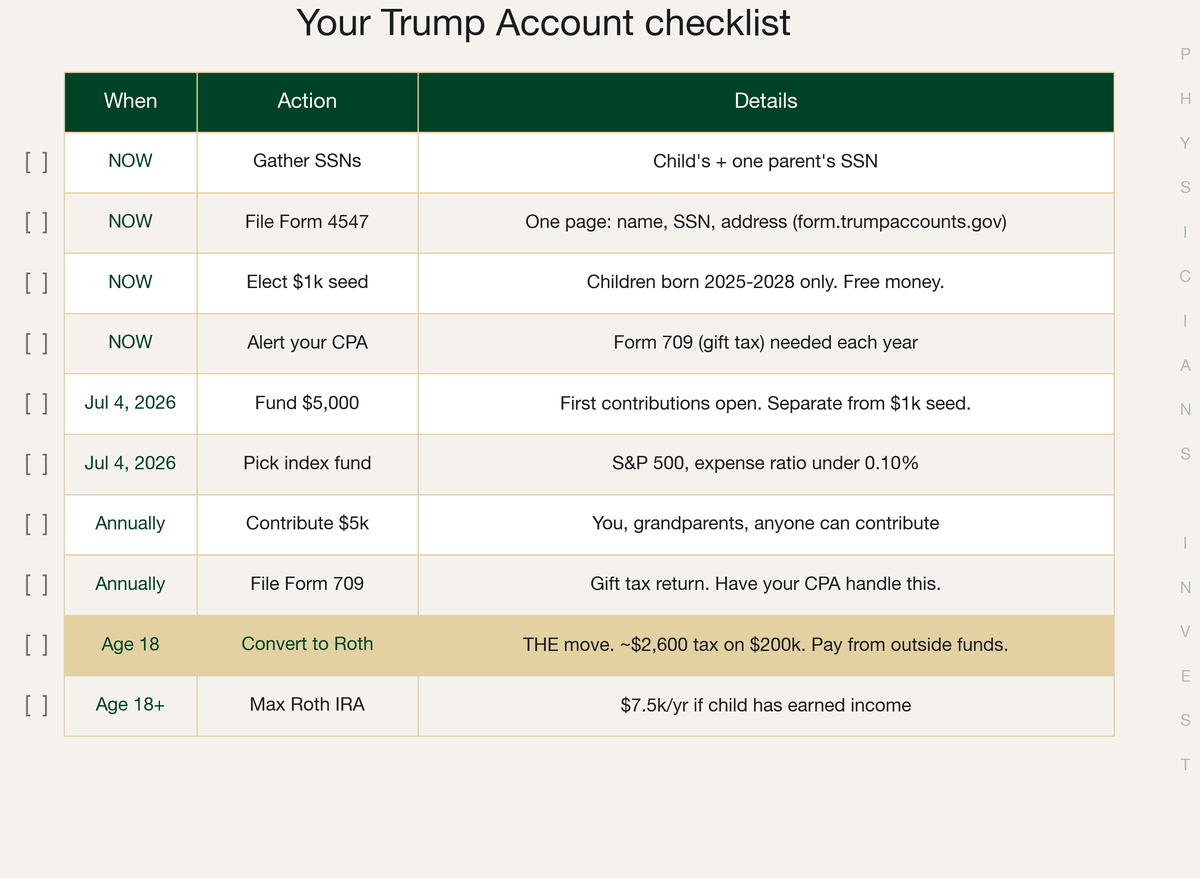

We think every physician with children should open a Trump Account. And in our view, the Roth conversion at 18 is non-negotiable. Here's the general sequence:

- Now: File Form 4547 at form.trumpaccounts.gov. Five minutes. You need your SSN and your child's SSN. (We've done it. Best government form we've ever filled out. The student loan programs should take notes.)

- Now: If your child was born 2025-2028, elect the $1,000 government seed. Free money that doesn't count against your $5,000 annual limit.

- Now: Tell your CPA. Each contribution requires a Form 709 gift tax filing. It's paperwork, not a tax bill (you're well under the $15M lifetime exemption). This is not a TurboTax-friendly situation.

- July 4, 2026: Fund $5,000 into an S&P 500 index fund with an expense ratio under 0.10%.

- Every year: Contribute $5,000. Anyone can contribute: you, grandparents, friends.

- Age 18: Convert to a Roth IRA while your kid has zero income. Pay the small tax from outside funds. This is the whole ballgame.

We put together a printable checklist so you can track every step:

One wrinkle on the gift tax: the current law requires Form 709 for every contribution because Trump Account deposits are classified as "future interest" gifts. We think this was a drafting oversight that'll get fixed. But until it does, plan for the annual filing with your CPA.

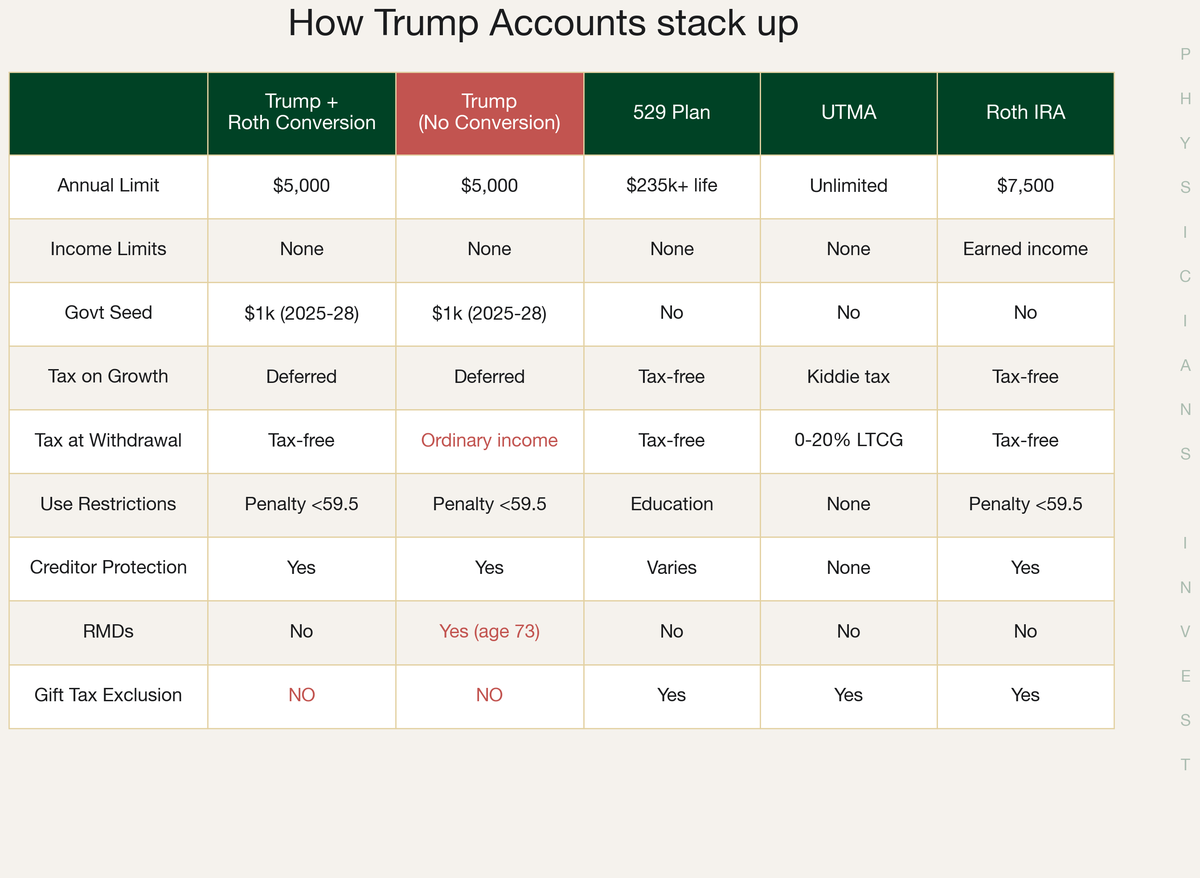

How It Compares

If you're wondering how Trump Accounts stack up against other accounts you might already have for your kids, here's the side-by-side:

What About the Investment Risk?

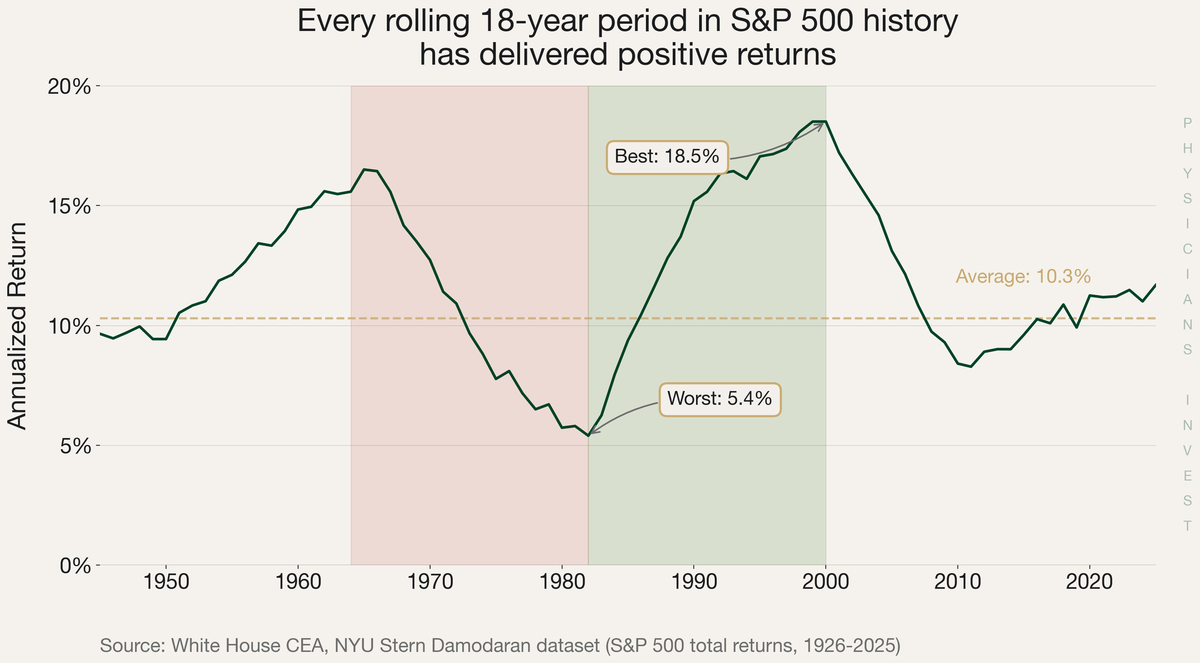

During the growth period (birth through age 17), Trump Accounts can only be invested in U.S. equity index funds with expense ratios under 0.10%. No individual stocks. No bonds. No international. The legislation baked in low-cost index investing by design. That's actually a feature, not a bug. It removes the temptation to tinker.

That naturally raises the question: is 18 years in a U.S. equity index safe? According to the White House CEA, every rolling 18-year period in S&P 500 history has delivered positive returns. The worst was 5.4% annualized. The average was 10.3%. It's a decent bet the investment will turn out just fine.

Sources

Government & Policy

- IRS: Treasury Guidance on Trump Accounts (Notice 2025-68)

- IRS: Proposed Regulations for Trump Account Pilot Program

- IRS: 2026 Tax Inflation Adjustments (OBBBA)

- IRS: 2026 IRA Contribution Limits

- White House CEA: Trump Accounts Give Next Generation a Jump Start

Analysis

- Boston College CRR: Trump Accounts -- A Primer for Parents

- Kitces: Why Taxable Custodial Accounts Are Better Than Trump Accounts

- White Coat Investor: Trump Accounts

- American Action Forum: Trump Accounts Are Here

Tax & Legal

- EisnerAmper: Trump Accounts -- How They Work and Who Benefits

- Carr, Riggs & Ingram: Trump Account Gift Tax Rules

Data