US stocks kept climbing through May, then gave back a few percent last week. International stocks took a hit after a strong start to the year. Energy stocks continued higher on ongoing Middle East tensions, Bitcoin fell off a cliff and is down significantly on the year, and bonds had a quiet month.

The 2-Minute Version

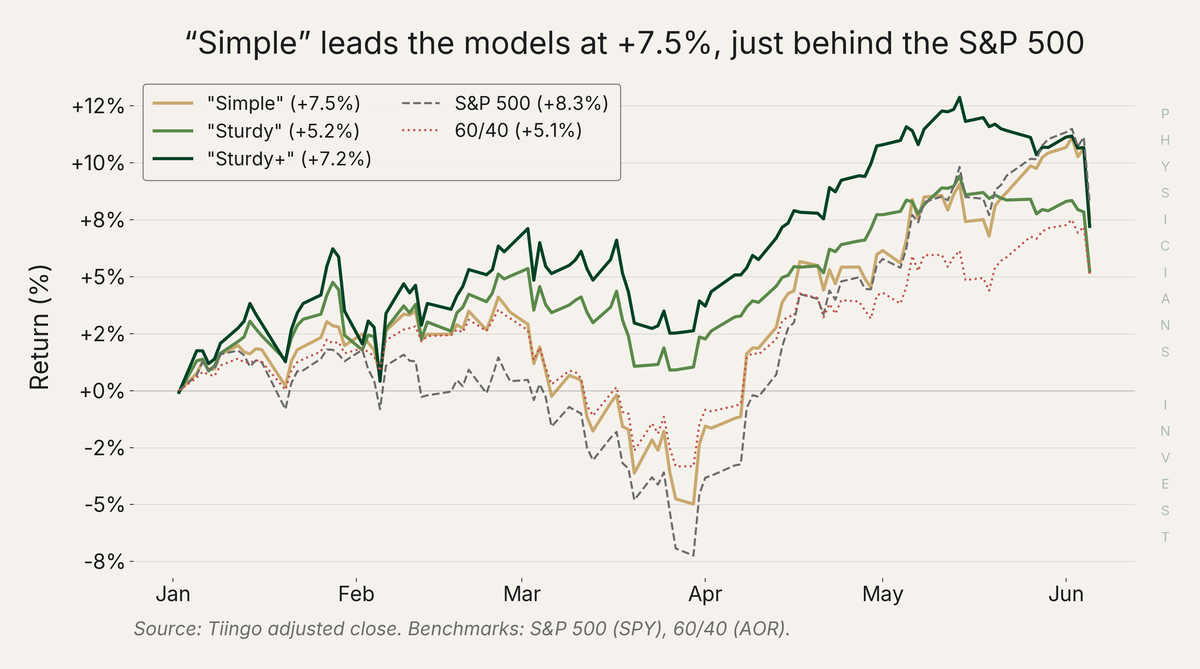

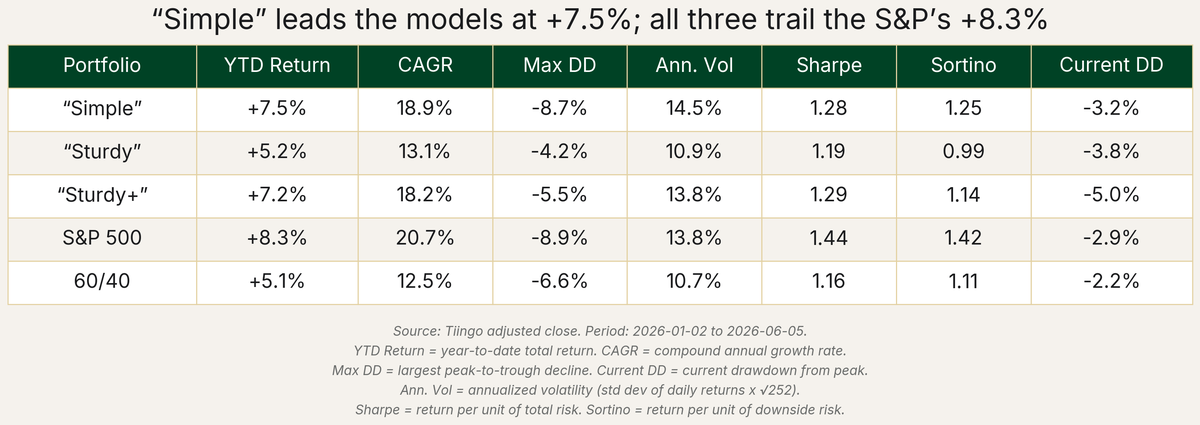

- Simple leads our models at +7.5% YTD, just behind the S&P 500's +8.3% YTD.

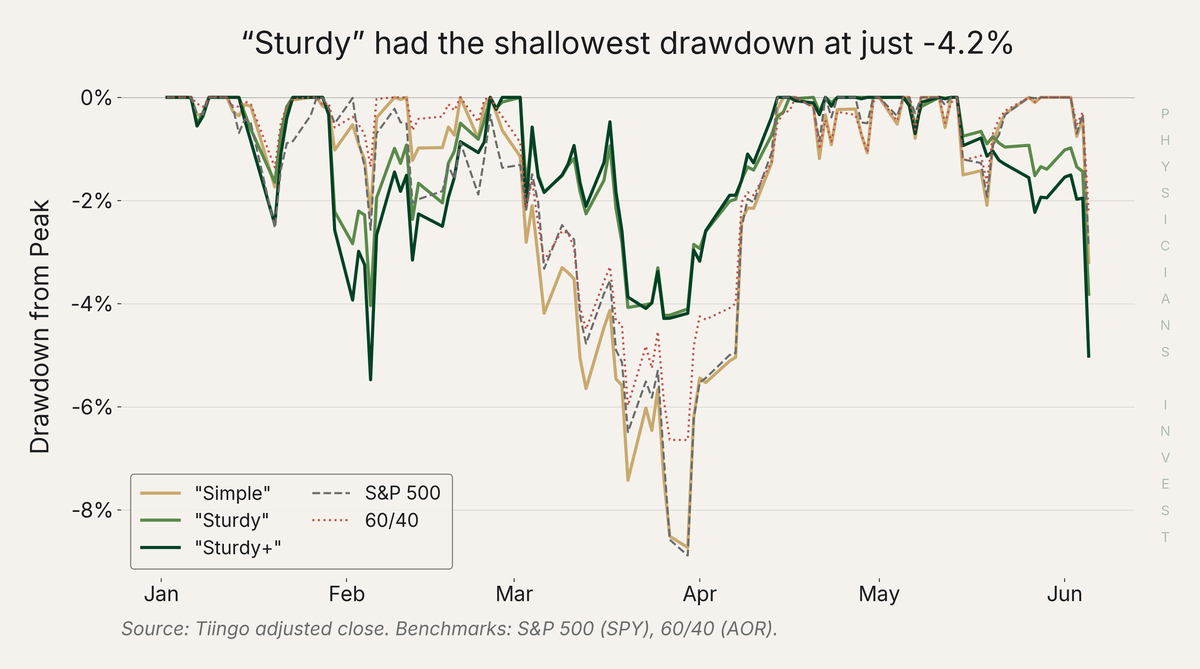

- Sturdy had the smoothest ride. Its worst drawdown (its biggest peak-to-trough drop) was just -4.2%, roughly half the S&P 500's. It currently sits at 5.2% YTD.

- Sturdy+ has returned +7.2% YTD and carries the best risk-adjusted return of the three (Sharpe of 1.29, the best return per unit of risk).

- Bitcoin (IBIT) is down 33% YTD. This provides a strong tax-loss harvesting opportunity.

Market Context

May was a continuation of the spring rally for US stocks. While the US showed growth, International stocks fared more poorly and are down 3% over the past month. Stocks were strong through all of May and then the first week of June handed back a few percent across all the major indices. Last Friday was particularly pronounced downside action. As the returns suggest, international stocks were hit harder than US stocks in this last week's pullback.

Outside of equity indices, the energy sector continues to provide strong returns. The energy holding (XLE) is up 27% on the year. Bitcoin, on the other hand, has been an anchor on portfolios the past month. The bitcoin ETF, IBIT, is down 33% year-to-date, and most of that damage came in the last couple weeks. Gold pulled back over the past month, though it is roughly flat on the year. When assets sell off the way bitcoin has, tax loss harvesting opportunities present themselves. We will discuss in the portfolio section how to take advantage of this.

Other than tax loss harvesting opportunities, there are no changes to any of the portfolios this month.

Performance Dashboard

Source: Physicians Invest model portfolio. Hypothetical $100K, not actual returns.

Source: Physicians Invest model portfolio. Hypothetical $100K, not actual returns.

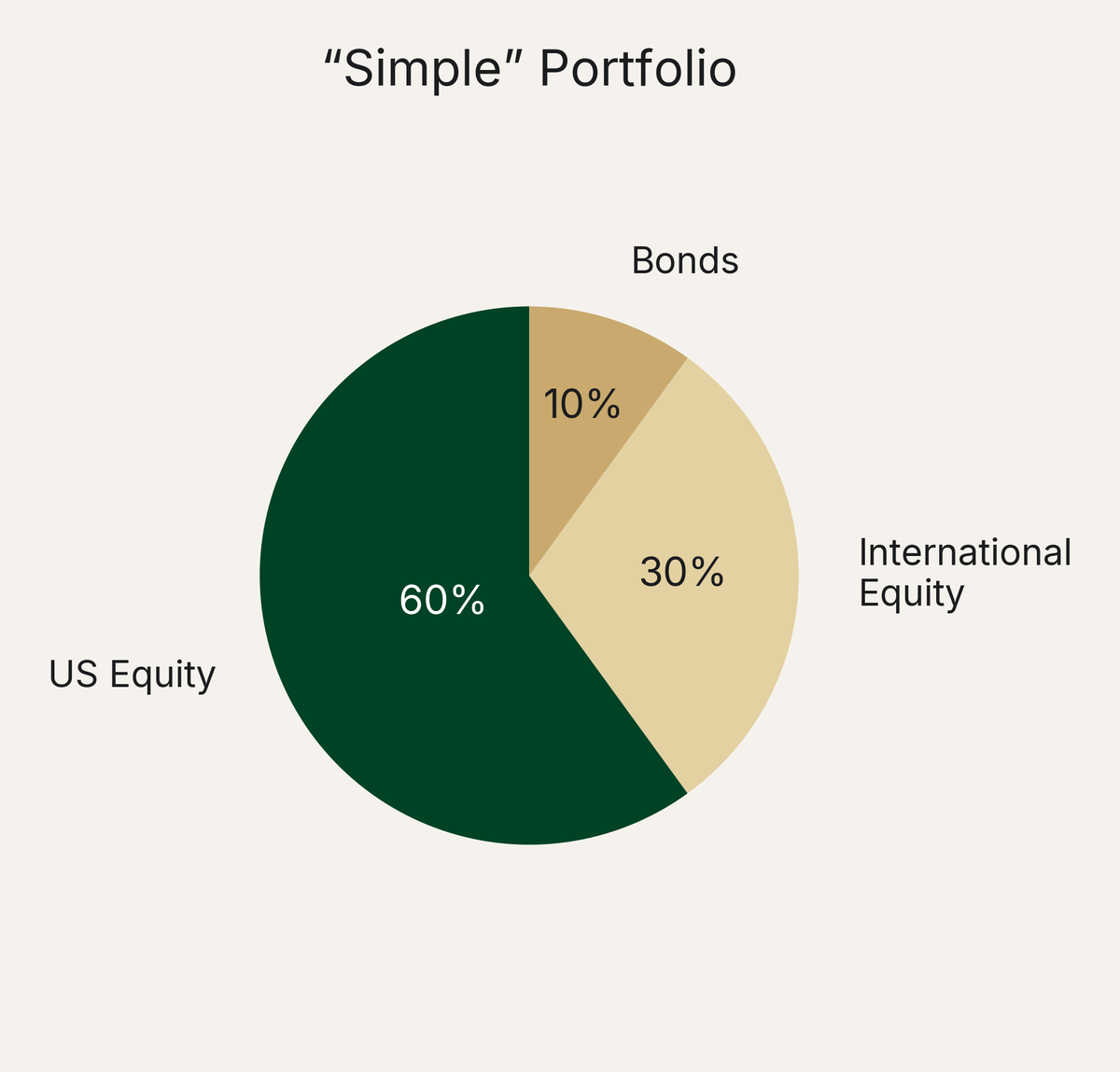

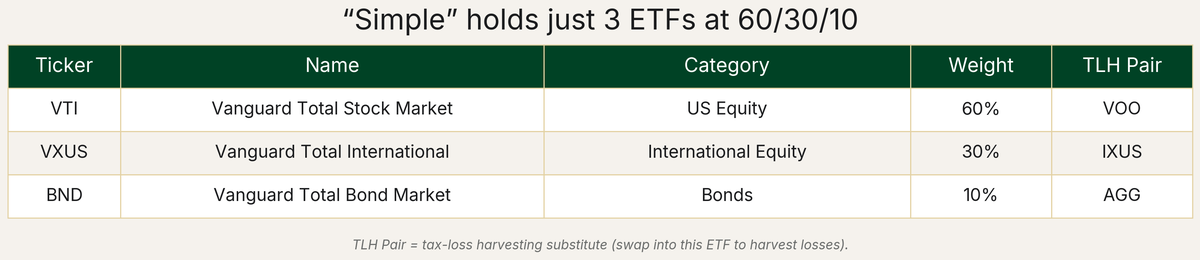

"Simple" Portfolio

For: Residents and early-career physicians who want a "set it and forget it" approach.

Strategy: Three ETFs at 60/30/10. Beauty in simplicity.

Advantages: Lowest expense ratios in the lineup (under 0.05% blended; expense ratio is the annual fee an ETF charges, expressed as a percent of assets). Easy to rebalance with three line items. No exotic holdings.

Disadvantages: Concentrated in stocks and bonds. When both go down together (like Q1 2026), there is nowhere to hide. Diversifies across assets but does not perform well when interest rates are increasing (2022).

Tax-Advantaged Tweak: In a Roth or 401(k), investors who want real-estate exposure could add a 5-10% REIT (real estate investment trust) slice carved from US equity (VNQ is one common ETF to use for this). REITs throw off ordinary income that gets taxed at the marginal rate in a taxable account so it should be kept in tax-protected accounts only.

What Changed

No changes this month. The Simple portfolio is designed for long-term holding with minimal intervention.

Tax Loss Harvesting Opportunities

One holding is slightly underwater YTD:

- BND (Total Bond Market): at the beginning of the year it traded around $73, and its price is now about 0.7% lower, a small unrealized loss on shares bought then. The tax-loss harvesting substitute is AGG.

Tax-loss harvesting means selling a position at a loss to bank that loss against future gains (or up to $3,000 of ordinary income a year), then buying a near-identical fund to stay invested. A 0.7% loss on a bond fund is thin, so this is probably not worth the hassle for most investors. Harvesting it means the wash-sale rule applies: the same fund cannot be repurchased within 31 days, which is why the swap goes into AGG rather than back into BND.

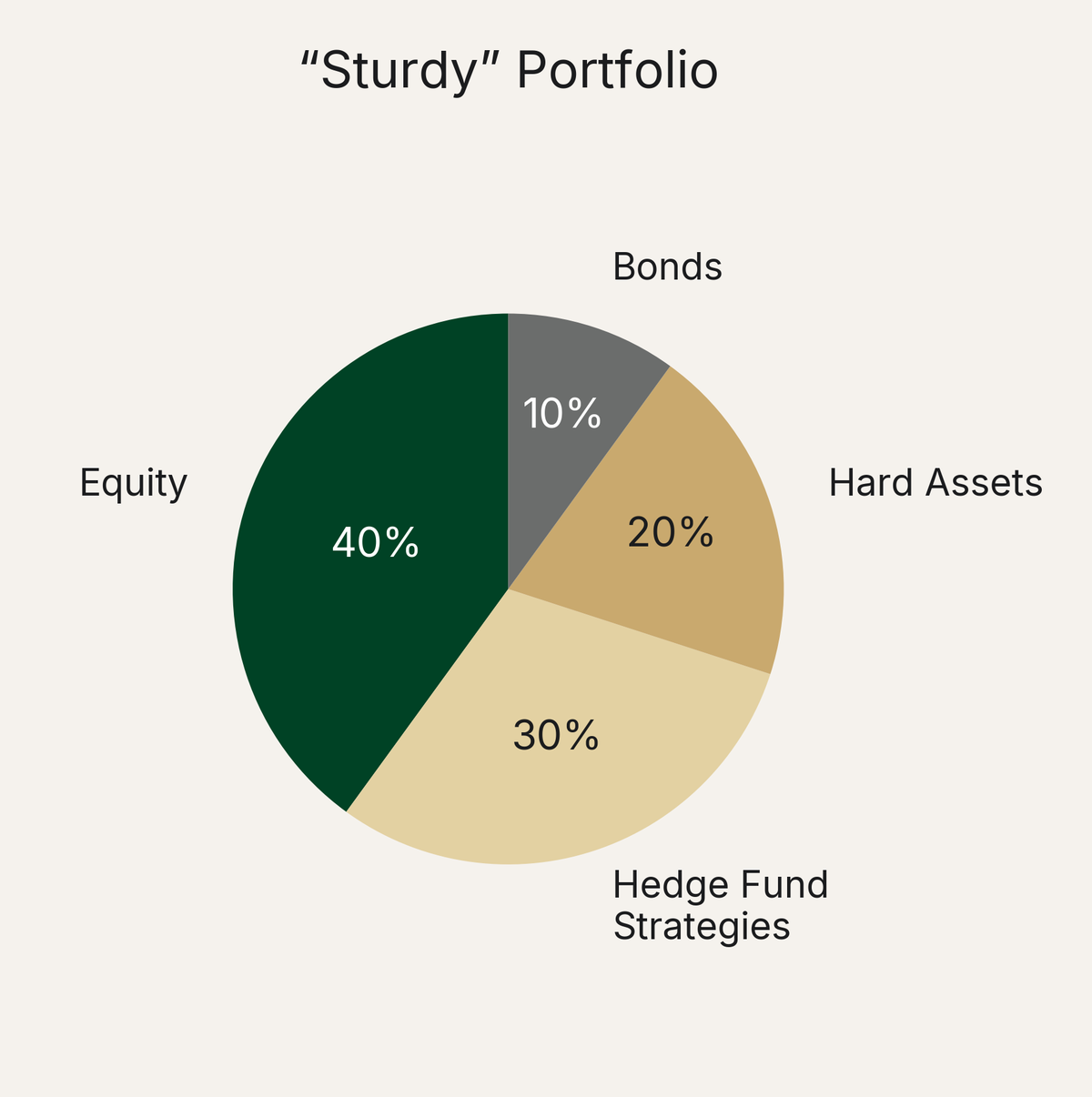

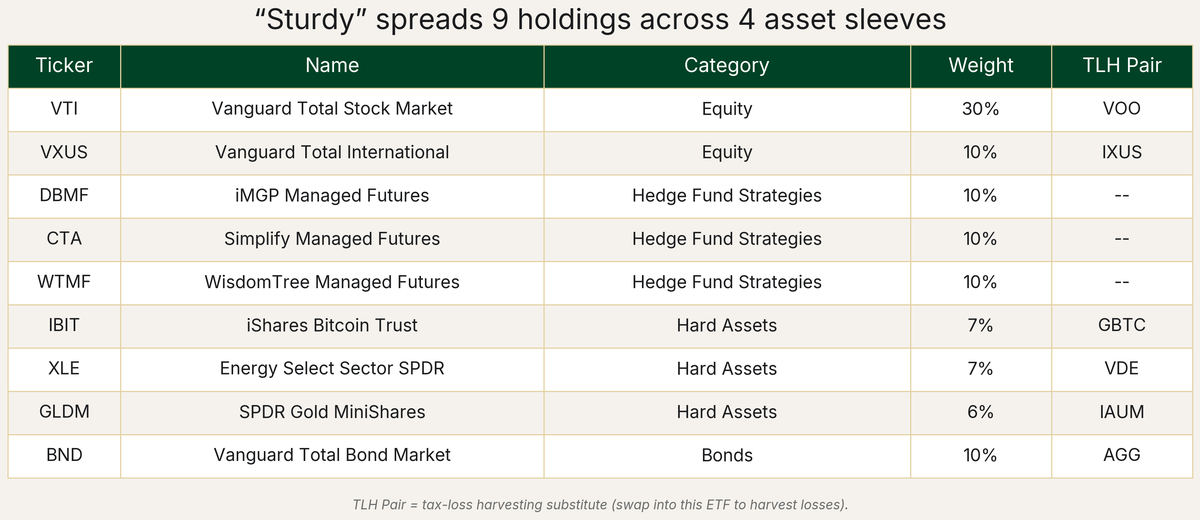

"Sturdy" Portfolio

For: Mid-career attendings who want a smoother ride without giving up return.

Strategy: 40% equity / 30% hedge fund strategies / 20% hard assets / 10% bonds.

Advantages: Lower volatility for the same long-term performance as Simple. A much smoother ride without giving up return. Diversifies risk exposures away from just stocks.

Disadvantages: Nine holdings means more rebalancing complexity than Simple. Hedge fund ETFs have higher expense ratios (0.65-0.85%) than the equity holdings and take more homework to understand: what they are doing under the hood, how they make money, and when they pay off.

Tax-Advantaged Tweak: Asset location is the practice of placing tax-inefficient holdings in tax-sheltered accounts. Place more BND, GLDM, WTMF, CTA, and DBMF exposure in tax-sheltered accounts and more index fund exposure in taxable brokerage accounts (VTI, VXUS, XLE, IBIT).

What Changed

No changes this month.

Tax Loss Harvesting Opportunities

Three holdings are underwater versus their add price:

- IBIT (iShares Bitcoin Trust): started the year at $50.94, now around $34.14, an unrealized loss of about 33%. The substitute is GBTC.

- BND (Total Bond Market): Down about 0.7% in price since year start. The substitute is AGG.

- GLDM (gold): Down about 0.4% YTD. The substitute is IAUM.

The IBIT loss is the meaningful one here. A 33% unrealized loss on the bitcoin sleeve is a sizable harvest. Investors who hold IBIT can capture that loss by selling and buying GBTC to keep the same bitcoin exposure. The wash-sale rule requires waiting at least 31 days before rebuying IBIT for the loss to count.

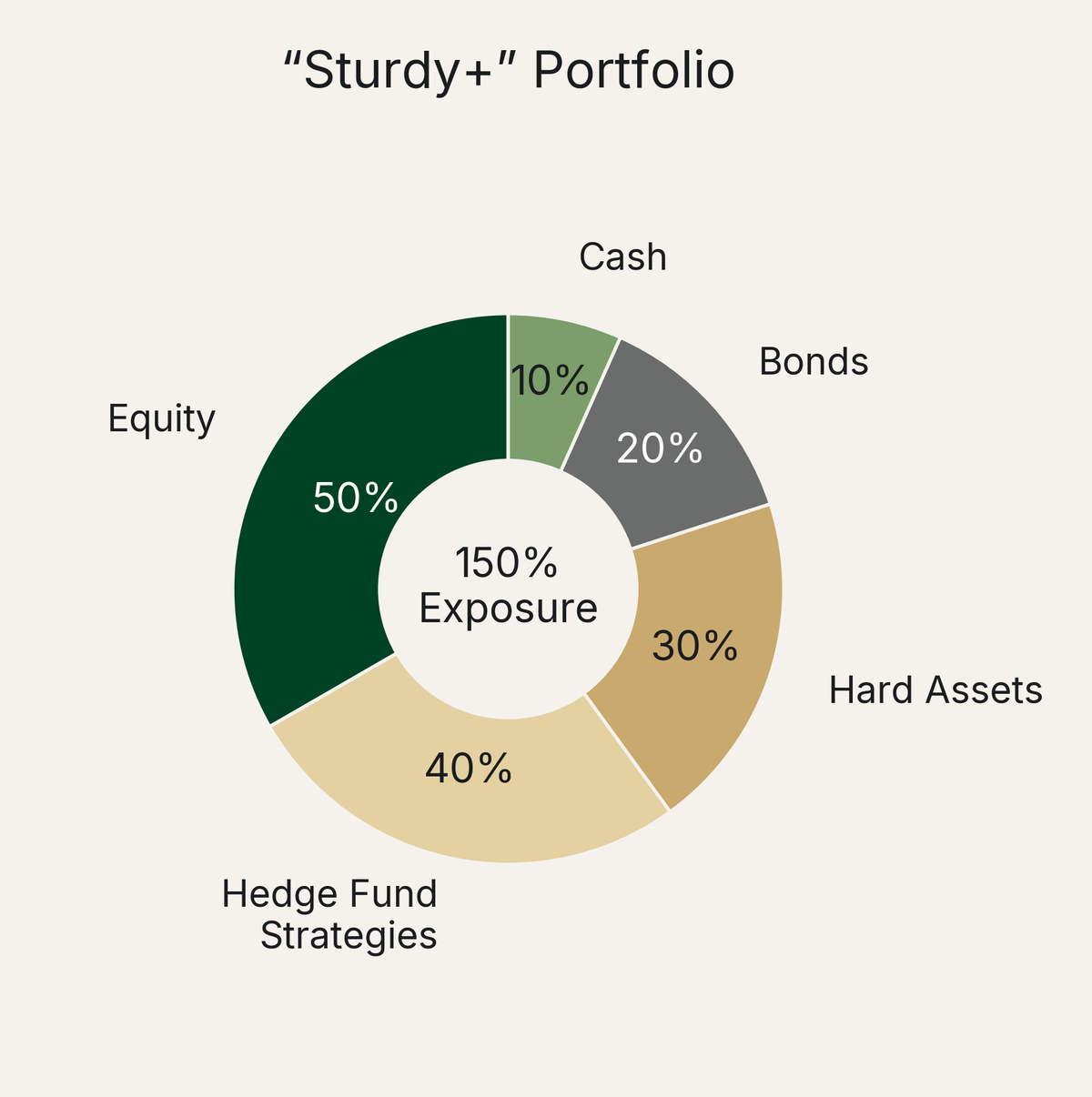

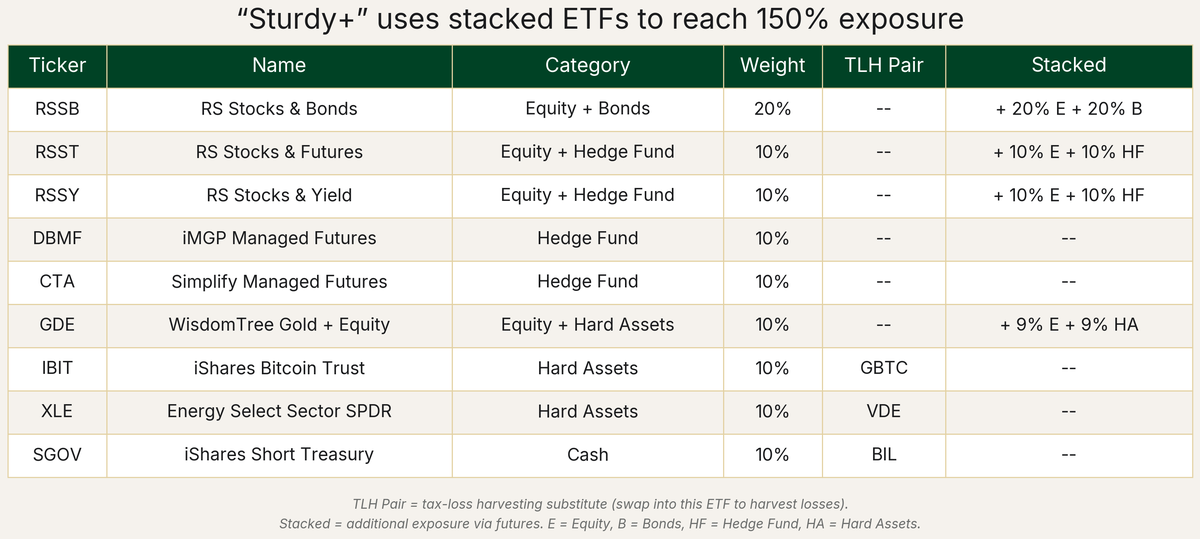

"Sturdy+" Portfolio

For: Sophisticated investors comfortable with leveraged ETF mechanics, looking for higher long-term returns than the market and willing to take on volatility.

Strategy: 150% total exposure via stacked ETFs (RSSB, RSST, RSSY, GDE). A stacked ETF bundles two exposures into one ticker, so $1 invested gives you exposure to both at once.

Advantages: Capital efficiency (getting more market exposure per dollar invested) lets Sturdy+ reach 150% exposure while only deploying 100% of capital. Broker margin (borrowed money from your brokerage used to buy more securities than your cash balance supports) is not needed, so the investor avoids any risk of margin calls and avoids inflated borrowing rates. Investors simply buy these ETFs like any other, and the stacked exposures are already baked in. Futures-based holdings receive 60/40 tax treatment: gains are split 60% long-term and 40% short-term no matter how long you hold them, making this more tax-efficient than you might expect for a leveraged strategy.

Disadvantages: More volatile than Sturdy due to the additional exposure. More complex to understand and requires real effort to learn the mechanics. Stacked ETFs are newer products with shorter track records. Requires comfort with leverage and futures, even though the implementation is straightforward.

How the Leverage Works: Four holdings provide stacked exposure:

- RSST (10% of portfolio) = 10% US equity + 10% hedge fund strategies (trend following: a strategy that buys assets going up and sells assets going down)

- RSSY (10% of portfolio) = 10% US equity + 10% hedge fund strategies (carry: earning the yield difference between holding an asset and financing it)

- RSSB (20% of portfolio) = 20% global equity + 20% bonds

- GDE (10% of portfolio) = 9% US equity + 9% gold

Think of stacked ETFs like combination drugs: Augmentin gives you amoxicillin plus clavulanate in one pill. RSST gives you S&P 500 plus hedge fund strategies in one ticker. Combined with the standalone holdings (DBMF, CTA, IBIT, XLE, SGOV), total exposure reaches approximately 150% while only deploying 100% of capital. No broker margin is required, and a much lower effective borrowing rate than broker margin can be realized.

Tax-Advantaged Tweak: Investors typically prefer holding SGOV in tax-advantaged accounts (Roth, 401(k), 403(b)). Bond interest is taxed at ordinary income and benefits more than the other ETFs from sheltering in tax-advantaged vehicles.

What Changed

No changes this month.

Tax Loss Harvesting Opportunities

Same as Sturdy. One holding offers a meaningful harvest opportunity:

- IBIT (iShares Bitcoin Trust): A YTD unrealized loss of about 33%. The substitute is GBTC.

This is the strongest harvest across the three models. Investors who hold IBIT can sell it, bank the ~33% loss against future capital gains, and buy GBTC to keep the bitcoin exposure intact. The wash-sale rule requires waiting at least 31 days before rebuying IBIT.

Methodology

These model portfolios track a hypothetical $100,000 investment made on January 2, 2026. All prices use adjusted close from Tiingo (accounts for splits and dividends). No transaction costs, slippage, or taxes are modeled. Benchmarks: SPY (S&P 500 ETF) and AOR (iShares Core Growth Allocation ETF, a 60/40 proxy). All metrics annualized where applicable.

The portfolios are account-agnostic. They work in taxable, traditional IRA, Roth IRA, 401(k), or any other account type. Tax-advantaged tweaks are noted per portfolio as suggestions, not requirements.

Want help building one of these portfolios? Book a free consultation.

These are hypothetical model portfolios for educational purposes only. They do not represent actual investments, do not account for transaction costs or taxes, and are not personalized investment advice. Past hypothetical performance does not guarantee future results. Physicians Invest does not manage client assets. Consult a qualified financial advisor before making investment decisions.