The 2-Minute Version

- SGOV (an ETF that holds short-term Treasuries) pays about 0.17% more than a reputable high-yield savings account pre-tax, and up to 0.55% more after tax in high-tax states. On $100,000 of cash, that's $170 to $552 a year.

- Banks offering HYSAs take your deposit, buy short-term Treasuries with it, give you a rate less than short-term Treasuries, and keep the spread. Cut out the middleman.

- Open a Schwab account, buy SGOV, keep a small HYSA buffer for instant cash needs.

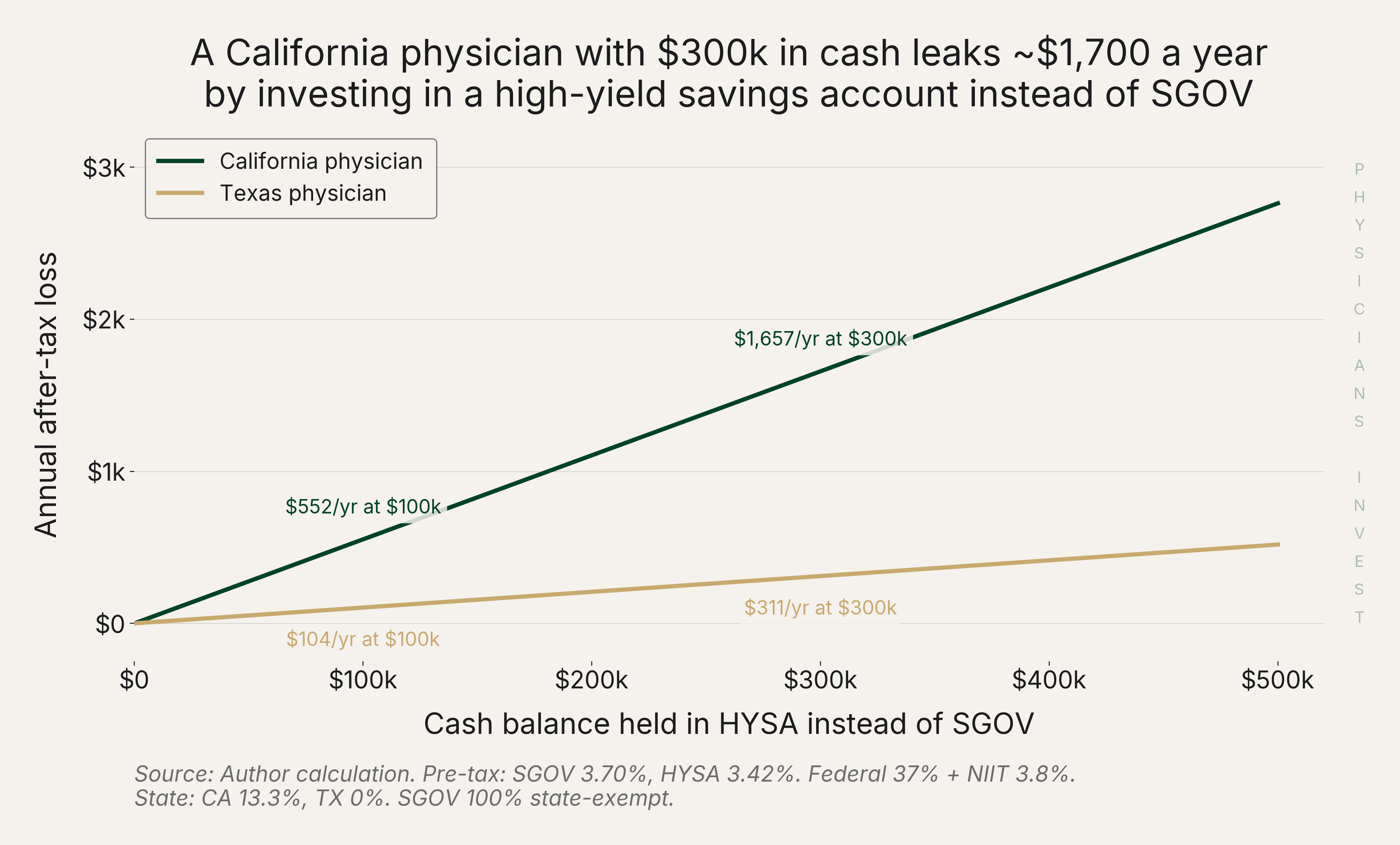

Imagine ten $1 bills sitting on a table. You are entitled to take all ten if you wanted to. Instead, you take nine and leave the last one sitting there just because it is slightly more work to reach out and grab it. Investing in a High Yield Savings Account (HYSA) is like not going the easy extra step to get the last dollar. Let's put some real numbers to this. For a California-based attending with $100,000 in cash, that one missing dollar is worth about $552 a year. Do that every year and the numbers add up fast.

The Setup

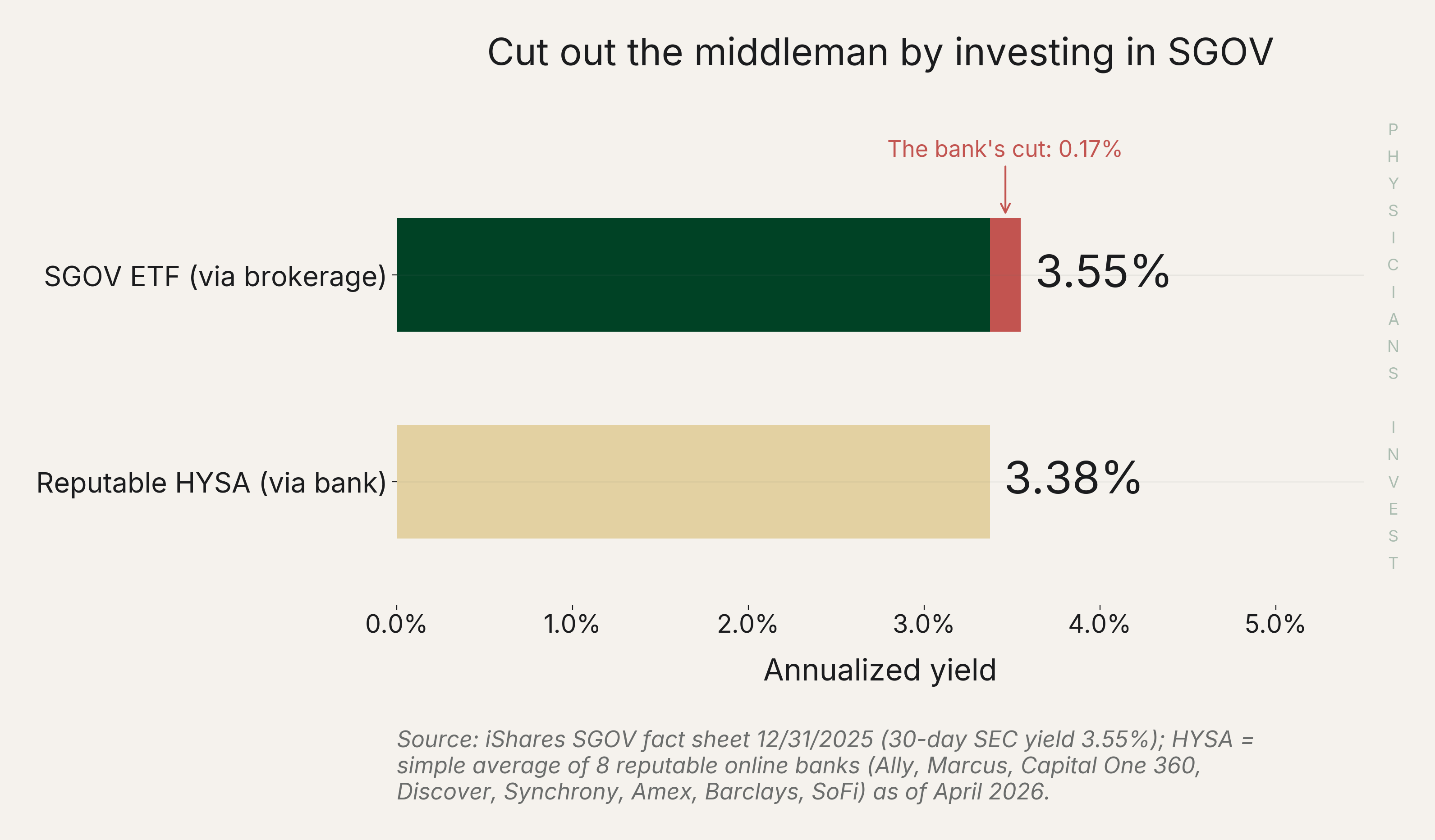

First, let's understand exactly why banks offer high-yield savings accounts. Banks are a business, so why are they paying you money? Here's what's happening behind the scenes. Your high-yield savings account deposit doesn't actually sit in a vault. The bank takes that deposit, buys short-term Treasuries with a portion of it, and pays you a yield that's lower than what the Treasuries earn. The difference is the bank's cut. That's how the business model works, and to be clear, we're not saying it's evil or ill-intentioned. It's the same reason a hospital charges $200 for a lab test that costs them $40 at the reference lab. There's a middleman, and the middleman takes a cut.

Today, in April 2026, SGOV (an exchange-traded fund that holds the same short-term U.S. Treasuries the bank is buying with your HYSA money) has a 30-day SEC yield of 3.55%. The 30-day SEC yield is the SEC's standardized way of measuring what a fund actually earned over the last 30 days, annualized after expenses. This is a good approximation of your expected yield for the next month or so. HYSAs are harder to pin down because the rate is set purely at the discretion of the bank, but it is always lower than Treasuries at reputable firms. In order to get an estimate of the current HYSA yield for an apples-to-apples comparison, we took the simple average of eight reputable online HYSAs (Ally, Marcus by Goldman Sachs, Capital One 360, Discover, Synchrony, American Express, Barclays, and SoFi with direct deposit) via Doctor of Credit's rate tracker. The average yield is 3.38% with a fairly tight spread. That 0.17% difference between the HYSA and the SGOV ETF yield is the spread the bank keeps. On $100,000 of cash, that's $170 a year. Before taxes even enter the conversation, which makes the case for SGOV even stronger.

The Analysis

Where you physically live changes the math

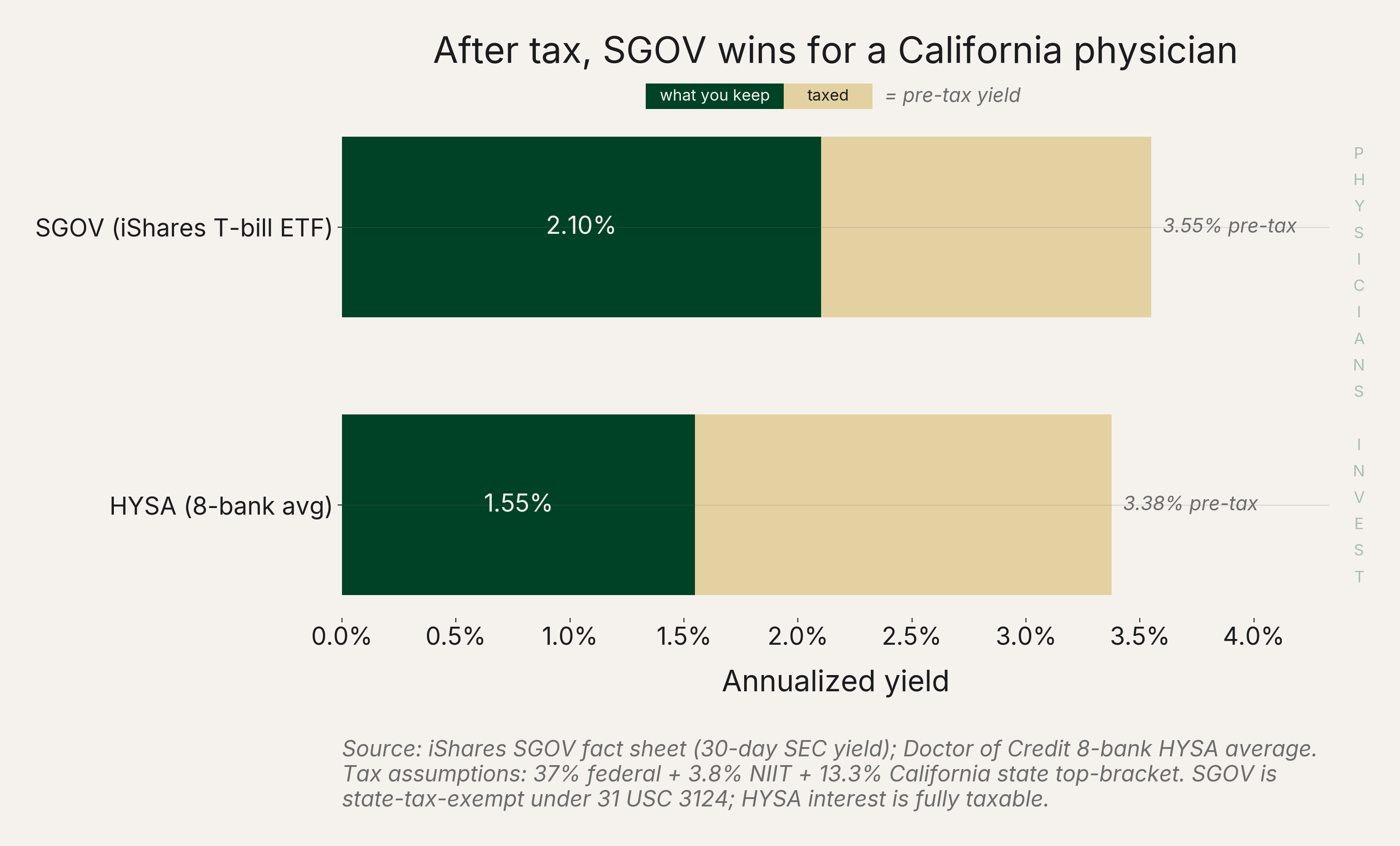

The spread gets wider once you factor in state tax. Treasury interest is EXEMPT from state and local income tax under federal law. That's correct, SGOV interest is fully exempt for state and local taxes. HYSA interest is FULLY TAXABLE at every level. For a California physician in the top bracket (37% federal + 3.8% Net Investment Income Tax (NIIT) + 13.3% state), that pre-tax 0.17% spread becomes a 0.55% gap after tax. On $100,000 of cash, that's $552 a year. Roughly $46 every month. Put that money towards much better things: investments, a premium subscription to Physicians Invest, a night out. The list goes on, but please not the bank.

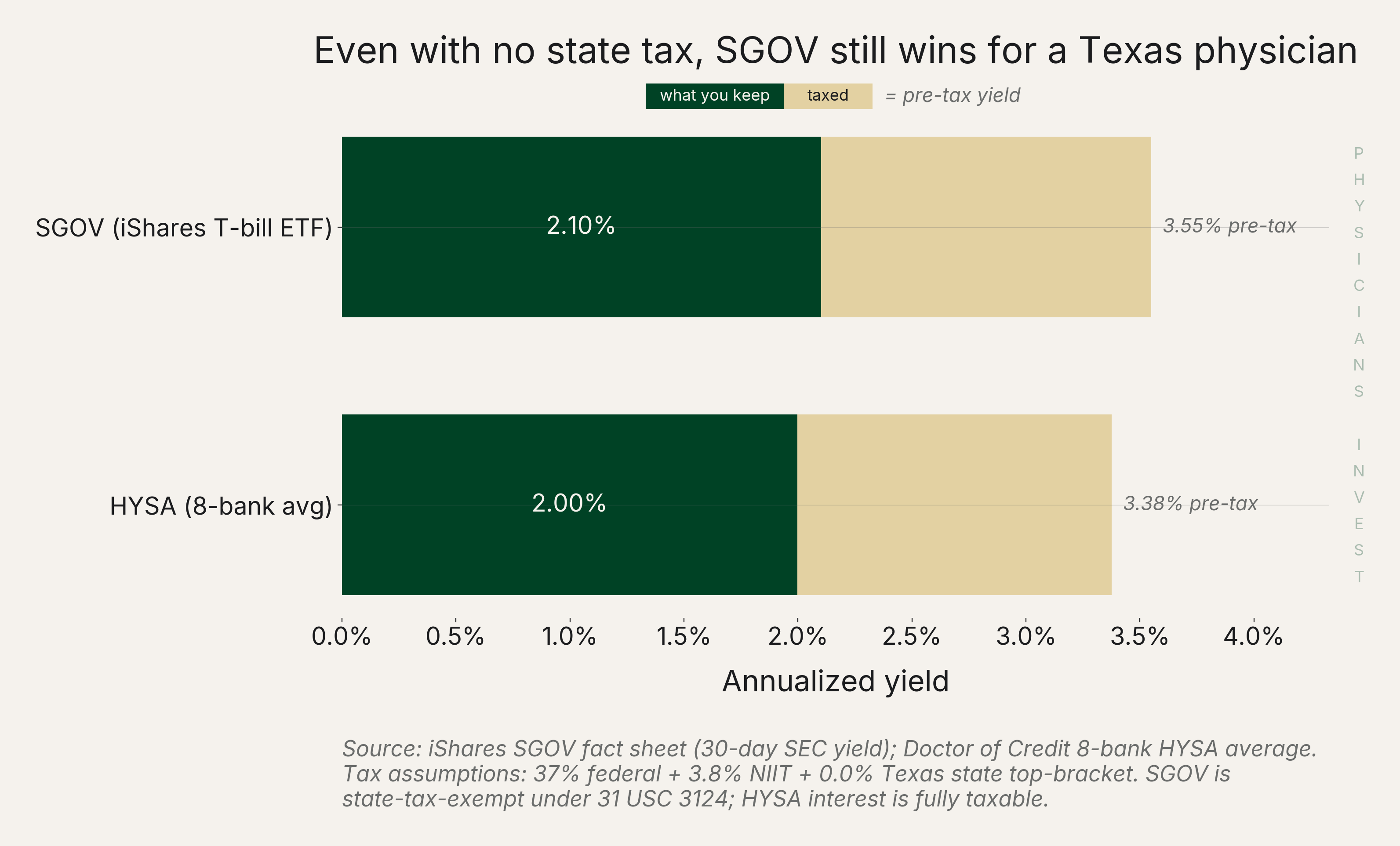

What if I live in a no-tax state like Texas or Florida? Not as big of a win, but SGOV still wins. The state-tax edge disappears, but the pre-tax yield advantage carries through. SGOV's 3.55% still beats the HYSA average of 3.38%, so a Texas physician with $100,000 in cash is leaving about $104 a year on the table. A win is a win.

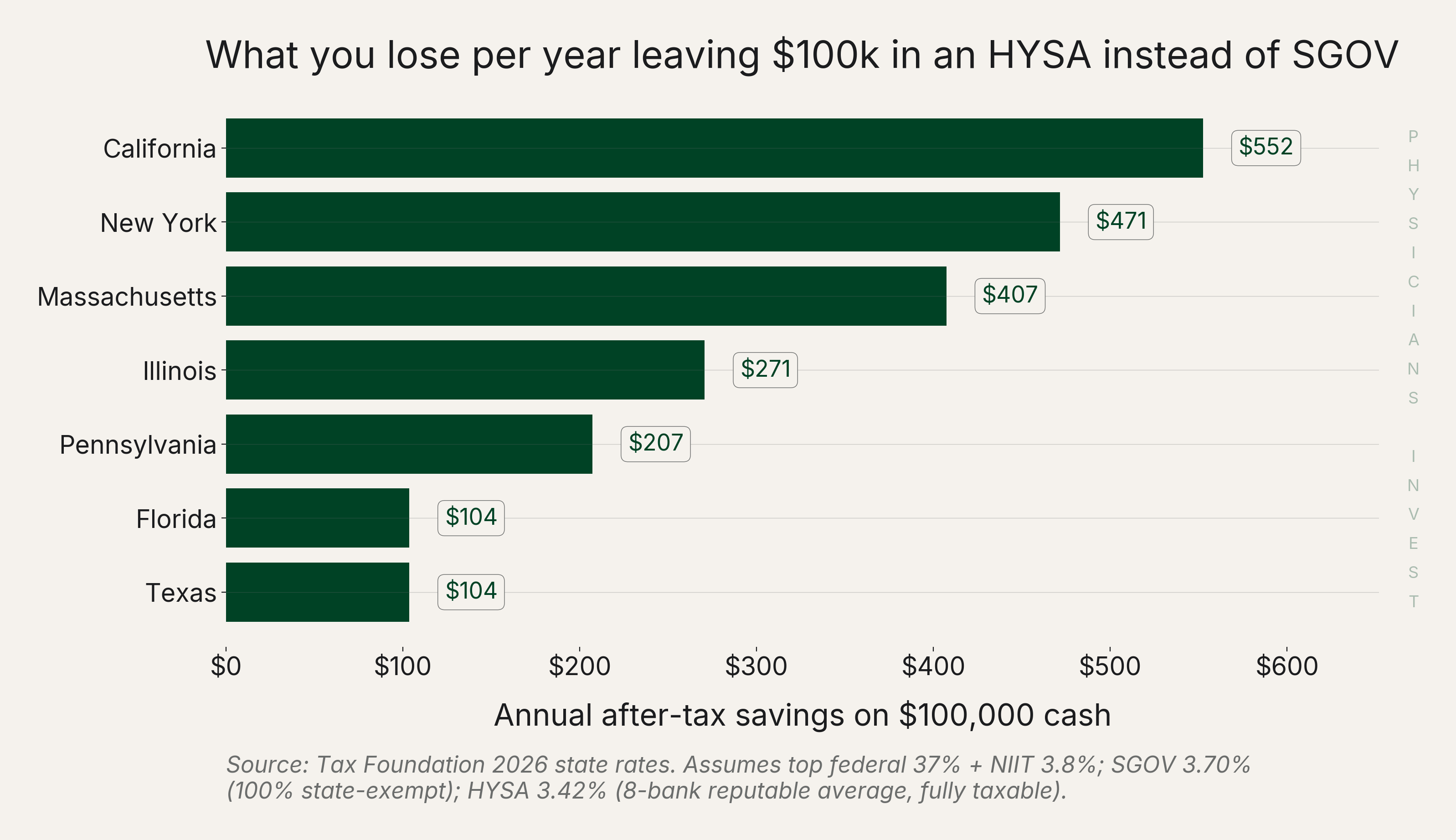

Because of the state tax exemption, the size of the gap depends heavily on what state you practice in. As a reference, here's what $100,000 in cash costs you per year, by state:

So all in all, it's worth stepping back and looking at the full ladder of options for your cash holdings from worst to best. There are three primary places physicians park cash: traditional bank accounts, high yield savings accounts, and ETFs. Traditional bank accounts at institutions like Chase or Bank of America pay close to nothing for retail investors (the FDIC national average savings rate is 0.38%), and inflation is eating your purchasing power at more than 2% a year. This is the bottom rung for cash investments. They pay almost nothing, you are losing purchasing power due to inflation, and it's not a good decision. A reputable HYSA is the middle rung, and it's where most physicians land. It's reasonable, but it's not where you should stay. The top rung are short term Treasury ETFs like SGOV. The move up from HYSA to SGOV is smaller than the move from Traditional to HYSA for no-state-tax physicians, but it's still worth making.

A quick word on money market funds

Some of you will ask about money market funds. Fair question. Vanguard's VMFXX and VUSXX actually edge out SGOV by a whisker for a California physician after tax, because both hold enough direct U.S. Treasuries to clear California's 50% exemption threshold. But they're Vanguard-only, and VUSXX has a $50,000 minimum investment. Schwab's default SWVXX (a prime fund holding commercial paper, not Treasuries) and Fidelity's default SPAXX (which failed California's quarter-end threshold in 2025) are both fully state-taxable in California and lose to SGOV. If you already keep cash at Vanguard, VUSXX is a fine pick. Although, you are required to put up with Vanguard's clunky user interface and "impossible to do things easily" customer service which has its own cost...your sanity. For everyone else, SGOV is the move.

The Move

Here's the playbook:

- Open a Schwab brokerage account. About 15 minutes online. If you already have one, skip this step. We recommend Schwab specifically because they run an institutional-grade banking system and brokerage under the same login. Transferring cash between the two is as fast as moving money inside a single bank. The interface is clean, the fees are zero, and their bank account reimburses ATM fees anywhere in the world. Disclaimer: we are in no way partnered with Schwab. We just like them as your best option here.

- Link your current checking account for transfers. Could be at Schwab or at any other bank.

- Buy SGOV ETF. Just type in the ticker SGOV and it will pop up. Treat it like cash. Buy an amount equivalent to whatever you'd otherwise keep in your HYSA. Minimum purchase is one share, about $100.

- Keep a small HYSA buffer (maybe $5,000 to $10,000) at Ally or wherever you already bank online. This handles the "what if I need cash tonight" scenario so the rest of your cash can sit in SGOV without worry.

- To transfer out of SGOV, sell the amount you need, wait one day, then transfer to your bank account. Very easy and painless.

One caveat. The dollar difference between SGOV and an HYSA only gets meaningful above roughly $30,000 to $50,000 in cash. Below that, we'd say the juice isn't really worth the squeeze, but the habit is. If you're a resident with $5,000 in savings, open the Schwab account and buy a few shares of SGOV anyway. When your cash balance triples at attending, you'll have the playbook in muscle memory. Start practicing how you eventually want to play.

Enjoy those extra dollars, doctors. Talk again soon.

Sources

Data

- iShares SGOV Fund Fact Sheet (12/31/2025)

- Doctor of Credit: Best High-Yield Savings Account Rates

- FDIC National Rates and Rate Caps

- FRED Consumer Price Index (CPIAUCSL)

Policy

- 31 U.S.C. Section 3124: Exemption from Taxation (Cornell LII)

- IRS 2026 Tax Inflation Adjustments

- Tax Foundation: 2026 State Income Tax Rates and Brackets

Reference