The 2-Minute Version

- The S&P 500 rebounded 15% in Q2, the biggest quarterly rally since 2020. The small sell-off of Q1 fully reversed.

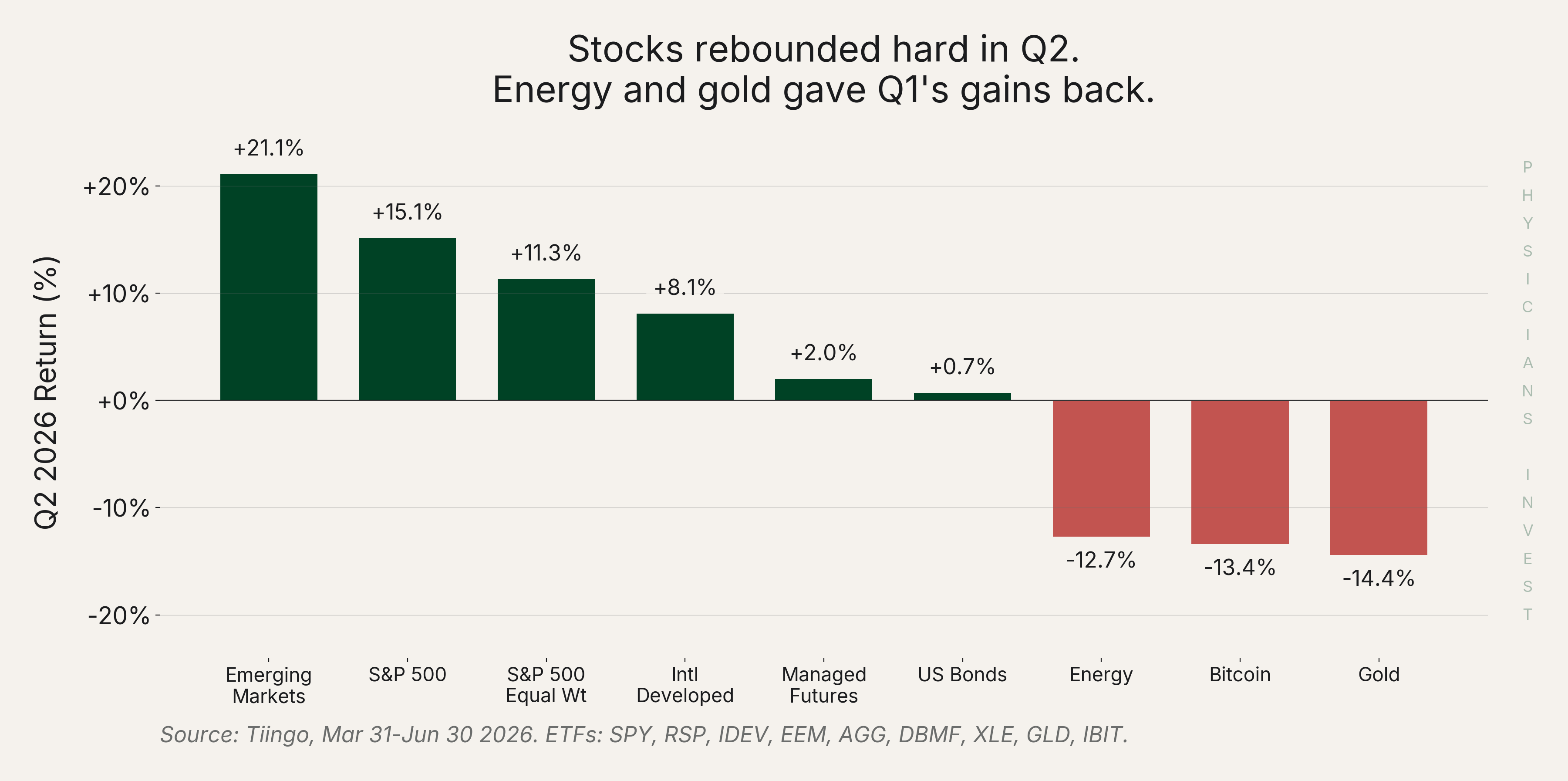

- The exact assets that protected you in Q1 gave it back in Q2: energy down 13%, gold down 14%.

- Managed futures were positive in both Q1 and Q2. Multi-regime performance is what makes them one of the strongest diversifiers a physician can hold.

- The lesson from this year is to hold uncorrelated assets and rebalance opportunistically to take advantage of what the market offers.

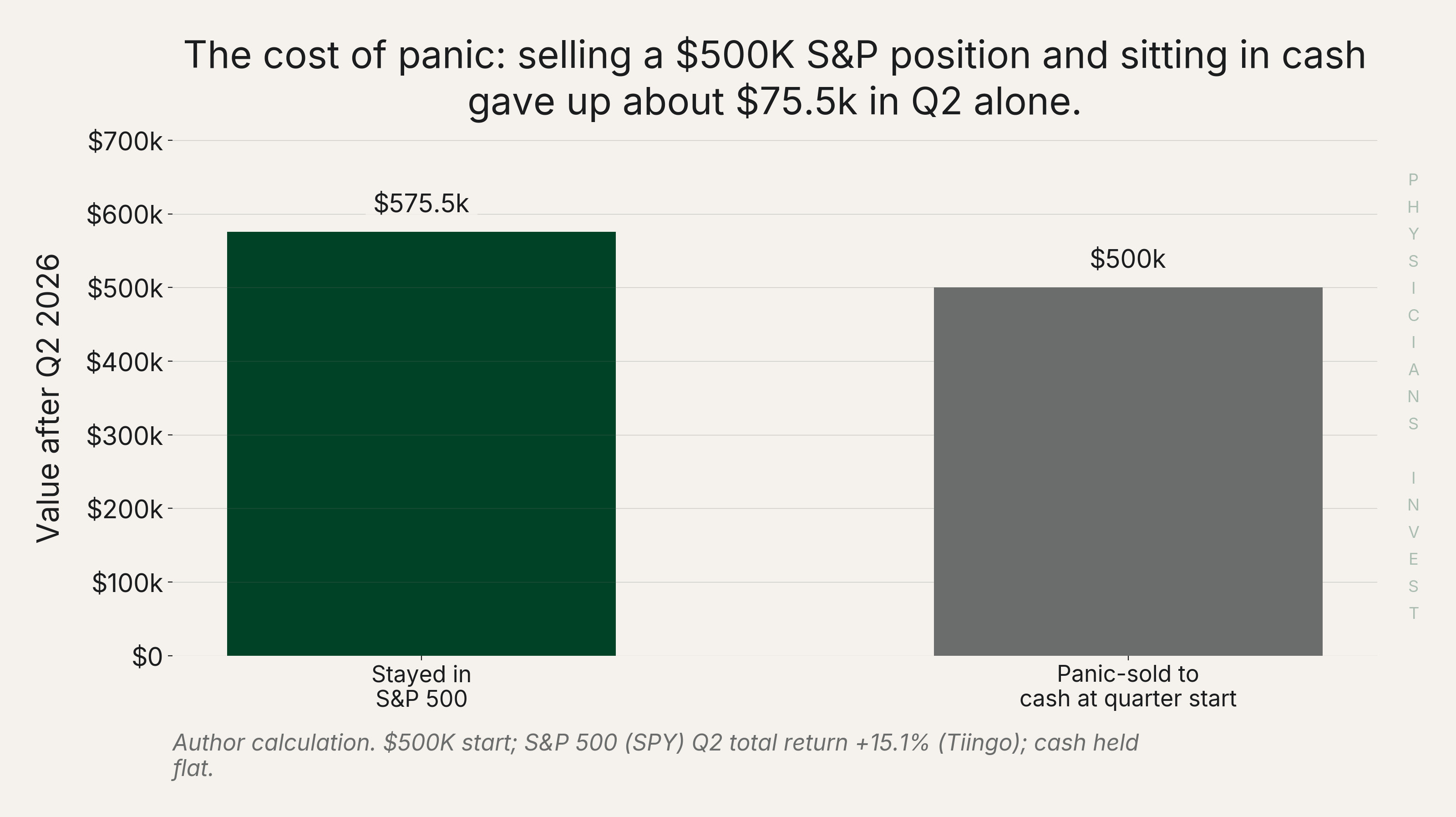

The Dollar Math Panic-selling a $500K S&P 500 position at the start of Q2 and sitting in cash would have cost you about $75,500 in a single quarter. An expensive price for an emotional decision.

Managing your emotions is one of the hardest parts of investing, and it matters most at the extremes. There are three times when investors are particularly vulnerable.

- When times are really good [like right now]

- When times are really bad [like Q1]

- When times are really boring

Today we sit squarely in a regime where things feel really good. Everyone feels wealthier, stocks have been ripping higher, and some stocks have more than doubled over a few short months - such as Micron. This is a time where investors are vulnerable because of FOMO and a time where risks can be obscured. Stay vigilant and continue to make wise decisions.

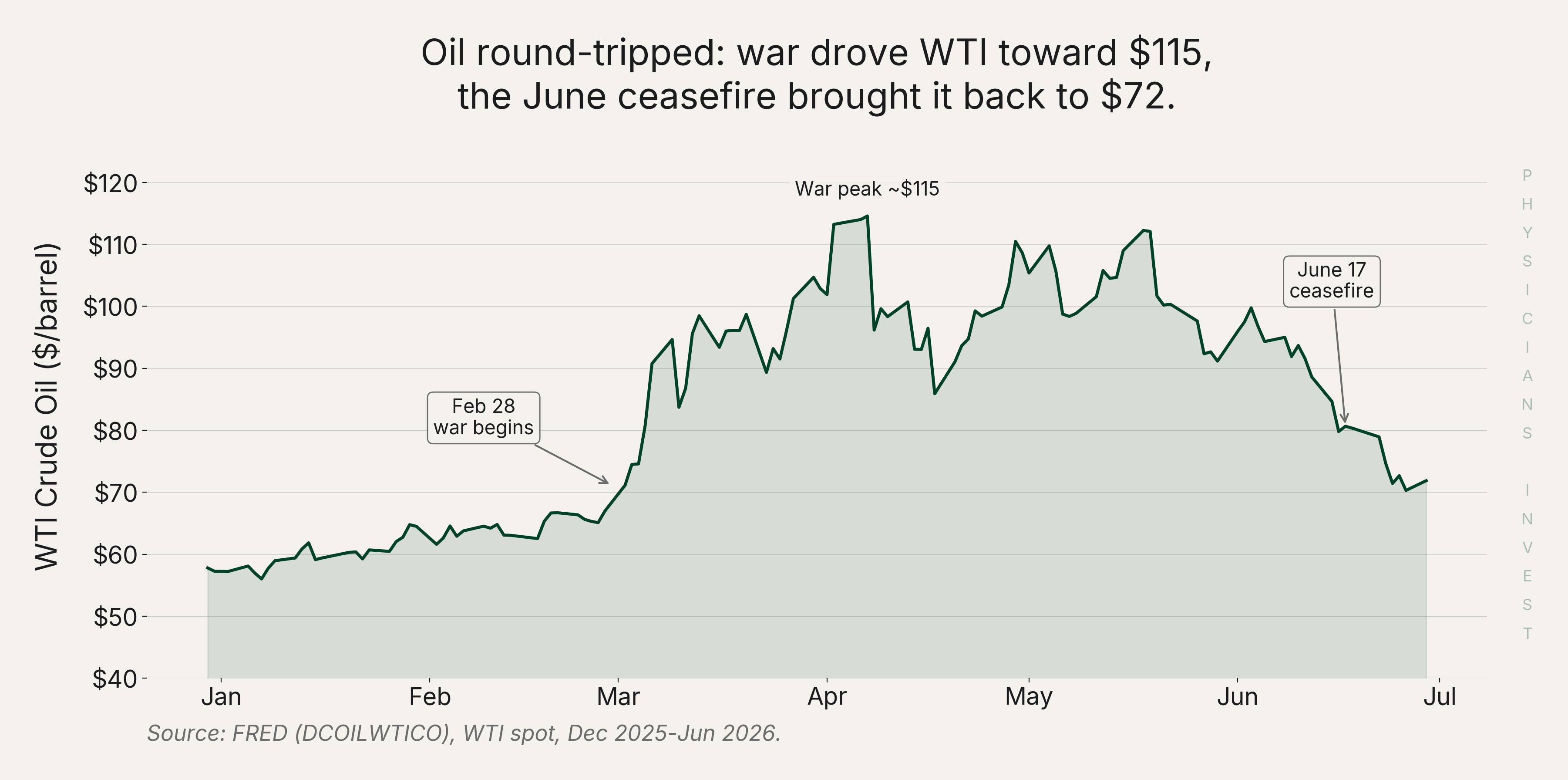

Just 3 months ago the mood was quite the opposite. Many investors watched losses in their accounts pile up as war in the Middle East sent oil to nearly $115 a barrel and stocks down. Then Q2 did a complete flip. If you reacted to Q1 by selling stocks and piling into gold and energy, the market just handed you an expensive lesson. In April we told you two things: build real diversification, and do not panic-sell what you already hold. Q2 proved both.

What happened in Q2

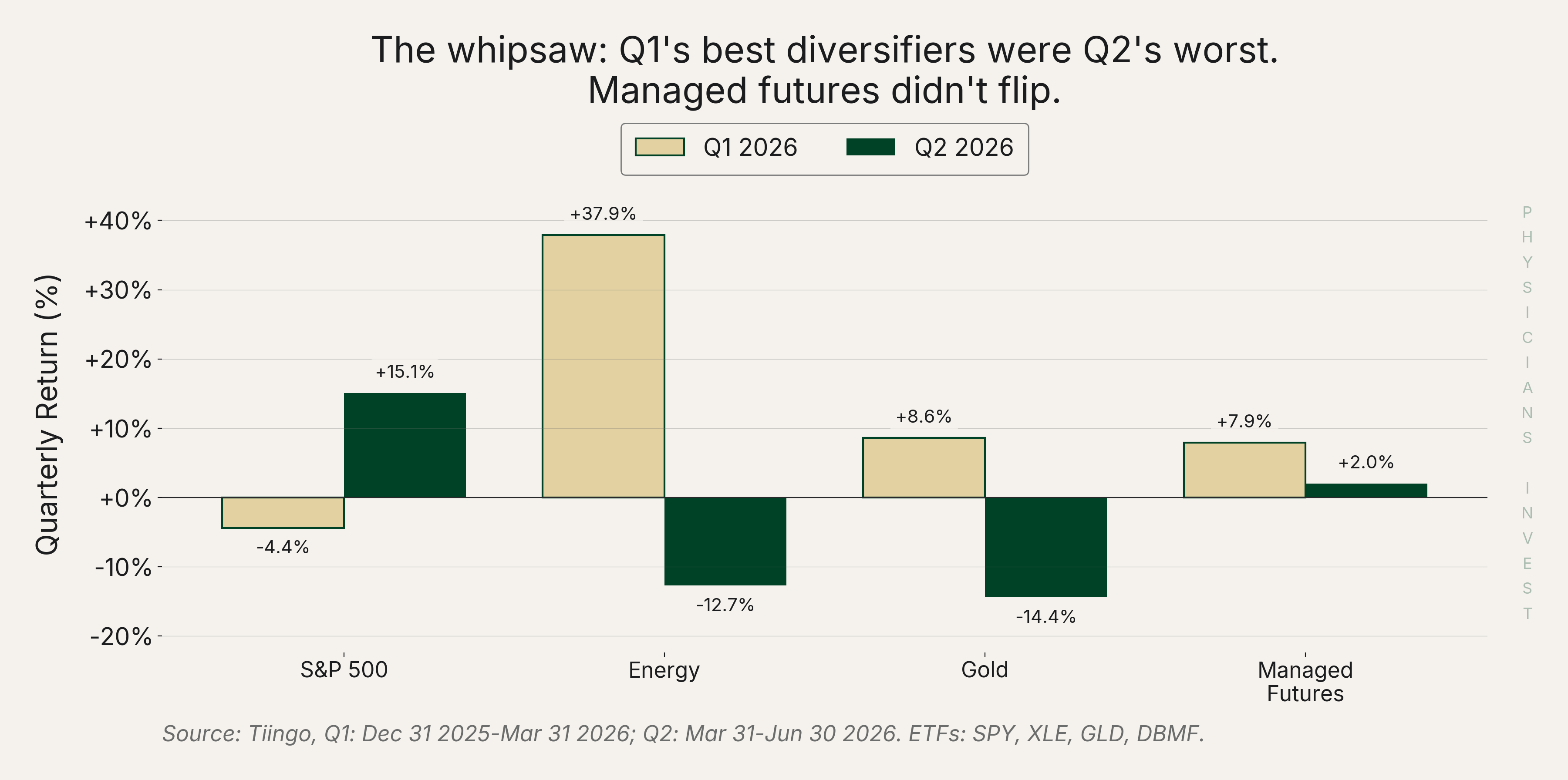

For equity markets, Q2 was a sharp V-shaped recovery off the late-March bottom. The S&P 500 returned 15.1%, its biggest quarterly rally since the post-pandemic rebound of 2020. Emerging markets did even better at 21%. The assets that carried Q1 such as energy and gold, on the other hand, went into reverse and gave back most of their Q1 gains. The bar chart below shows Q2 performance by asset class.

Oil has been a headline this year. The driver of oil prices has been primarily the war and many thought oil would go much higher for much longer than it has. Overall, this administration has a strong desire to keep oil prices contained and it seems like they have managed to do just that even in the face of a significant supply shock with the closure of the Strait of Hormuz. A June 17 ceasefire reopened the Strait of Hormuz, and oil round-tripped from its April peak near $115 back to about $72. We would expect to see moderate tightness in oil markets through the rest of this year, which should provide some support to the floor of the price.

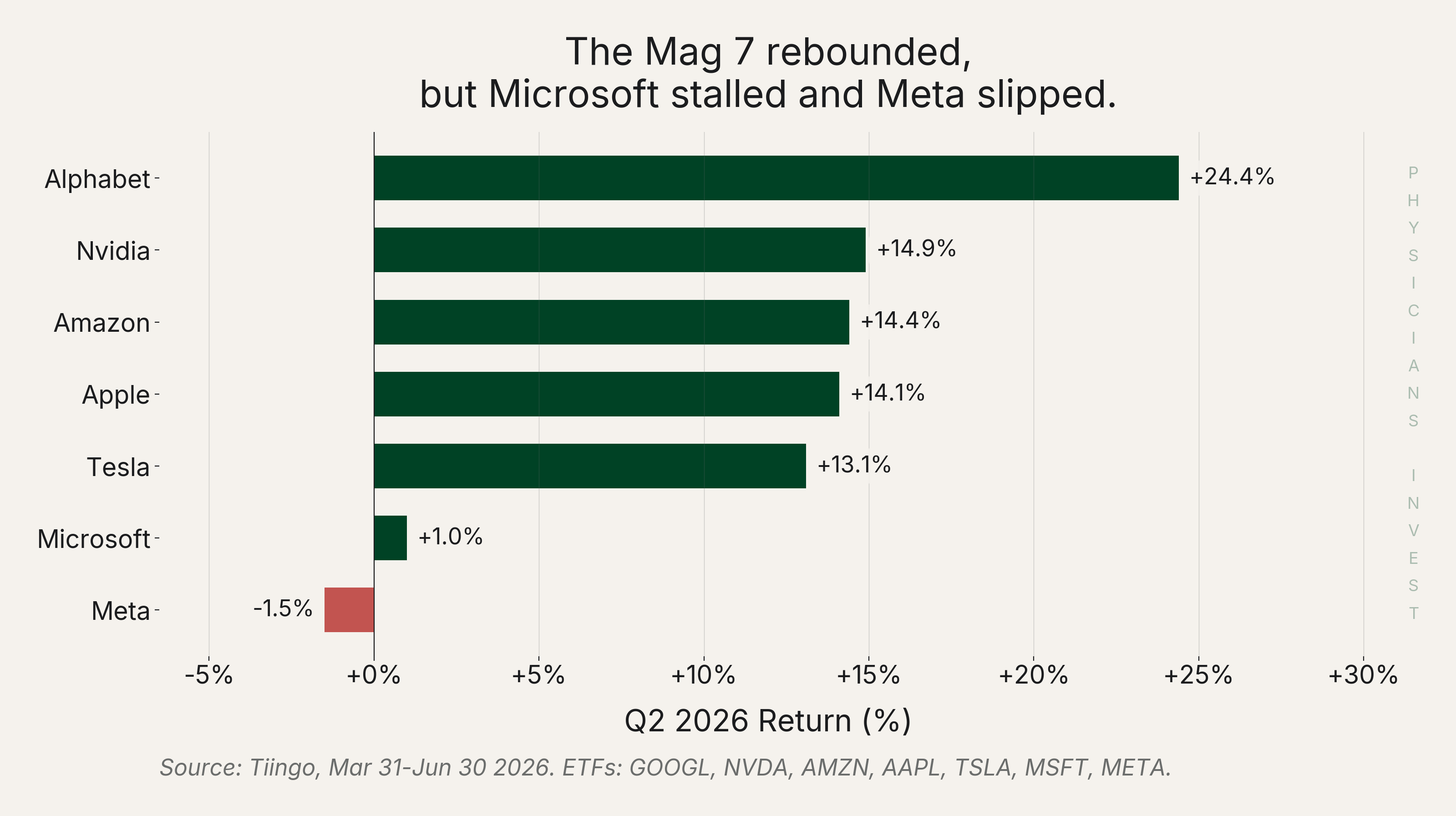

Mega-caps continue to relentlessly power forward and had a very strong quarter. Technology led the rebound, though not uniformly as META slipped. Alphabet gained 24% and Nvidia 15%, while Microsoft was flat.

The whipsaw: Q1's best diversifiers were Q2's worst

Q2 is a perfect case study for the importance of intelligent asset allocation. The exact assets that protected you in Q1 were the ones that hurt you in Q2. Energy went from up 38% to down 13%. Gold went from up 9% to down 14%. By holding multiple asset classes that are uncorrelated to each other and then opportunistically rebalancing you can take advantage of swings in the market. For example, when equities were down in Q1 and energy and gold were up, you could have opportunistically rebalanced out of energy and gold and into equities. This is a beautiful way to invest because it takes full advantage of every regime the market decides to throw at investors. For those that just hold equities, the opportunity to rebalance into uncorrelated assets doesn't exist which hurts long-term compounding, especially in times of stress like 2022.

Managed futures worked in both quarters

Managed futures returned about 8% in Q1 and stayed positive at 2% in Q2. Up when stocks fell, and still up when stocks ripped higher. Many academic papers identify managed futures as one of the best diversifiers for portfolios yet few people use them as an asset class. This has always been curious to us. We feel strongly that all investors should include managed futures in their portfolios at a significant weight (not just 5% or less). Managed futures dynamically adjust to what markets are doing, which is why it can hold its ground across opposite quarters that had two very different regimes. It has a near zero correlation (a measure of how closely two assets move together) with equities and a near zero correlation with bonds, and tends to perform best in times of market stress. The exact sort of asset you want to hold.

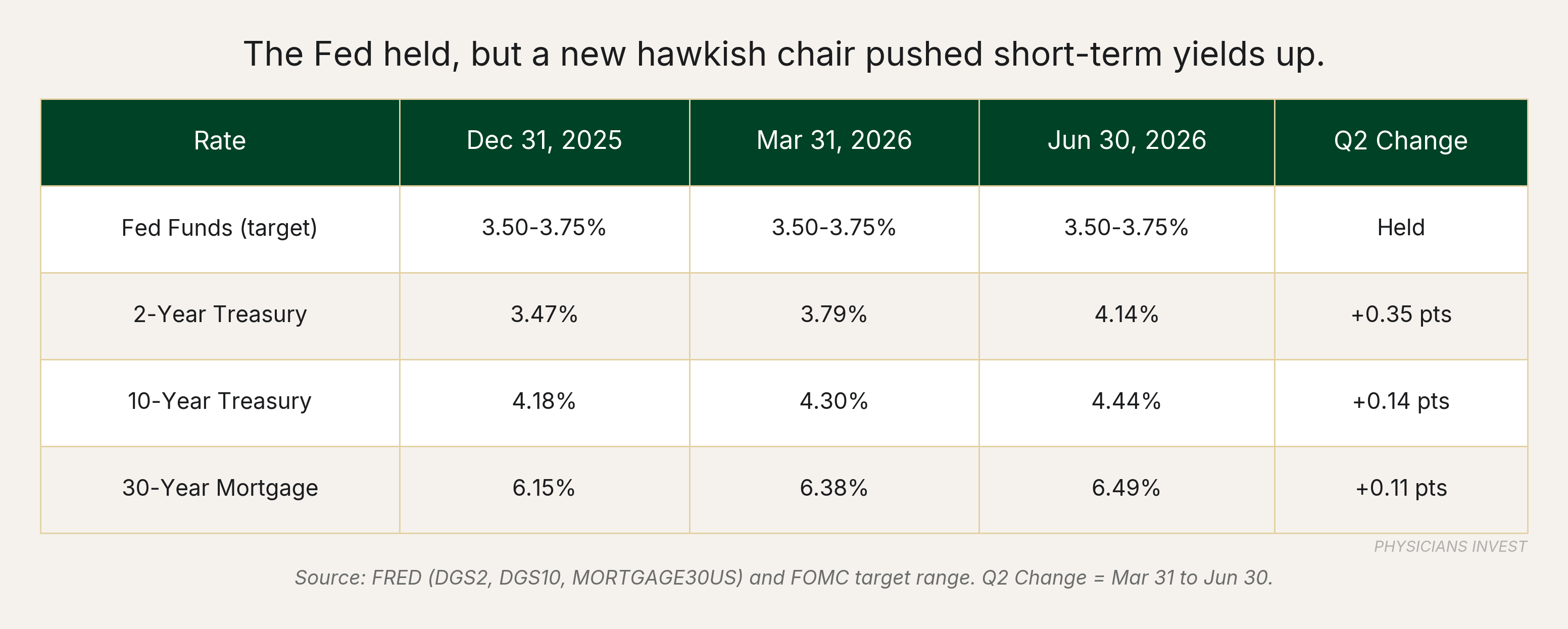

Bonds still did not hedge, for a new reason

Bonds were flat again this quarter, up just 0.7%. In Q1 bonds didn't perform because inflation fear pushed yields up. In Q2 bonds lack of performance was mostly because new Federal Reserve leadership that has so far proved to be more hawkish than many expected. New Fed chair Kevin Warsh held rates steady, removed the language signaling future cuts, and the Fed's own projections now flirt with hikes rather than cuts. The two-year Treasury yield jumped about a third of a percentage point over the quarter, basically a market induced rate hike.

At current rates bonds are a reasonable place to hold money you will need soon, but they are not a growth engine and should not be expected to be a strong hedge to your equity positions over the coming quarters.

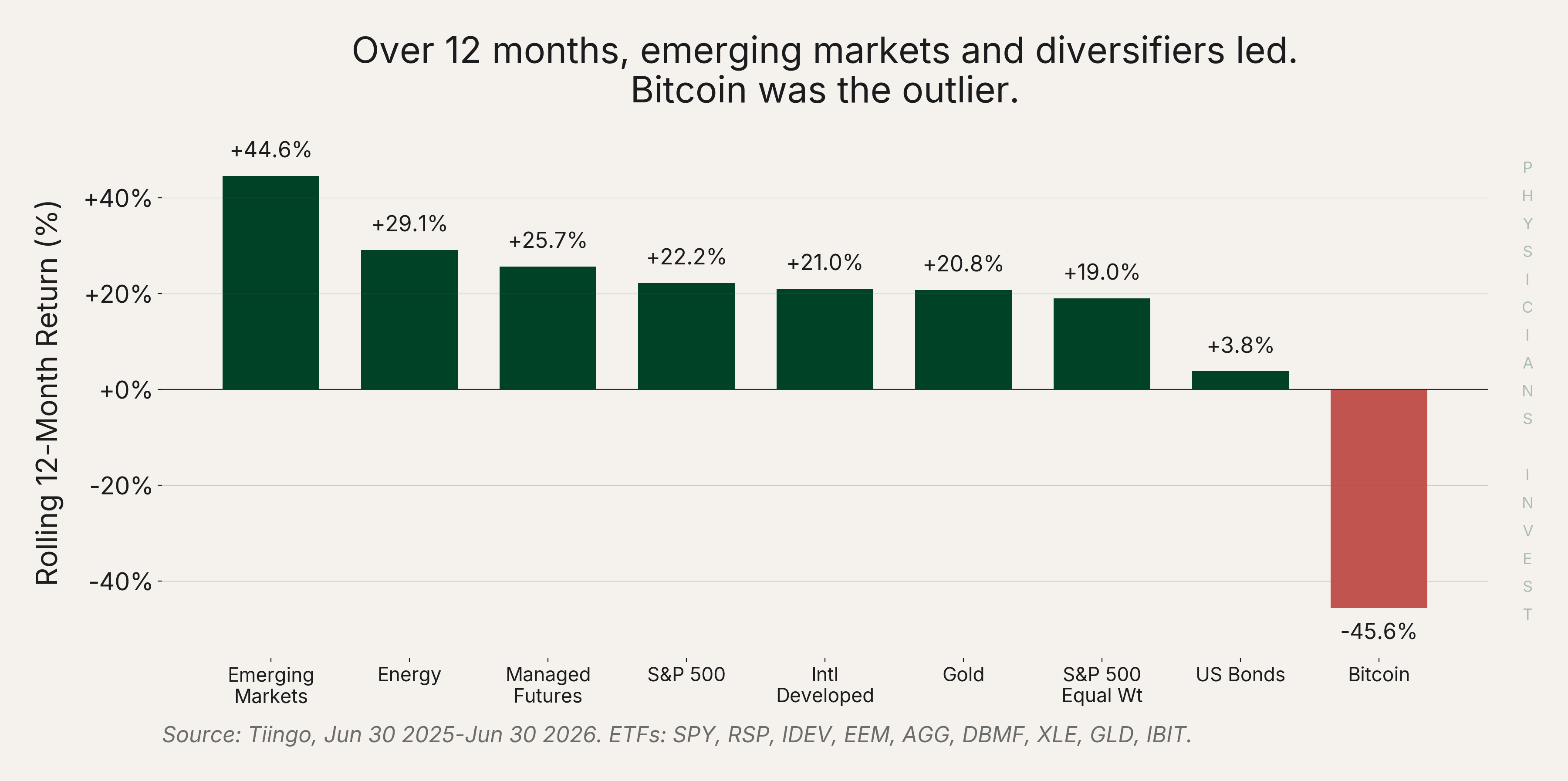

Zoom out: twelve months of context

Over the past twelve months, everything has been looking good - sans Bitcoin which has had a face-melting selloff. It is always a siren's call to get caught up in the short term gyrations of markets, and quarter end is always a good reminder to zoom out and to position yourself as a long-term investor. Own uncorrelated assets, rebalance opportunistically, and hold all of them for a very long time.

The Move

- Do not performance-chase. The winners often rotate every quarter. Q1's heroes were Q2's losers. A takeaway for investors today, know that the tech stock eye-popping performance can go on for a while but it will not last forever.

- Rebalance on a schedule or on rules, not on emotion. A simple calendar rebalance would have trimmed the Q1 spike in energy and gold and added to beaten-down stocks near the bottom. It captures the whipsaw in both directions without you having to make big bets about anything.

- Hold genuinely uncorrelated assets, such as managed futures. A diversifier that adapts across regimes, like managed futures, does more for you than trying to time equity markets.

- Moderate your expectations for bonds. We would not position a bond allocation for cuts a new hawkish Fed may not deliver. This isn't an environment where we'd extend duration (how sensitive a bond's price is to rate changes), and we'd lean toward a lighter bond weight.

- Build a portfolio you do not have to watch daily. Your goal is not to call the next week or the quarter. It is to own an allocation that works for decade long periods that is tax advantaged and low-overhead.

Sources

Data

- Tiingo API -- ETF and equity adjusted close prices (SPY, RSP, IDEV, EEM, AGG, DBMF, XLE, GLD, IBIT, Micron (MU), and the Magnificent 7)

- FRED -- Treasury yields (DGS2, DGS10), Fed funds rate, 30-year mortgage (MORTGAGE30US), WTI crude spot (DCOILWTICO)

Analysis

- Federal Reserve FOMC statement, June 17 2026 -- rate hold, removal of easing bias

- FactSet S&P 500 Earnings Season Preview, Q2 2026 -- Q2 earnings growth tracking ~23%

- AQR: "A Century of Evidence on Trend-Following Investing" -- long-run managed futures evidence

News

- Al Jazeera -- Oil prices and the Strait of Hormuz (June 29 2026) -- June 17 ceasefire, oil round trip

- CNBC -- Fed interest rate decision, June 2026 -- Warsh first meeting, hawkish tone

- The Motley Fool -- "2022 Was the Worst Year Since 1937 for This Investing Strategy" -- stocks and bonds falling together in 2022

Related from Physicians Invest