The 2-Minute Version

- The energy sector is 4% of the S&P 500 today, down from over 13% in the early 1990s. Most physicians only own index funds so they are systemically under-exposed to energy.

- Four ways to add deliberate exposure: public ETFs (exchange-traded funds), individual stocks, private working interests, private mineral interests.

- For most physicians, an energy ETF (like XLE) at 3-7% of the portfolio is the right answer. Private deals can work, but only with a competent operator and an attractive opportunity.

Energy is a mere 4% of the S&P 500 today, down from over 13% in the early 1990s. Most physicians only have exposure to the sector through their index holdings. This makes them systemically underexposed to the asset class and that may or may not be a problem worth solving.

The Setup

At some point in their career physicians will be pitched a private oil and gas deal. Why? Physicians are targets for these deal marketers because physicians have high W-2 income, have accredited-investor status, and have strong interest in reducing taxable income.

I spent seven years as a petroleum engineer at EOG Resources and have invested in both private mineral and working-interest deals personally. From those experiences, I have strong feelings about how physicians should approach these deals. Two questions need to be answered:

- Should you invest in more energy exposure?

- If yes, what is the best way to get that exposure?

Should physicians have more energy exposure?

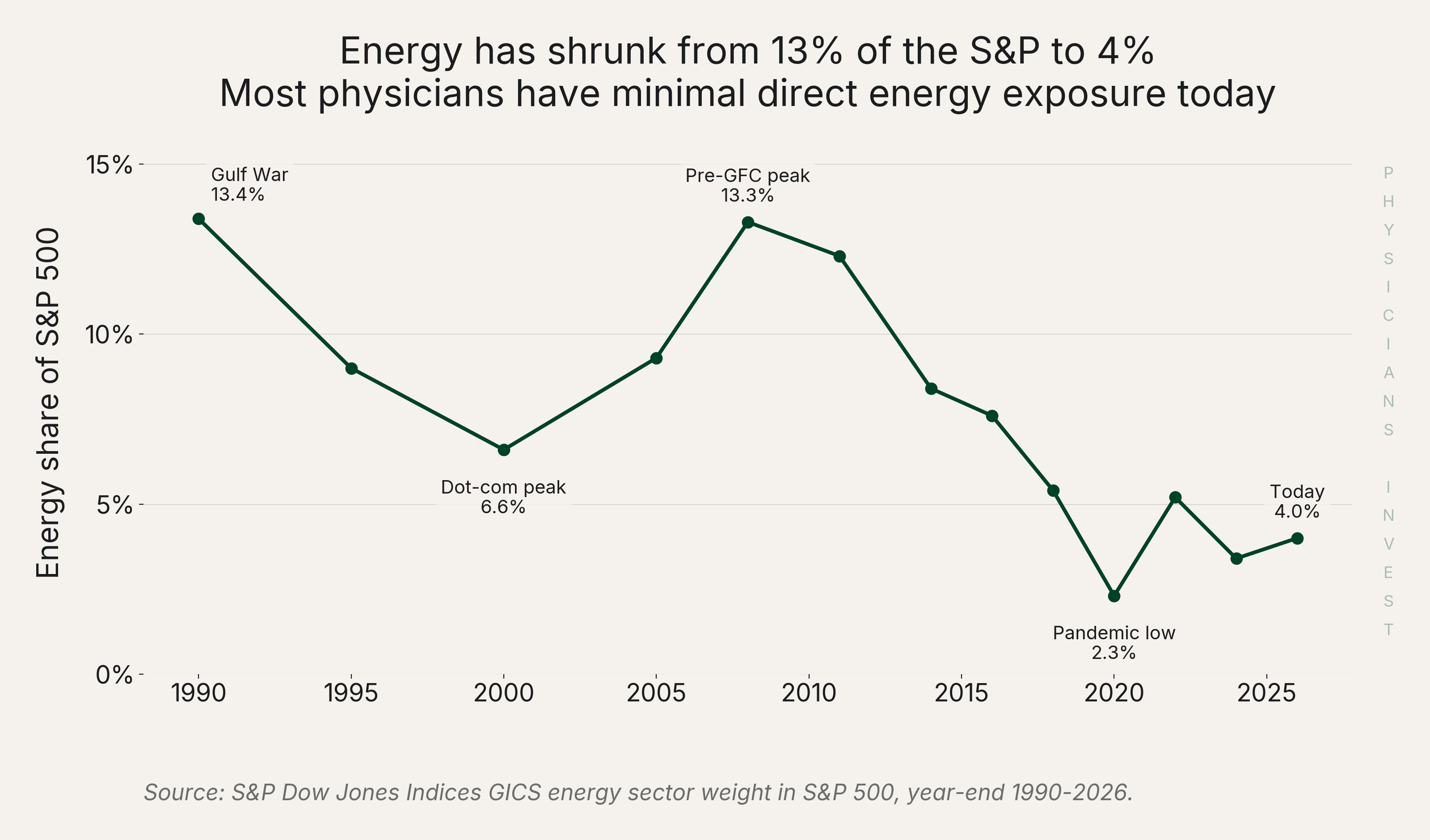

Most physicians sit in broad index funds like VTI or VOO and have 4% exposure to the energy sector by default. This puts energy, a core economic sector, on the low end of exposures compared to the others that make up the S&P 500. Especially tech. Not adding a deliberate allocation to energy is an active bet that it will underperform other sectors over the coming years. The chart below shows the shrinking exposure the S&P 500 has had to energy over the years.

Source: S&P Dow Jones Indices, Westmount Fundamentals.

Source: S&P Dow Jones Indices, Westmount Fundamentals.

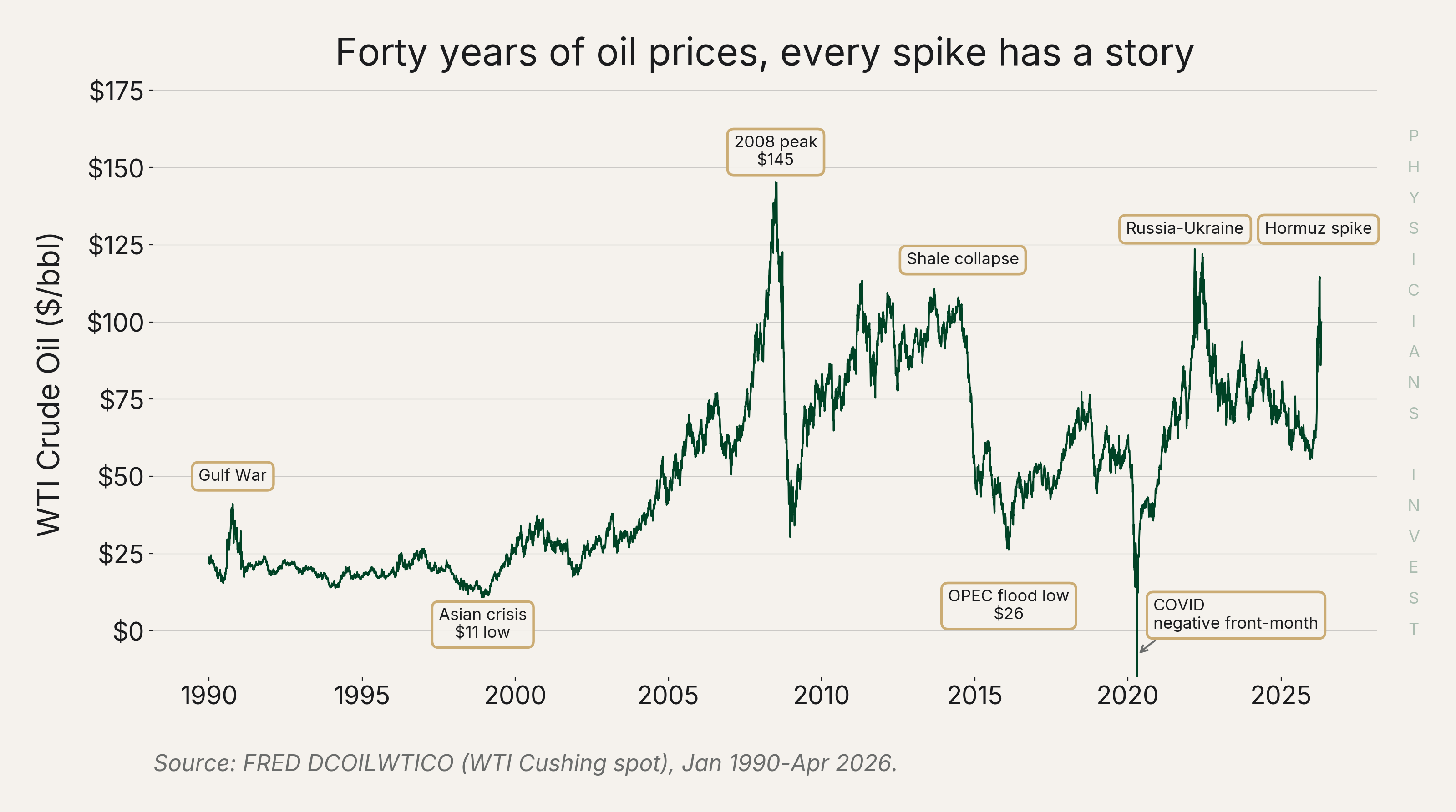

There is a legitimate case to be made that energy will be a crucial sector moving forward into the age of AI and that it deserves a spot in your portfolio. Energy sells a commodity whose price tends to rise with inflation, which makes the sector structurally inflation-resilient. 2022 was a perfect example of this. The chart below shows oil prices through major macro events, including the 2022 spike.

Source: FRED, DCOILWTICO daily WTI front-month spot.

Source: FRED, DCOILWTICO daily WTI front-month spot.

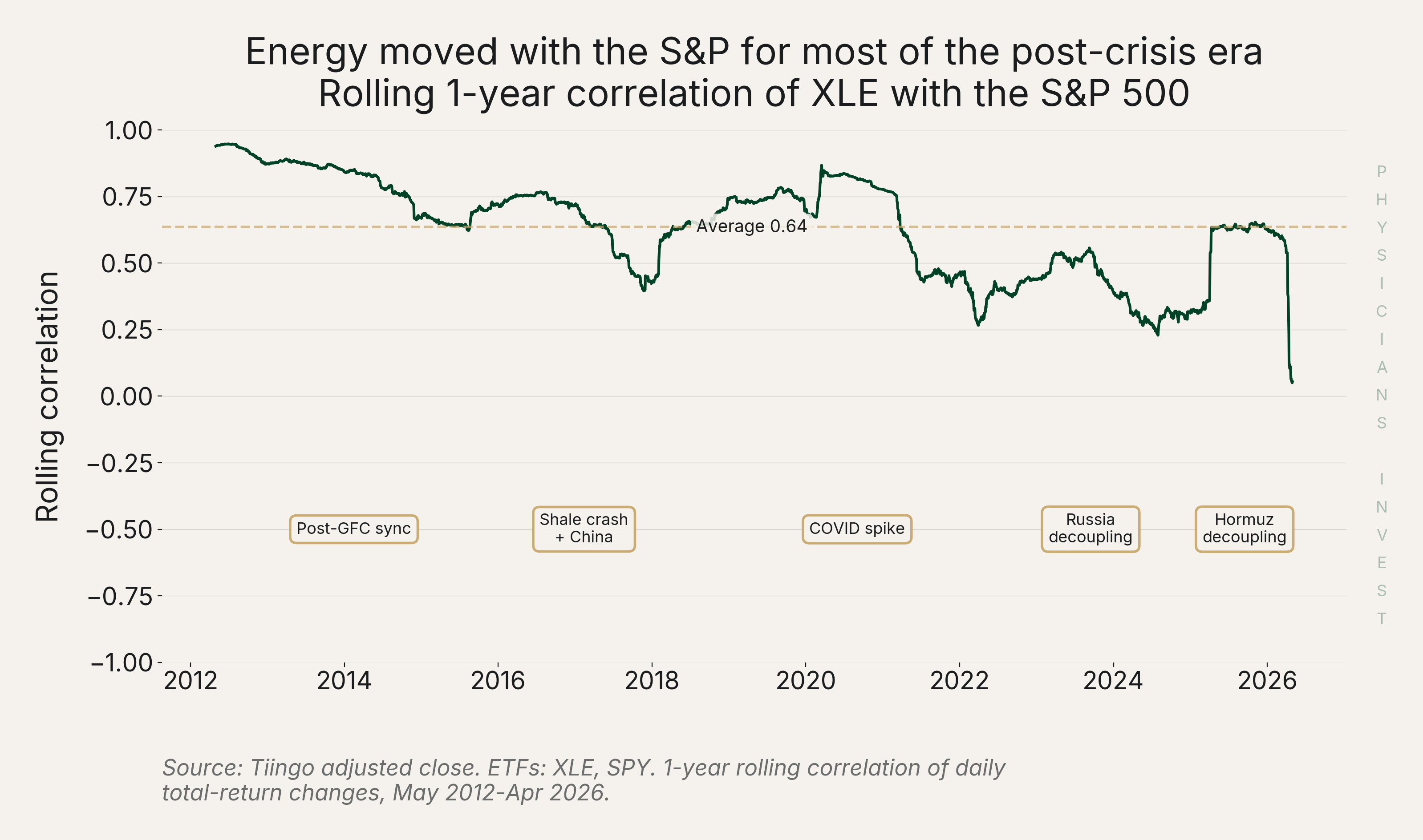

Another reason for owning the sector is that energy can act as a diversifier when its correlation (how closely two assets move together) breaks down with the broader equity market (see plot below). Q1 of this year is a perfect example of this. In addition, the companies that drive the sector have also been more shareholder-friendly post-COVID. Here are a few examples:

- Adherence to capital discipline, meaning that they are more selective on the projects they pursue

- Aggressively paying down debt, meaning they are more resilient to future shocks

- Returning cash at record levels through dividends and share buybacks, meaning they are investor focused

Source: Tiingo. 2-year rolling correlation, daily returns.

Source: Tiingo. 2-year rolling correlation, daily returns.

The case against owning energy is just as honest. Energy is volatile and 50% drawdowns (drawdown = peak-to-trough decline) are normal. It has also underperformed the index over the last 20 years. That could continue if the large tech companies continue their dominance.

As far as allocation goes, the reasonable exposure is 3-7% on top of the broad index. Every physician situation is different, but this is how I personally think about it. That's my mental model; your situation will differ, and a financial advisor can help you size this for your own plan.

How do you actually get exposure?

The next question is how. There are few main vehicles:

Vehicle 1: Public energy ETFs.

- XLE: Large-cap energy stocks like Exxon and Chevron, more stable.

- AMLP: Pipeline MLPs in a C-corp ETF wrapper. This is important because it skips the K-1s and IRA UBTI problem, though the wrapper carries a 1-2 percentage point annual tax drag from federal income tax inside the fund.

- XOP: Smaller E&P names, more volatile.

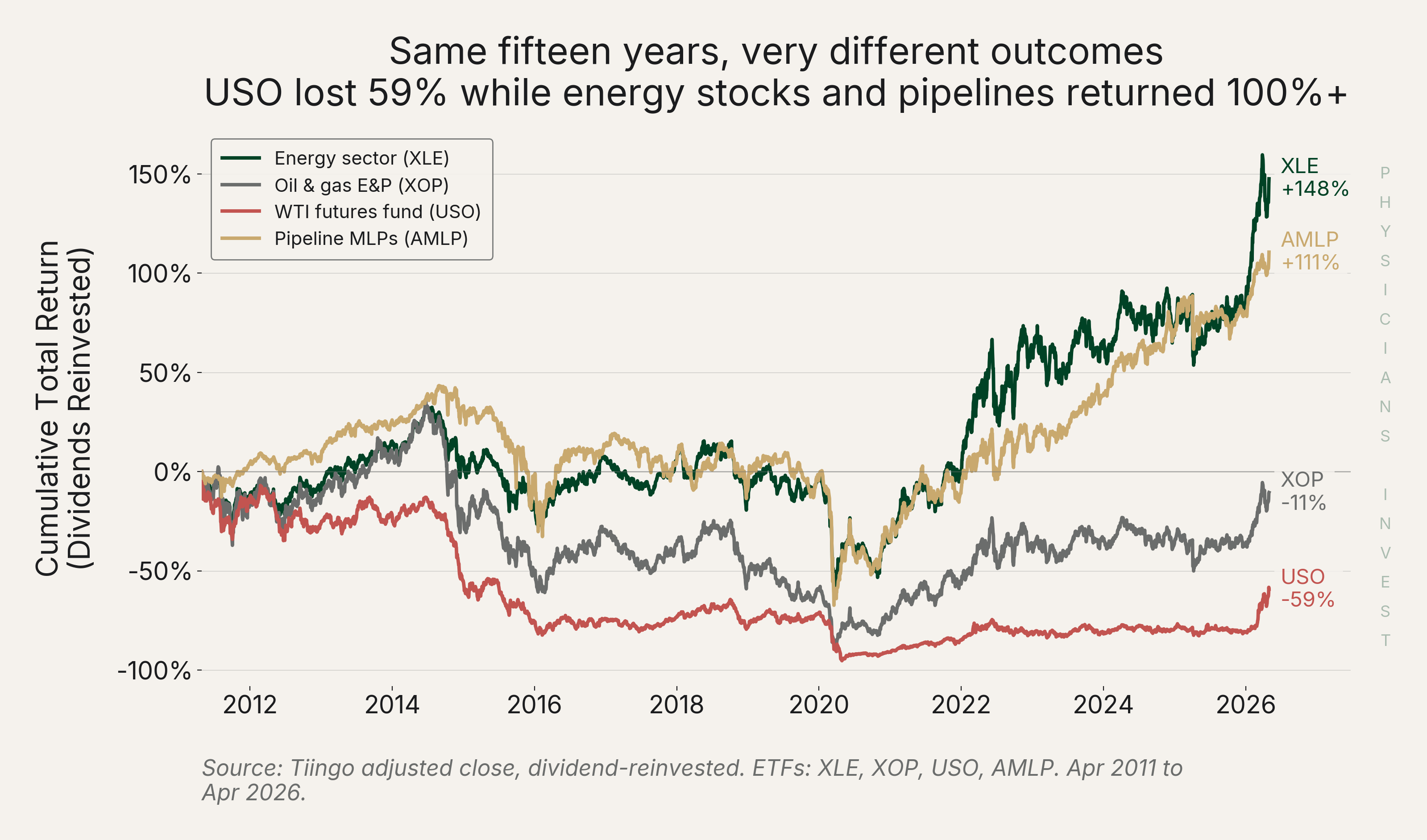

- USO: Skip USO. It bleeds in contango (when later-month futures cost more than front-month, so the fund sells low and buys high every roll). It has lost roughly 60% over 15 years even as oil rallied.

Source: Tiingo. Total return assumes dividends reinvested.

Source: Tiingo. Total return assumes dividends reinvested.

ETFs are liquid, low-fee, and have diversified operator-quality risk. They should be the default for most physicians. (XLE is one example; FENY, IYE, and others do similar work.)

Vehicle 2: Individual energy stocks.

Pick stocks directly. ExxonMobil, Chevron, EOG, ConocoPhillips, Enterprise Products, and many more. These are for targeted exposure and carry more risk than the ETF path. Tradeoffs include single-name risk and more management. This route fits physicians who already pick stocks elsewhere and are comfortable with fundamental analysis.

Vehicle 3: Private working interests. You put up capital and become a partner in a partnership that drills specific wells.

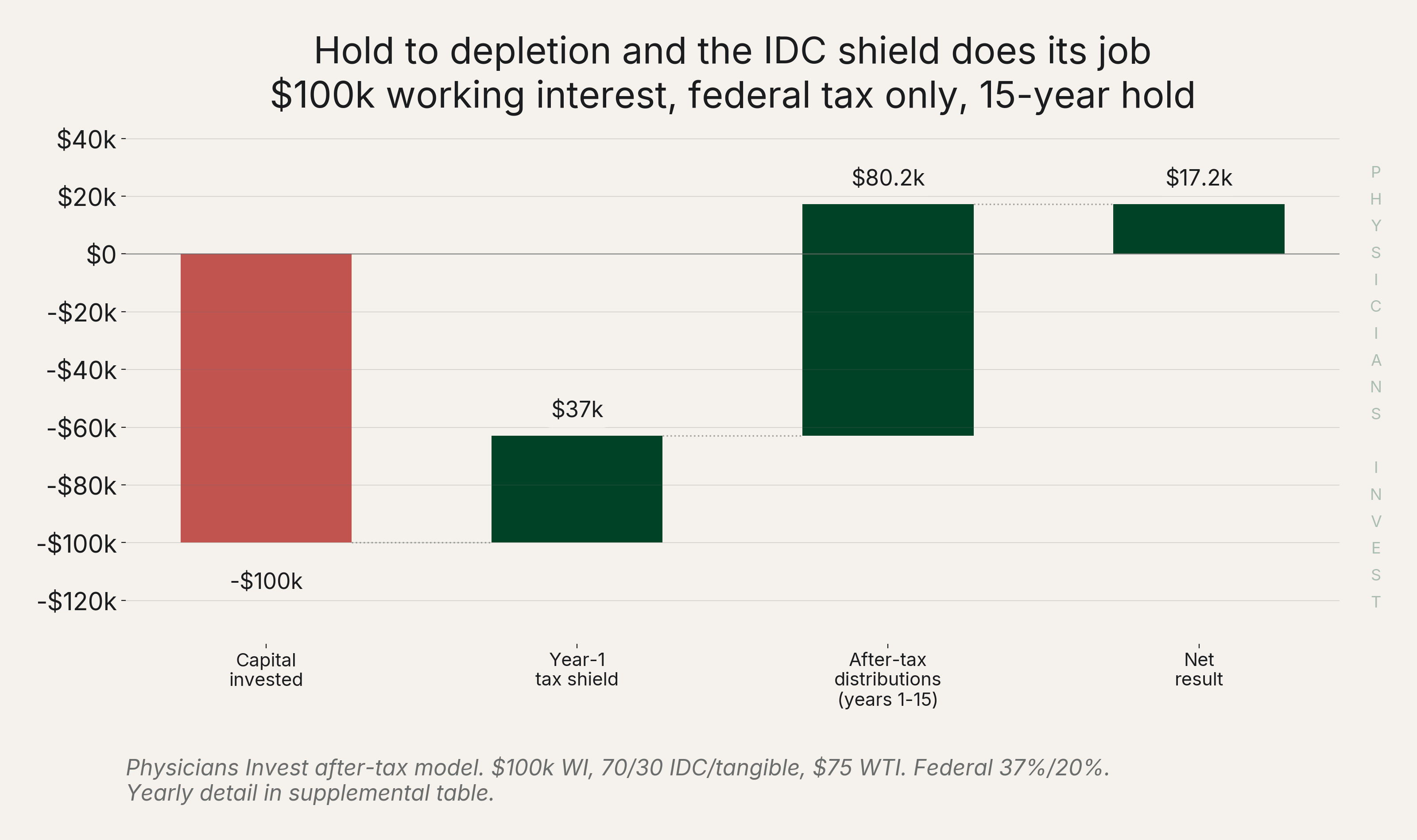

Private working interest comes with significant tax advantages as it is one of the few investments that can actively reduce taxable W-2 income. On $100k with a typical 70/30 IDC/tangible split, an investor in 2026 can deduct close to the full $100k in year one. About $70k as intangible drilling costs (§263(c)) and $30k as bonus depreciation (§168(k), permanently restored at 100% by the One Big Beautiful Bill Act (OBBBA) for property placed in service after January 19, 2025). For a top-bracket physician this is roughly $37k of immediate federal tax savings. The waterfall plot below shows this mechanism. The specifics depend on how the partnership structures the deal -- run the numbers with your accountant before committing.

Source: Physicians Invest model. $100k invested, 70/30 IDC split, 37% top federal bracket, $75 WTI.

Source: Physicians Invest model. $100k invested, 70/30 IDC split, 37% top federal bracket, $75 WTI.

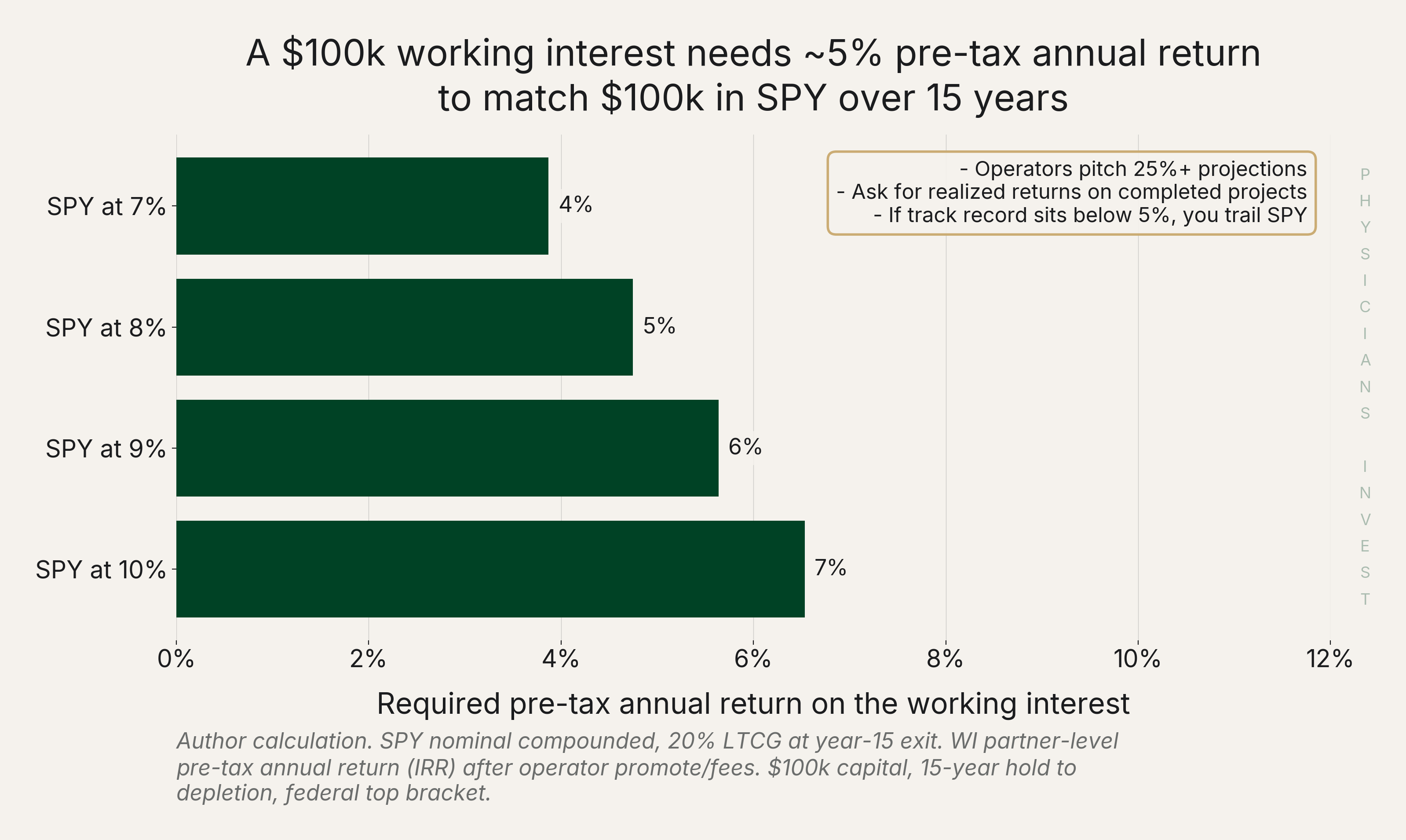

But the math can't end there. The $37k that otherwise would have gone to taxes can now be invested elsewhere. I'll assume that's the S&P 500 through the SPY ETF. With the tax shield compounded into SPY for 14 years, what does the underlying working interest investment have to clear pre-tax to match $100k in SPY if I had never invested in the working interest deal?

Source: Physicians Invest model.

Source: Physicians Invest model.

About 5% pre-tax annual return is what the private deal needs to deliver. Sounds easy, but in practice many working interest deals never get there. EOG is known as one of the better operators, and we still had to grind to make sure that everything was efficient. And that's with some of the most capable people in the industry. Shops with less experienced teams face serious hurdles when it comes to drilling wells profitably. Some end up getting a little bit lucky, and that bails them out. The ones who don't get lucky end up going under or incinerating capital.

Working interests are illiquid, operationally exposed (time with the well not being drilled is time lost on the capital committed), tax-complex (§1254 recapture turns those deductions back into ordinary income on disposition), and carry liability exposure. A general partner can be on the hook for environmental and operational obligations, not just the capital. The exact liability structure depends on how the deal is organized -- confirm GP vs. LP treatment before signing. This is important to understand before ever entering one of these deals.

If you go this route, use these general filters:

- No first-time operators. They should point to prior funds and show realized returns.

- Basin-specific experience. Permian, Eagleford, and Anadarko aren't interchangeable.

- Break-even test. Ask them what the break-even oil price is for the project (assume $2.50 gas). If they tell you a number less than $50/barrel, you immediately know that they either don't know what they are talking about or they are lying. Almost no one runs economic projects below $50/barrel in U.S. unconventional.

- Follow-along test. Ask them if you can sign an NDA and follow along with the project they are pitching today in hopes to invest in their next one. If they aren't willing to do this, they probably aren't worth investing in ever.

- Tax-first pitches. If they pitch tax advantages first...run. This is a signal they are just focused on retail investors and not institutional investors who are tax-exempt. You want the project economics to be great before accounting for any tax advantages.

The industry is littered with either bad actors or incompetent actors. This filter matters tremendously for any sort of private oil and gas investment.

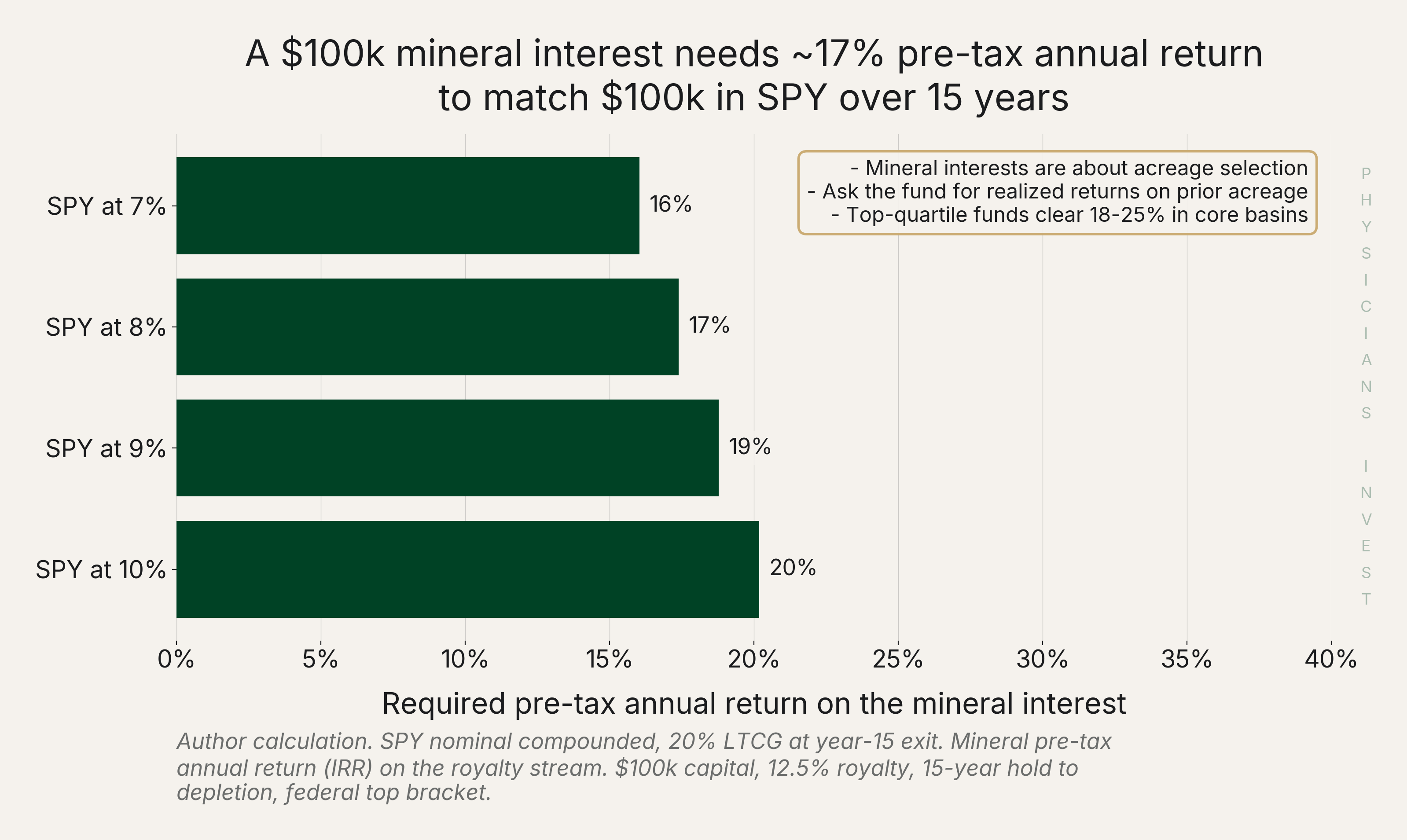

Vehicle 4: Private mineral interests. You own the mineral rights under acreage and collect a royalty (typically 12.5-25%) on production. Someone else operates. No upfront tax shield like in the working interest path above (you didn't drill, so you weren't "actively" exposed), but you do get 15% percentage depletion on royalty income going forward. Your accountant can walk through what that means. Without the year-one head-start from the tax write-off, the bar to match SPY is higher.

Source: Physicians Invest model.

Source: Physicians Invest model.

About 17% pre-tax annual return is what's needed to make minerals make sense. That's a high hurdle and means you should do ample due diligence before getting into a mineral deal. Royalty income from minerals is considered ordinary income from a tax perspective, and most pay out checks monthly. I personally invested in a Permian mineral fund (their 8th fund, decades of basin experience, transparent on prior returns) that has produced low double-digit returns. Keep in mind that past results are not indicative of future performance, and Physicians Invest has no referral arrangement with this fund -- to be clear, we're not endorsing any specific fund here. Mineral interests fit physicians who want energy without operational dependency, plus monthly income. Minerals can be thought of as somewhat similar to a rental real estate investment from a cash-flow and passive-income perspective.

The Move

Treat this decision like a differential diagnosis: simplest path that fits the case, not the most complex.

- Most physicians: XLE or a similar broad energy ETF at 3-7% of portfolio. Simple and easy.

- Physicians wanting named exposure. Add a few large-cap stocks (XOM, CVX, EOG) alongside the ETF.

- Physicians wanting a tax shield and are willing to spend lots of time vetting operators. A private working interest can work, but only after applying the checklist of filters above.

- Physicians wanting passive royalty income without operator risk. A private mineral fund with a long track record. Apply the same checklist for working interest before allocating any capital.

- Skip. USO. Individual Pipeline MLPs in an IRA. First-time operators. Any private deal that leads with the tax break instead of project economics.

Sources

Data

- Westmount Fundamentals — S&P 500 Sector Weights 25-Year Rotation -- energy sector weight over time, including 4% current and historical 13% peak

- FRED DCOILWTICO — WTI Crude Oil Spot Price -- 40-year WTI price history

- Tiingo — XLE, XOP, USO, AMLP, SPY total returns -- 15-year ETF total return comparison; rolling correlation chart

- 24/7 Wall St — "USO Is Up 64% This Year and Still Losing the Long Game" -- USO 15-year cumulative loss figure

- CME Group — "Implications of WTI Oil Futures In Backwardation Amid the Supply Crunch" -- 42% contango / 58% backwardation stat (1985-2026, front-month vs. 6-month)

Tax & Legal

- 26 CFR § 1.612-4 — Intangible drilling costs, §263(c) (Cornell LII) -- statutory basis for 100% IDC expensing in year one for working-interest holders

- 26 U.S. Code § 1254 — Recapture of natural resource deductions (Cornell LII) -- §1254 recapture mechanics; ordinary-income recharacterization on disposition

- 26 CFR § 1.1254-1 — Treatment of gain from disposition of natural resource recapture property (Cornell LII) -- definition of "disposition" and partnership-level recapture rules

- 26 U.S. Code § 613A — Limitations on percentage depletion, oil and gas wells (Cornell LII) -- 15% percentage depletion for independent producers; 1,000 bbl/day small-producer cap

- BDO — "One Big Beautiful Bill Act Expands 100% Depreciation Expensing Opportunities" -- OBBBA permanent restoration of 100% bonus depreciation under §168(k)

- Moss Adams — "How the New Tax Laws Benefit Oil and Gas" -- confirmation that OBBBA did not change §263(c) IDC expensing or percentage depletion

- RSM US — "OBBBA tax implications for the energy sector" -- OBBBA bonus depreciation rate and effective date; energy sector applicability

Industry

- SEC / Investor.gov — "Investor Alert: Private Oil and Gas Offerings" -- red flags in private O&G placements

- DW Energy Group — "What Is Intangible Drilling Cost?" -- 70/30 IDC/tangible split rule of thumb for partnership offerings

- Fidelity — "Unrelated Business Taxable Income (UBTI)" -- UBTI mechanics for IRAs holding MLPs