The 2-Minute Version

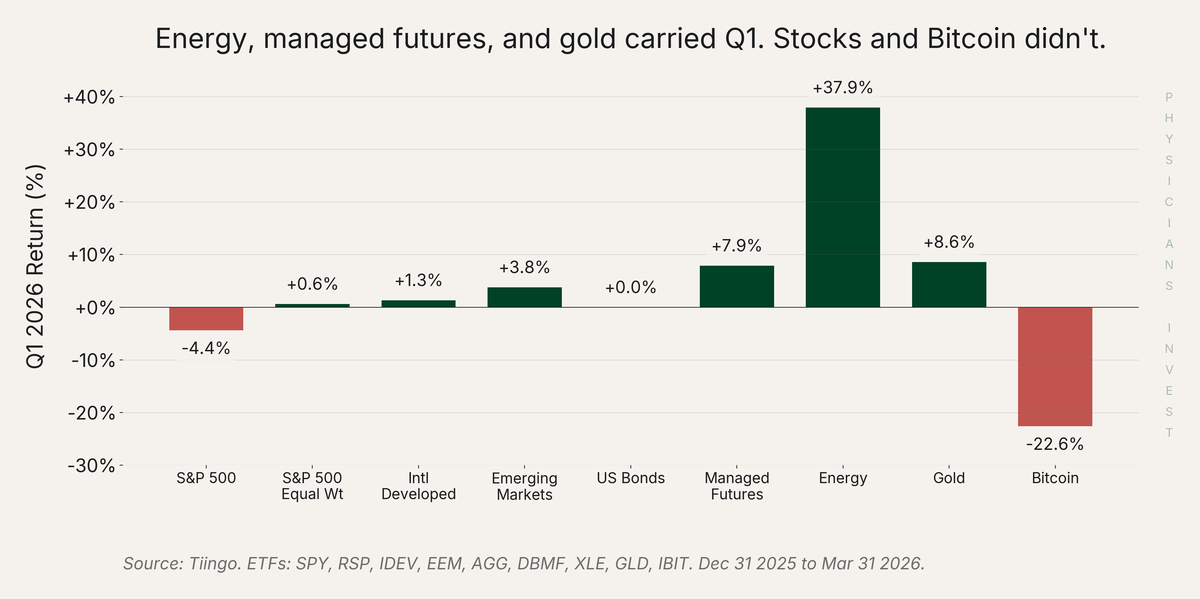

- The S&P 500 fell 4.4% in Q1 while bonds sat flat. The 60/40 portfolio failed to hedge.

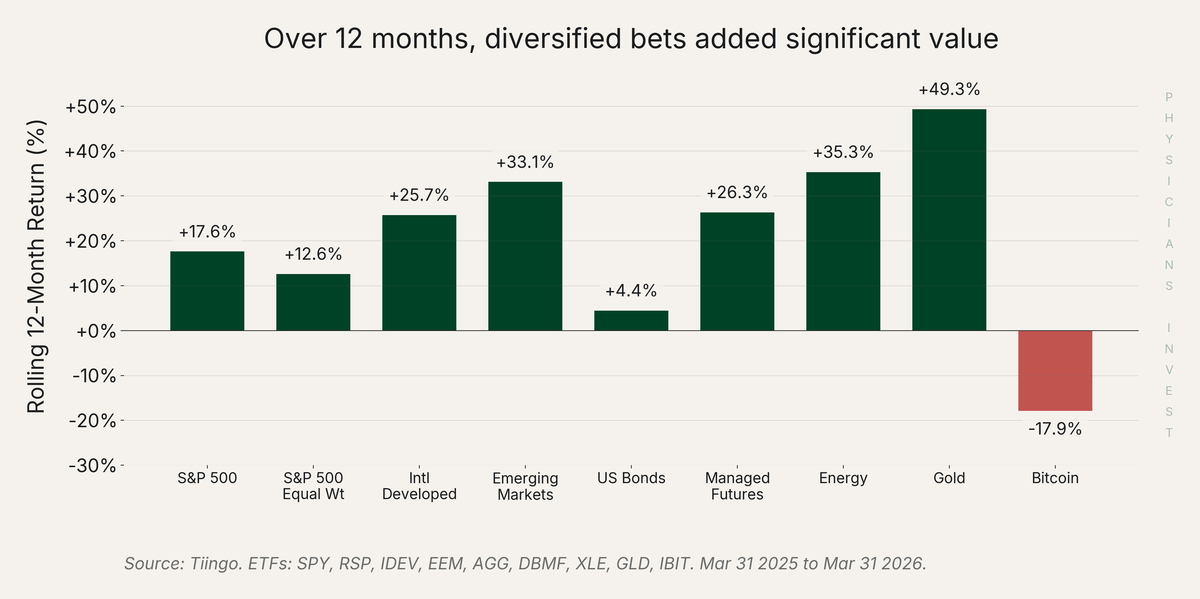

- Energy, managed futures, and gold were all up. The assets most physicians don't own did the protecting.

- Managed futures have returned ~11% annualized over 100+ years with near-zero correlation to stocks. They're ETFs, not exotic.

- Plan your diversification move now. Execute when equities recover.

You spent most of Q1 watching your brokerage account bleed. The S&P 500 dropped 4.4%. Your bond allocation did nothing (AGG, the most popular bond ETF, returned near 0%). Everything you thought was protecting your portfolio... wasn't.

What happened this quarter

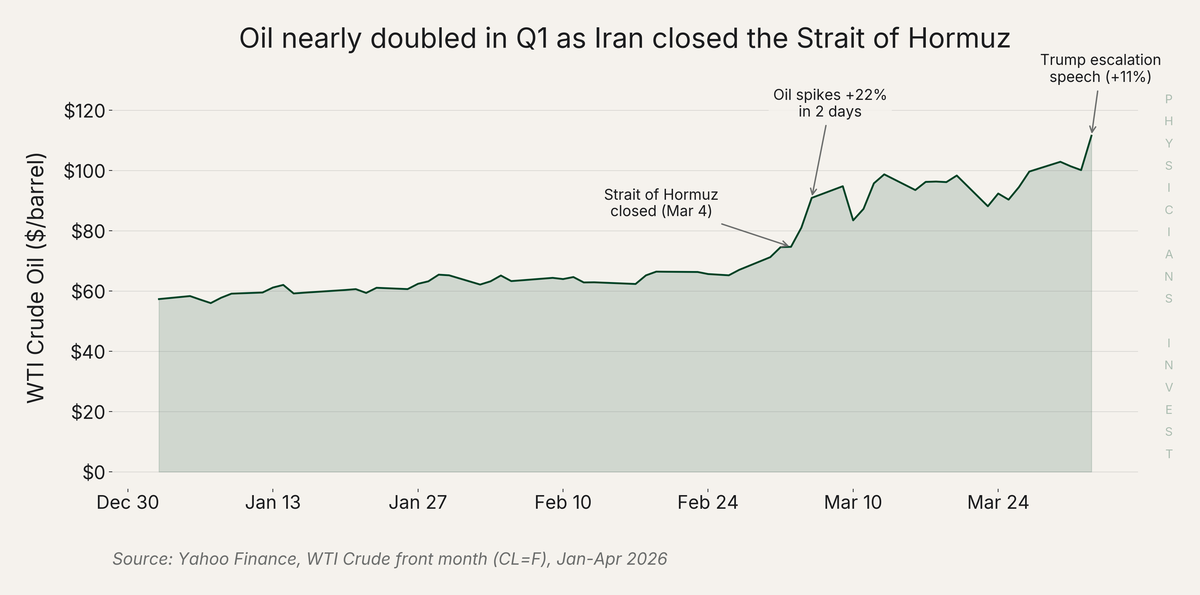

Well, the big story is a war. Iran closed the Strait of Hormuz on March 2, choking off 20% of global oil supply. Oil nearly doubled.

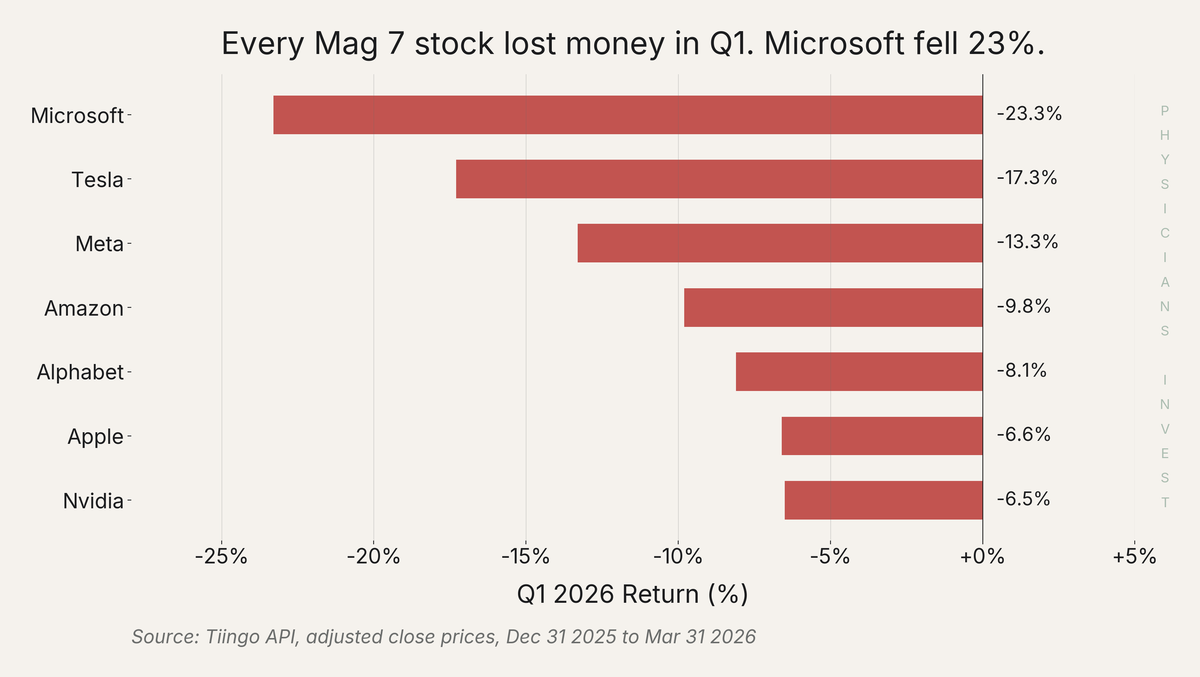

That shock rippled through equities. The S&P 500 fell 4.4%. The Nasdaq dropped 6%. And the biggest names in your index fund got hit hardest.

Microsoft down 23%. Tesla down 17%. Meta down 13%. These seven companies make up roughly 33% of the entire S&P 500. If you're holding SPY or a target date fund in your 403(b), one-third of your equity exposure sits in just seven names.

But other asset classes told a completely different story.

Energy up 38%. Managed futures up 8%. Gold up 9%. The assets most physicians don't own carried the quarter. Worth asking: why don't most physician portfolios hold any of them?

Your portfolio is less diversified than you think

We see the same portfolio over and over: U.S. equity index funds, some bond allocation, a house (which, by the way, should never be considered an "investment"), and a high-yield savings account. Physicians think this is diversified.

It's not.

The financial industry sells the idea that stocks and bonds balance each other out. Q1 proved they don't. Stocks went down. Bonds went sideways. Zero protection. Just like 2022.

There are better diversifiers. Managed futures, energy, gold, and ETFs that run hedge fund strategies (like global-macro or all-weather) have real, measurable negative or zero correlation with equities. They're not exotic private market investments. They're public market ETFs you can buy in any brokerage account. Think of it like a treatment plan: you wouldn't prescribe the same two drugs for every condition. Your portfolio shouldn't rely on the same two asset classes for every crisis.

We think managed futures are the single best diversifier a retail investor can access. Insurance on your equity portfolio that pays you to own it. It blows bonds out of the water. More on this below.

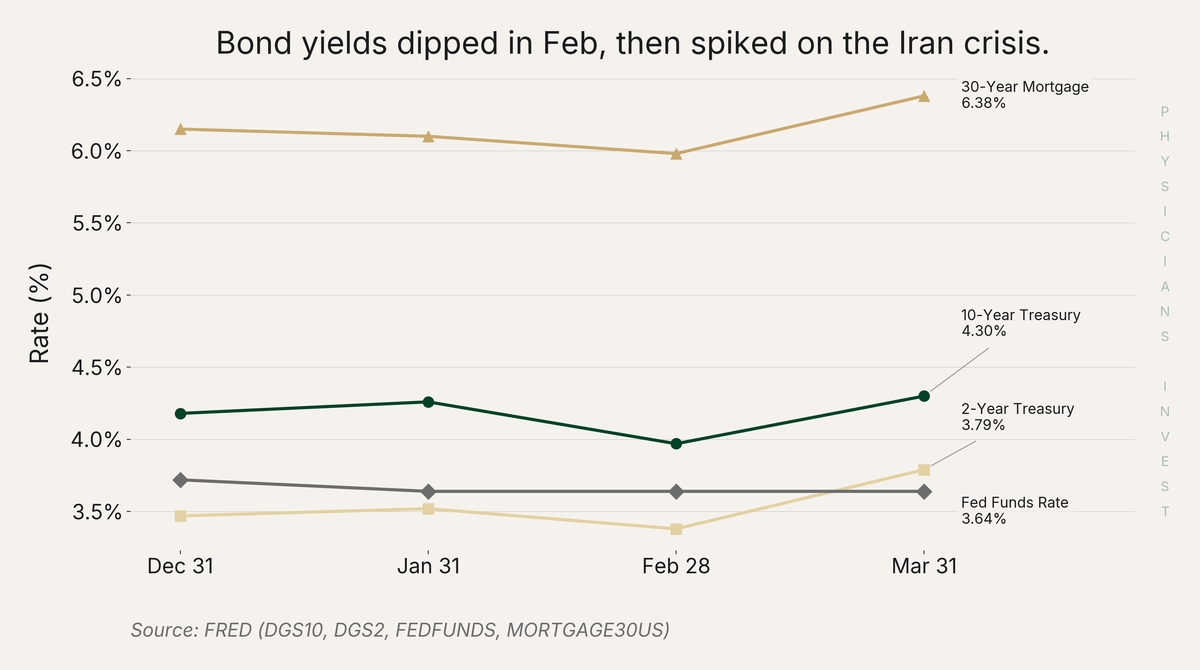

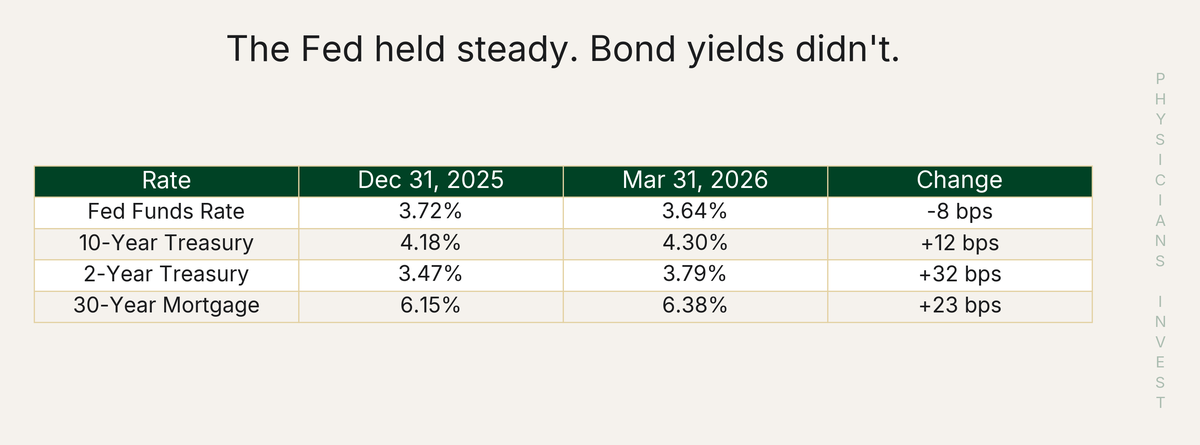

Why bonds didn't hedge this quarter

Bond prices move inversely to interest rates. When rates go up, existing bonds go down. Why? New bonds issued at higher rates make your older, lower-rate bond less attractive. The only way to sell it is at a discount.

In Q1, the 10-year Treasury yield rose 12 basis points (bps, hundredths of a percent) and the 2-year rose 32 bps. Both moved up because bond investors started pricing in higher inflation from the oil shock. AGG returned 0% because the yield increases wiped out the interest income.

The Fed held steady all quarter. But the 10-year and 2-year yields, set by the bond market (not the Fed), spiked in March on inflation fears. Bonds protect against deflation and recession. When the problem is inflation, stocks and bonds can both go down at the same time. (Quick aside: mortgage rates also rose 23 bps this quarter because they track the 10-year, not the Fed rate. We'll do a full deep dive on that in a future issue.)

The rebalancing opportunity most physicians missed

Managed futures are funds that use systematic, rules-based strategies across dozens of markets. When oil is trending up, they're usually long oil. When equities are trending down, they're usually short equities. (We hear "what even are managed futures?" constantly from physicians. It's simpler than it sounds.)

Managed futures returned +8% in Q1. The S&P returned -5%. That's a 13% spread. If you had both, you'd sell managed futures at a gain and rotate into equities at a lower price. Selling winners to buy losers at a discount. This systematic rebalancing works. But you can only do it if you hold uncorrelated assets in the first place. This same pattern played out during COVID and again in 2022.

"Yeah, but what about the long term? One good quarter doesn't justify a portfolio change."

Fair question. Over 100+ years of data, trend-following strategies have returned approximately 11% net annualized with roughly half the volatility of equities and near-zero correlation to stocks. That's from a 136-year study by AQR spanning 67 markets. DBMF, one managed futures ETF, has returned 8.28% annualized since its 2019 launch (past performance does not guarantee future results). These aren't just crisis hedges. They're competitive return streams.

Gold up 49%. Energy up 35%. Managed futures up 26%. The S&P returned 18%. Solid, but not the best game in town.

The Move

- Do not emotionally sell what you currently hold. Write down what you're feeling right now. If a 5-9% drop is making you anxious, your portfolio construction needs work. This is not even a road bump in the grand scheme of things.

- Plan your diversification now. Execute when equities recover. Get exposure to uncorrelated assets. Managed futures are the most accessible option (examples include ETFs like DBMF, CTA, or RSST, though this is not a recommendation to buy any specific fund), but energy, gold, and strategy-driven ETFs also provide diversification. Some investors allocate 10-25% of their portfolio to uncorrelated exposures, though the right amount depends on your situation. A brokerage account gives you the most flexibility, as 401(k)s and 403(b)s have limited fund menus.

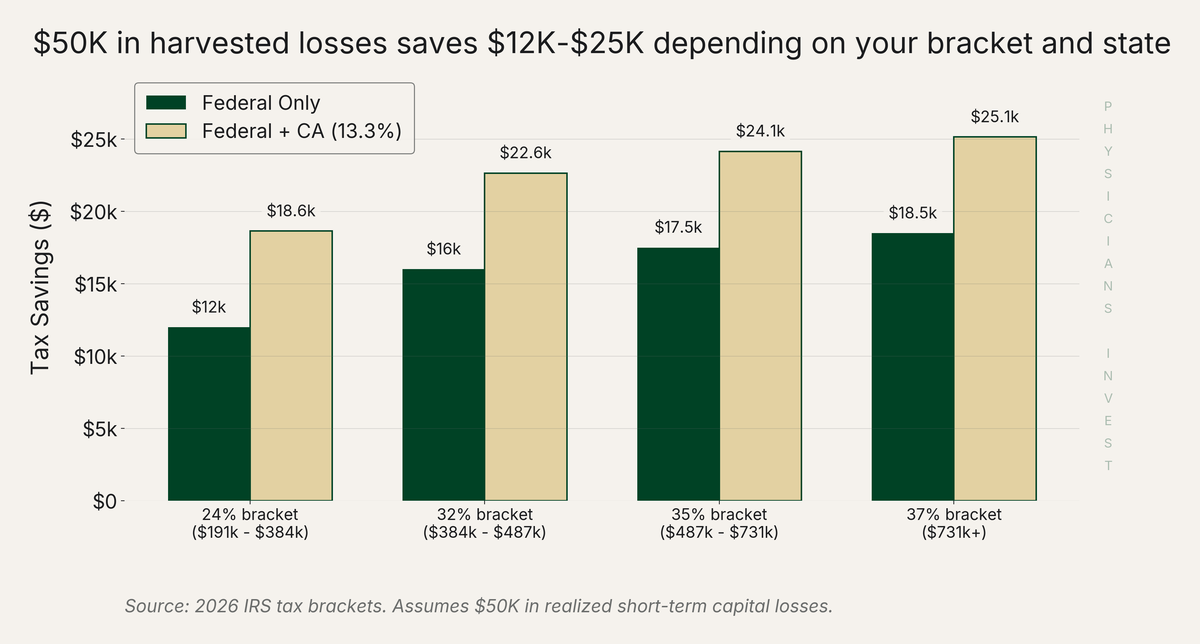

- Use tax-loss harvesting to fund the rotation. If you have positions at a loss, consider selling them. That locks in a loss that offsets a gain elsewhere. Think of it as unlocking the ability to sell something that's up without the tax hit. Watch wash sale rules (you can't buy the same security back within 30 days). A $50K harvest saves $12K-$25K depending on your bracket and state. (We'll do a full TLH deep dive in a future issue.)

- Understand that bonds protect against some crises, not all. Bonds hedge deflation and recession. They don't hedge inflation. Know why you hold them.

The physicians who felt Q1 pain the least were the ones holding genuinely uncorrelated bets. You can build that portfolio too. Start planning now, while the lesson is fresh.

Sources

Data

- Tiingo API -- ETF and equity adjusted close prices (SPY, RSP, IDEV, EEM, AGG, DBMF, XLE, GLD, IBIT, Mag 7 individual stocks)

- FRED -- Treasury yields (DGS10, DGS2), Fed funds rate, mortgage rates (MORTGAGE30US)

- Yahoo Finance -- WTI crude oil front-month futures (CL=F)

Analysis

- Winthrop Wealth Q1 2026 Market Review & Outlook

- AQR: "A Century of Evidence on Trend-Following Investing" -- Hurst, Ooi, Pedersen (136 years, 67 markets)

- DBMF Fact Sheet, December 2025

News