These are hypothetical model portfolios for educational purposes only. They do not represent actual investments, do not account for transaction costs or taxes, and are not personalized investment advice. Past hypothetical performance does not guarantee future results. Physicians Invest does not manage client assets. Consult a qualified financial advisor before making investment decisions.

The 2-Minute Version

- Three model portfolios launched January 2026

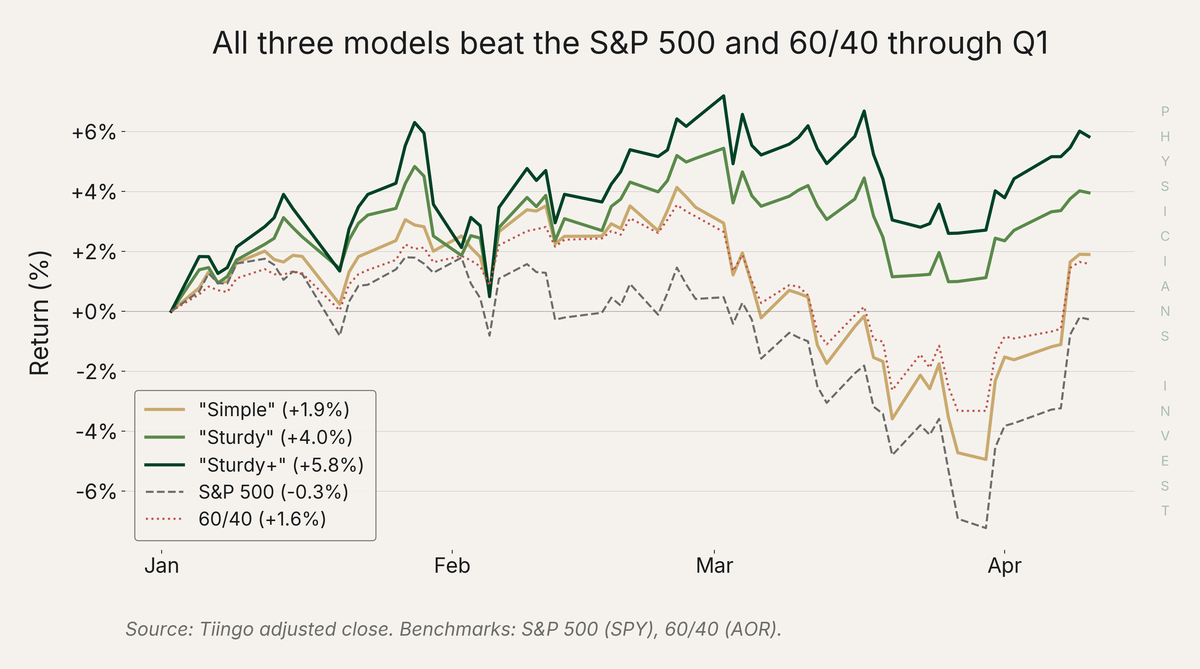

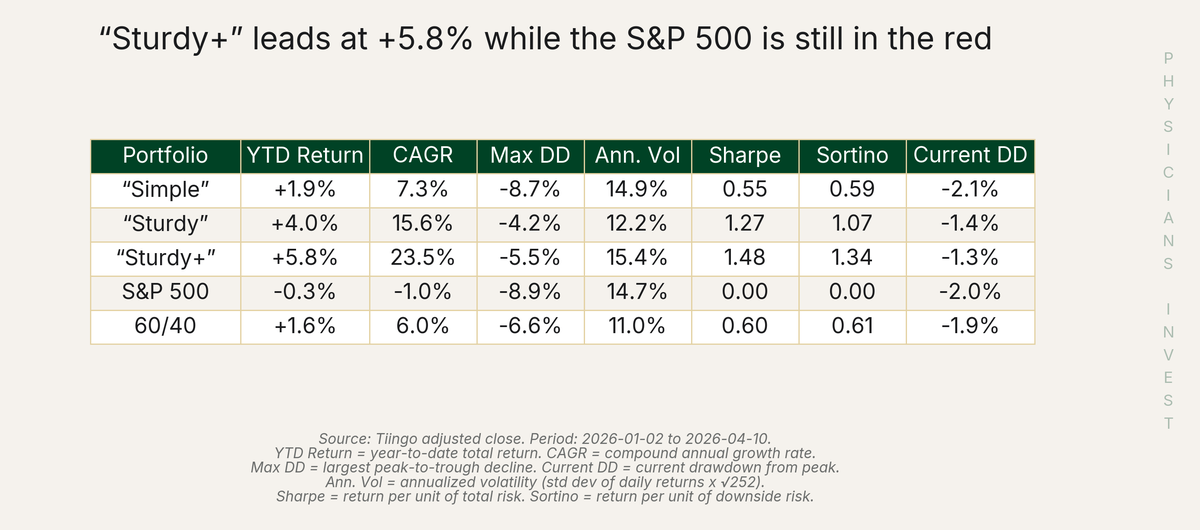

- Year-to-date hypothetical performance: "Simple" (3-fund portfolio) is up 1.9%. "Sturdy" (all-weather) is up 4.0%. "Sturdy+" (150% leveraged) is up 5.8%.

- All three are outperforming the S&P 500 (-0.3%) and a 60/40 benchmark (+1.6%) through April 10

- This is month one. We will update these monthly with changes and rationale.

What are model portfolios?

These portfolios are our effort to provide a solid framework to physicians regarding their asset allocation.

One of the biggest reasons physicians gravitate towards financial advisors is that they just don't know where to start. Unfortunately, when you look at the data, most advisors are not delivering anything meaningfully different than what physicians could achieve themselves. Often physicians can do better with DIY, considering they save significantly on fees. These model portfolios are the frameworks we use when building portfolios for physicians, depending on the sophistication and needs of the individual. We hope this can be a resource to both DIY physicians so that they can build better portfolios, and to hands-off physicians as benchmarks to evaluate their wealth managers by.

Market Context

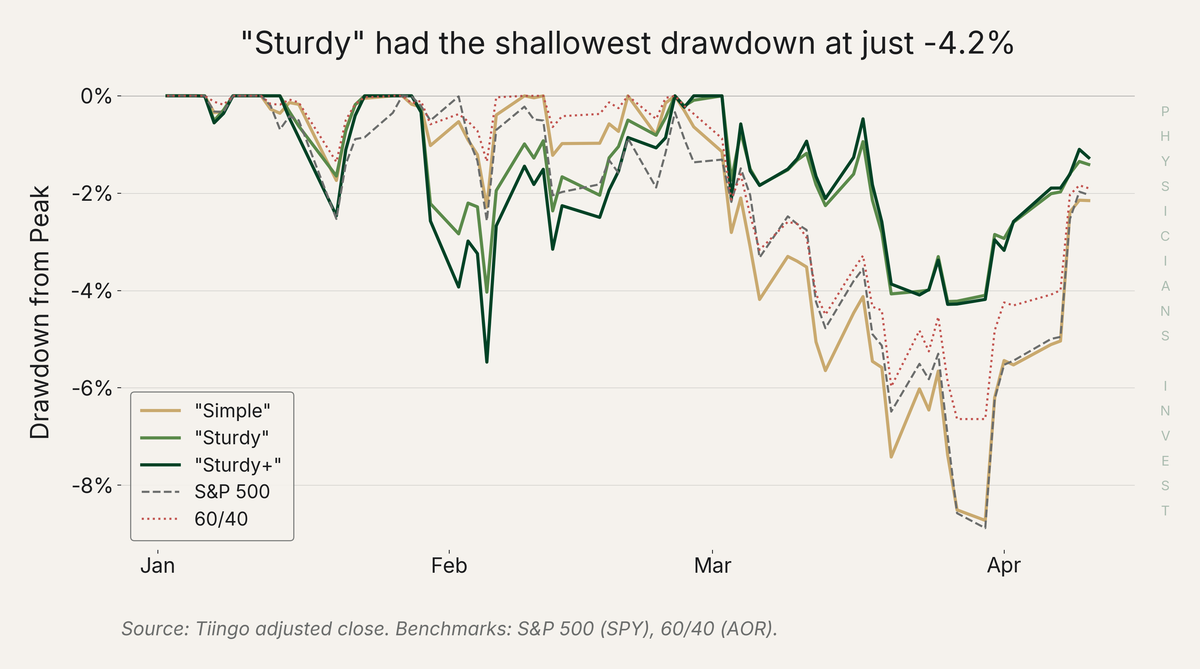

Q1 of 2026 was an interesting quarter as market moves were driven mostly by the Iran war and energy supply disruptions. The S&P 500 dropped 4.4% and bonds were flat. Most investors saw red in Q1, especially those in basic stock/bond portfolios. Investors who had exposure to more sophisticated portfolios not only felt less pain, but probably ended green on the quarter. Robust portfolio construction requires exposure to uncorrelated asset classes that perform differently across various economic environments. There are benefits to holding assets that perform well during events like those of Q1. You wouldn't treat every patient with the same drug regardless of presentation. Same logic applies here.

All three of our model portfolios performed better than benchmarks over the quarter, especially Sturdy and Sturdy+, given their exposure to assets that had tailwinds from Q1 events - such as energy and macro hedge fund ETFs.

Performance Dashboard

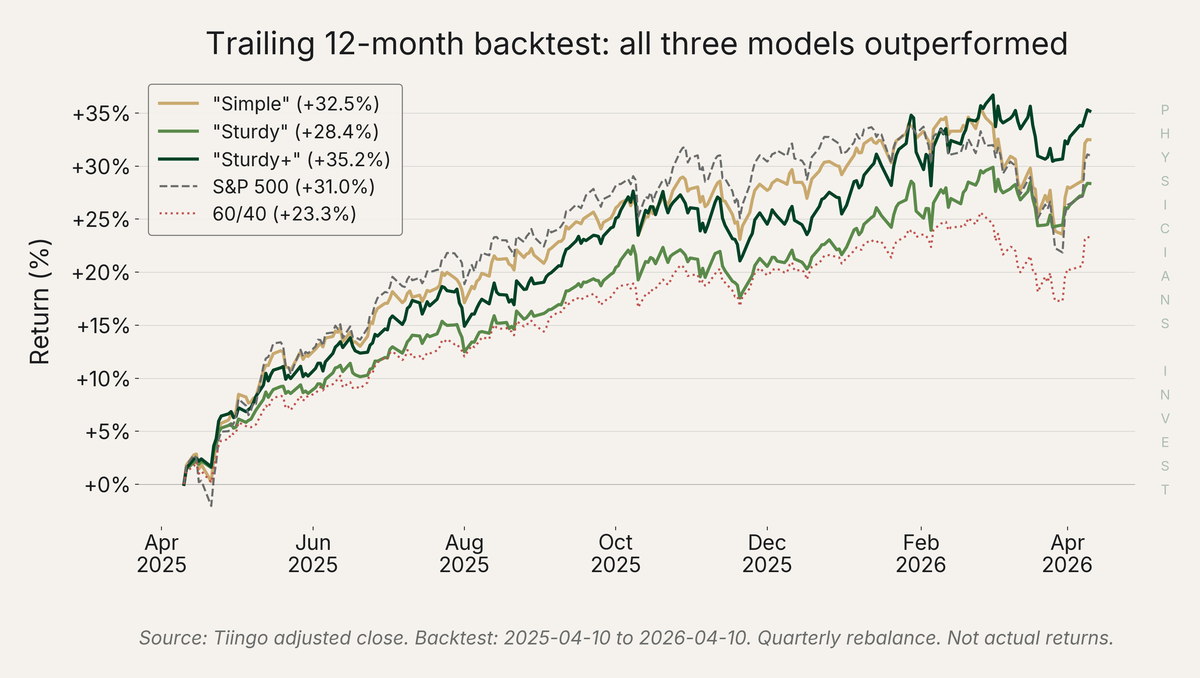

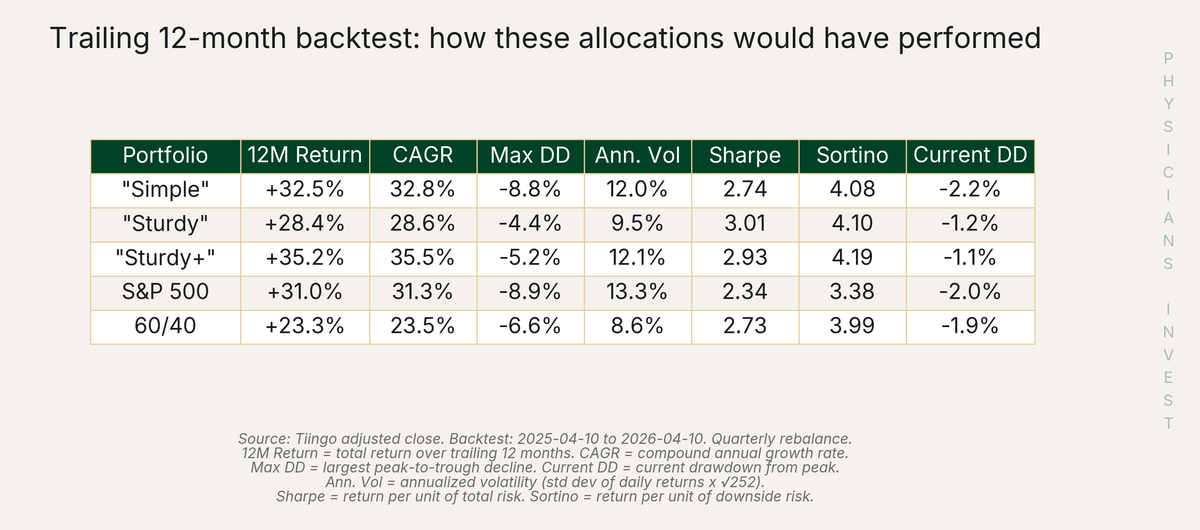

Trailing 12-Month Backtest

To show how these allocations perform across different market conditions, we backtested all three portfolios over the trailing 12 months (April 2025 to April 2026) with quarterly rebalancing. We have done extensive backtesting on these portfolios going back to the early 1990s (advent of electronic trading markets) -- the results of those tests will be discussed in future newsletters as they are the true support of the constructions seen in the Sturdy and Sturdy+ portfolios.

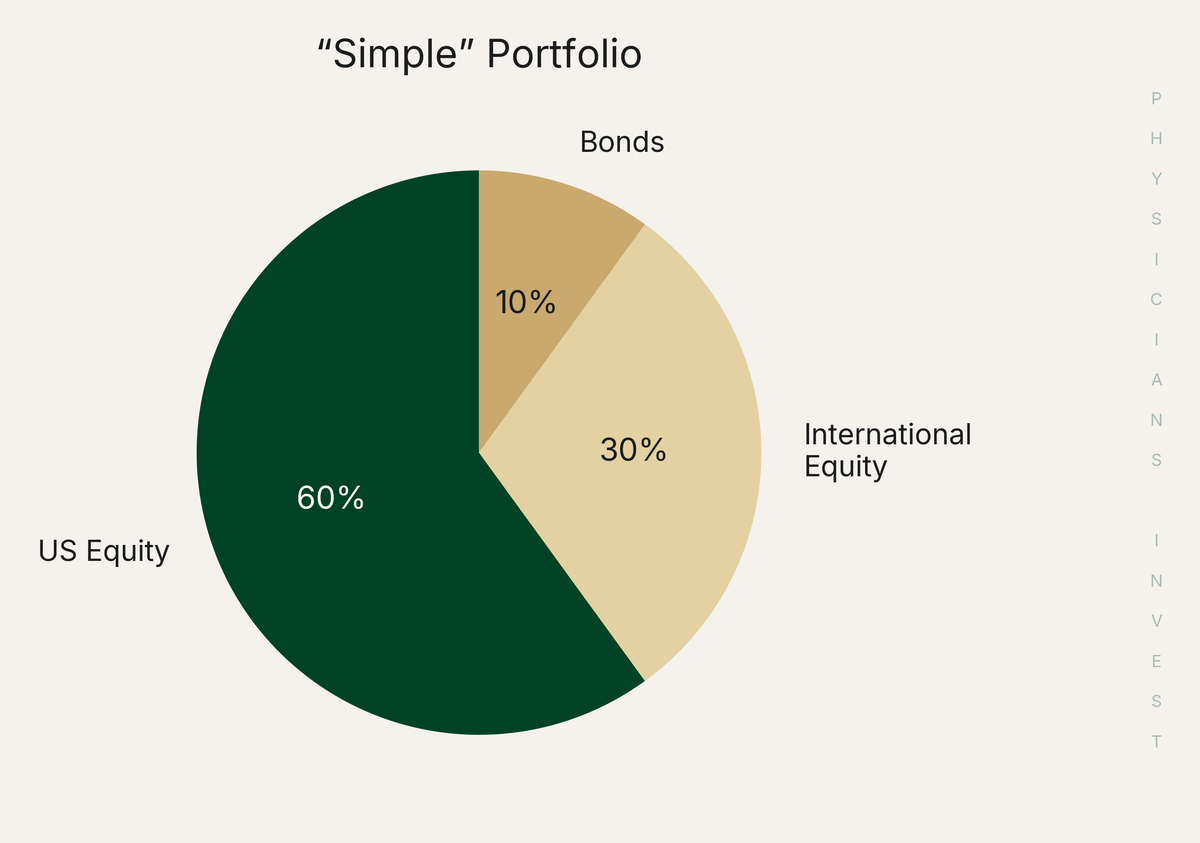

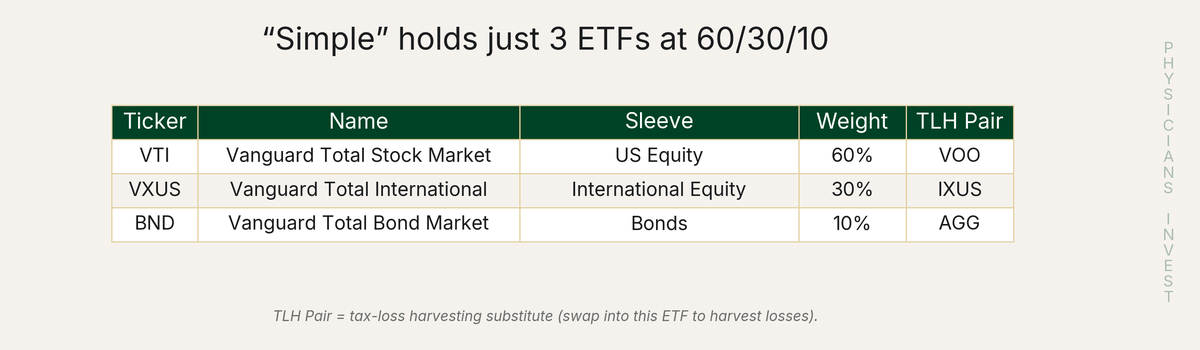

1. "Simple" Portfolio

For: Residents and early-career physicians

Strategy: 3-fund portfolio. Beauty in simplicity but higher volatility.

Advantages: Extremely low cost. Dead simple to maintain. Tax-loss harvesting (selling a losing position to offset gains, then buying a similar ETF) is straightforward with clear pairs. Works in any account type. This is designed for physicians with a net worth between $0 and $250K who don't want to overthink it.

Disadvantages: Entirely dependent on stocks going up. When equities sell off, you have minimal protection. Bonds just slow down the losses. No exposure to alternative return streams. Especially struggles during inflationary regimes, like 2022.

What Changed

No changes since this is the inaugural issue.

Tax-Sheltered Account Tweak

Consider holding all of your bonds in tax-advantaged accounts (Roth, 401(k), 403(b)). Bond coupons are taxed at ordinary income and this portfolio is simple enough to manage having all your bond exposure in tax-sheltered accounts.

Long-Term Capital Gain Status

TLH pairs if needed: VTI to VOO, VXUS to IXUS, BND to AGG.

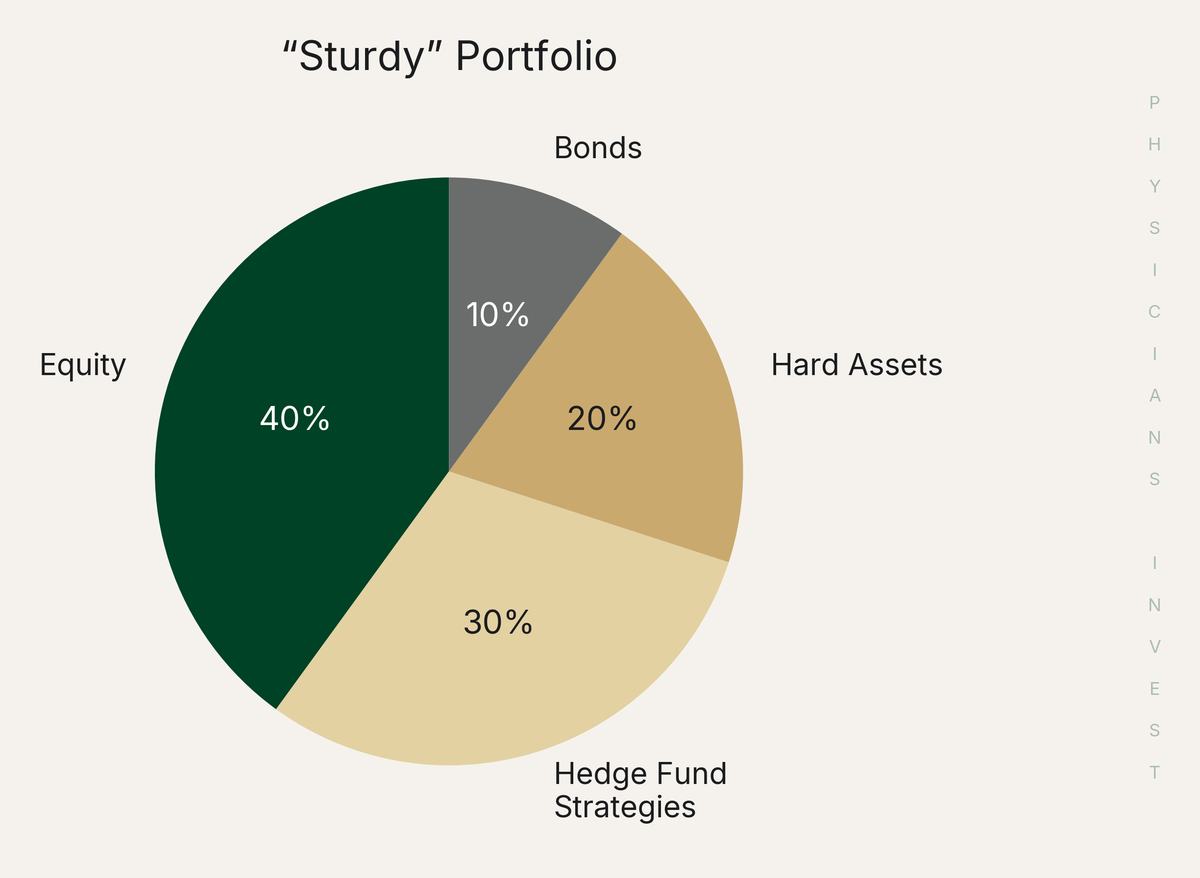

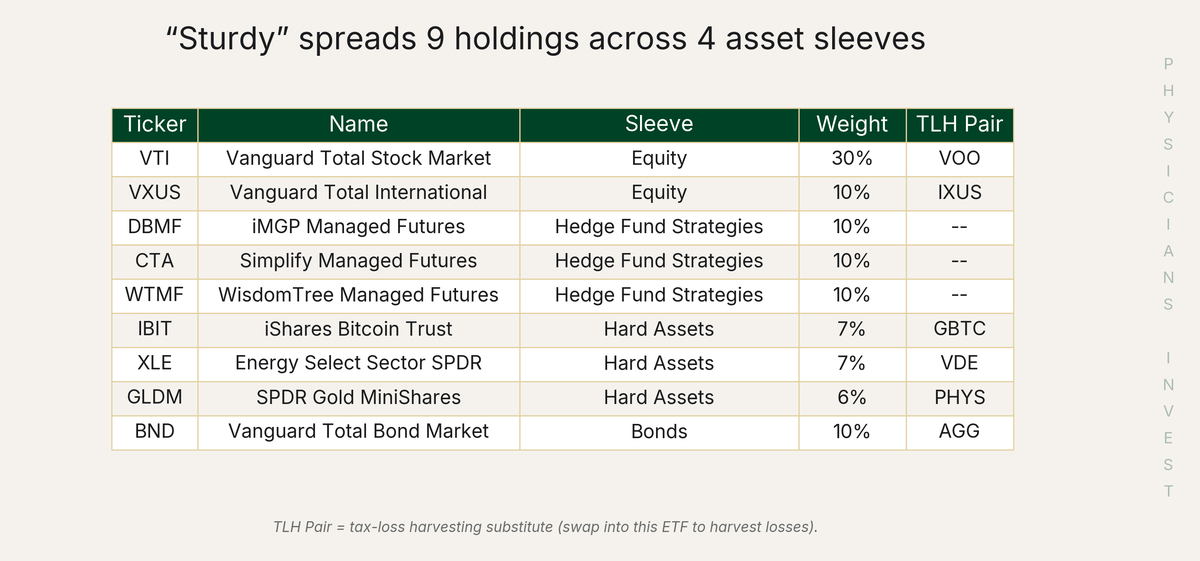

2. "Sturdy" Portfolio

For: Mid-career attendings who want strong growth with better reward-to-risk ratios than what wealth managers typically offer

Strategy: 40% equity / 30% hedge fund strategies / 20% hard assets / 10% bonds

Advantages: Diversified across four distinct asset sleeves. Does not rely on stocks just going up. Hedge Fund Strategy exposure through ETFs provides support when stocks go down. Hard assets provide inflation hedging over the long-term. Built to handle growth, inflation, deflation, and stagnation. The 40/30/20/10 structure draws from institutional asset allocation thinking. It allows investors to not rely on stocks just going up to grow their portfolio.

Disadvantages: More complex than a 3-fund portfolio. More holdings means more tax lots to track. Hedge Fund Strategy ETFs can underperform during sustained equity bull markets. Requires understanding what you own and why. More headache to rebalance.

What Changed

No changes since this is the inaugural issue.

Tax-Advantaged Tweak

Consider holding BND and GLDM in tax-advantaged accounts (Roth, 401(k), 403(b)). Bond coupons are taxed at ordinary income and gold ETFs are taxed at a collectibles rate of 28% regardless of hold length.

Long-Term Capital Gain Status

Tax-loss harvesting pairs ready if needed: VTI to VOO, VXUS to IXUS, XLE to VDE, GLDM to IAUM, BND to AGG.

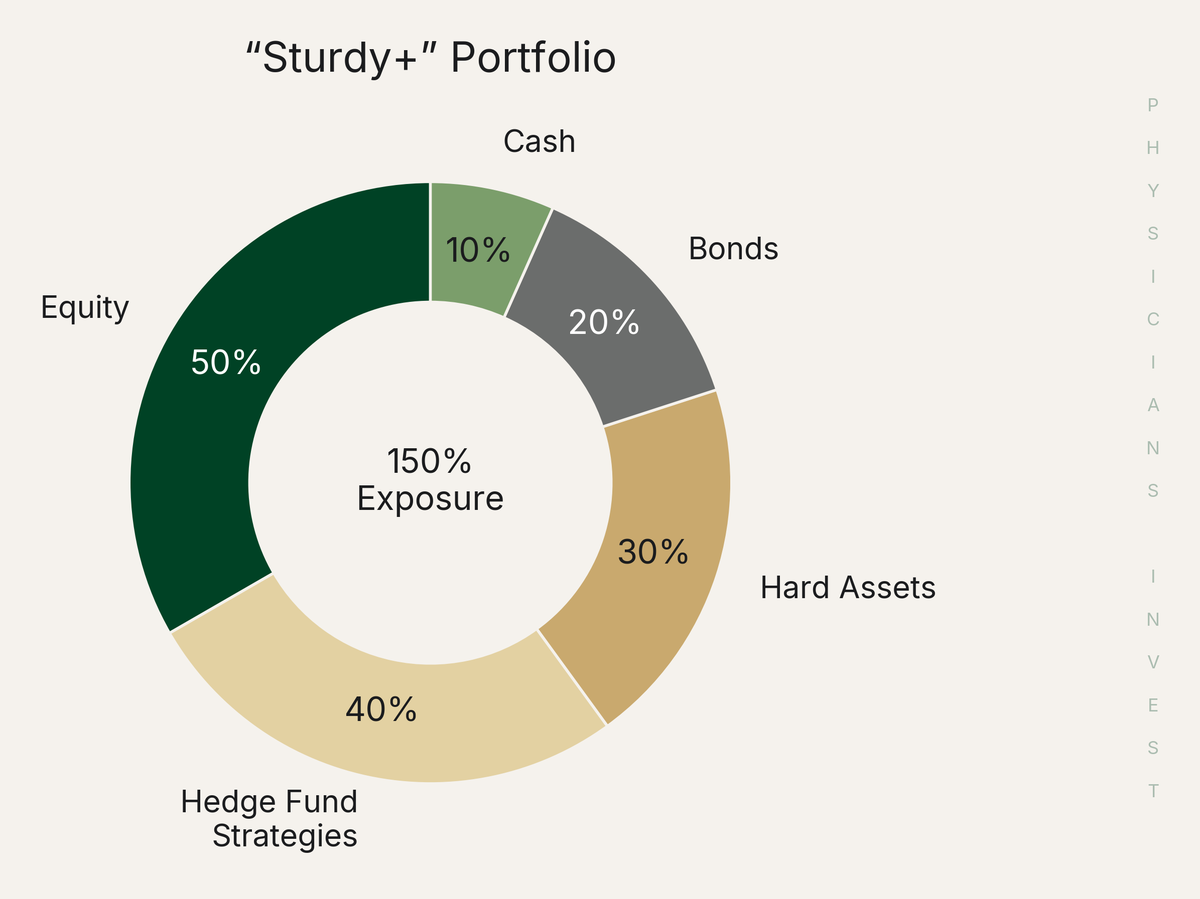

3. "Sturdy+" Portfolio

For: Sophisticated investors comfortable with leverage

Strategy: 150% total exposure via capital-efficient stacked ETFs

Advantages: Gets 150% exposure while only deploying 100% of capital. Broker margin is not needed so the investor avoids any risk of margin calls (and avoids inflated borrowing rates). Investors simply purchase these ETFs like any other, and the stacked exposures are already baked in. Futures-based holdings receive 60/40 tax treatment (60% taxed as long-term gains, 40% as short-term, regardless of holding period), making this more tax-efficient than you might expect for a leveraged strategy.

Disadvantages: More volatile than "Sturdy" due to the additional exposure. More complex to understand. Stacked ETFs are newer products with shorter track records. Requires comfort with leverage and futures, even though the implementation is straightforward.

What Changed

No changes since this is the inaugural issue.

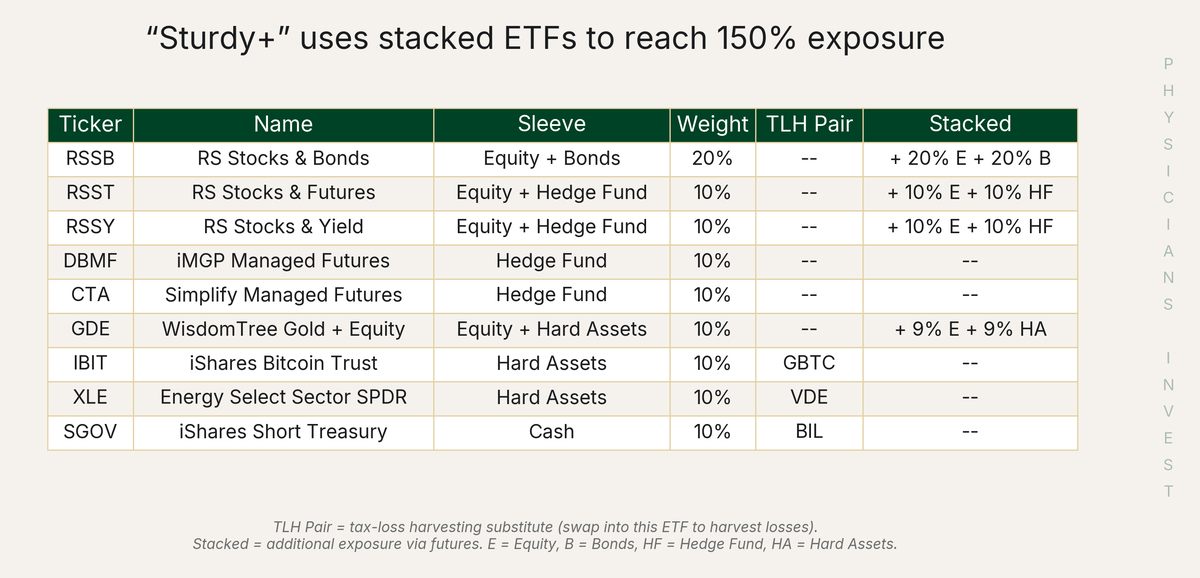

How the Leverage Works

Four holdings provide stacked exposure:

- RSST (10% of portfolio) = 10% US equity + 10% managed futures (trend following)

- RSSY (10% of portfolio) = 10% US equity + 10% managed futures (carry/yield)

- RSSB (20% of portfolio) = 20% global equity + 20% bonds

- GDE (10% of portfolio) = 9% US equity + 9% gold

Think of stacked ETFs like combination drugs: Augmentin gives you amoxicillin plus clavulanate in one pill. RSST gives you equity plus managed futures in one ticker. Combined with the standalone holdings (DBMF, CTA, IBIT, XLE, SGOV), total exposure reaches approximately 150% while only deploying 100% of capital. No broker margin required...and a much lower effective borrowing rate than broker margin.

Tax-Advantaged Tweak

Consider holding SGOV in tax-advantaged accounts (Roth, 401(k), 403(b)). Bond coupons are taxed at ordinary income and benefit more than the other ETFs from location in tax-advantaged vehicles.

Long-Term Capital Gain Status

The stacked ETFs (RSST, RSSY, RSSB, GDE) all hold futures, which receive 60/40 tax treatment (60% long-term, 40% short-term) regardless of holding period.

Methodology

These model portfolios track a hypothetical investment made on January 2, 2026. All prices use adjusted close from Tiingo (accounts for splits and dividends). No transaction costs, slippage, or taxes are modeled. Benchmarks: SPY (S&P 500 ETF) and AOR (iShares Core Growth Allocation ETF, a 60/40 proxy). All metrics annualized where applicable.

The portfolios are account-agnostic. They work in taxable, traditional IRA, Roth IRA, 401(k), or any other account type. Tax-advantaged tweaks are noted per portfolio as suggestions, not requirements.

We will update these portfolios on the second week of every month. Small tweaks monthly, bigger rebalances quarterly. We will clearly note any and all changes and the rationale behind them.