The 2-Minute Version

- Private credit is a $3 trillion asset class about to enter 401(k) and 403(b) plan menus. It will be pitched as a high-return, low-volatility alternative. The pitch leaves out a lot.

- The 9.3% headline return is gross of fees and based on internal models, not market prices. After four layers of fees, you're looking at roughly 7% for an illiquid, opaque investment.

- Physicians are uniquely bad candidates for this asset class. You already can't raise prices to keep up with inflation. Adding a fixed-income instrument with capped returns doubles that vulnerability.

- Before you say yes: ask if the return is gross or net, whether the price is real or modeled, what the public-market equivalent volatility looks like, and who is on the other side of the trade.

Your plan sponsor is about to pitch you something new at the next enrollment meeting. It will sound sophisticated. It will come with impressive return numbers. And if you're like most physicians, you won't have the time to dig into it between patients.

What Private Credit Actually Is

When a mid-sized company needs a loan and can't get one from a bank (or doesn't want the scrutiny), it borrows from a private credit fund instead. The fund pools investor money, lends it out, and collects interest. You get a slice of that interest.

You're basically being the bank. Except you don't set the terms, you can't see the borrower's full books, and you can't get your money back when you want. The IMF noted these borrowers tend to be smaller, more leveraged, and more vulnerable to rate increases than public bond issuers. Many have, diplomatically, less than professional accounting controls.

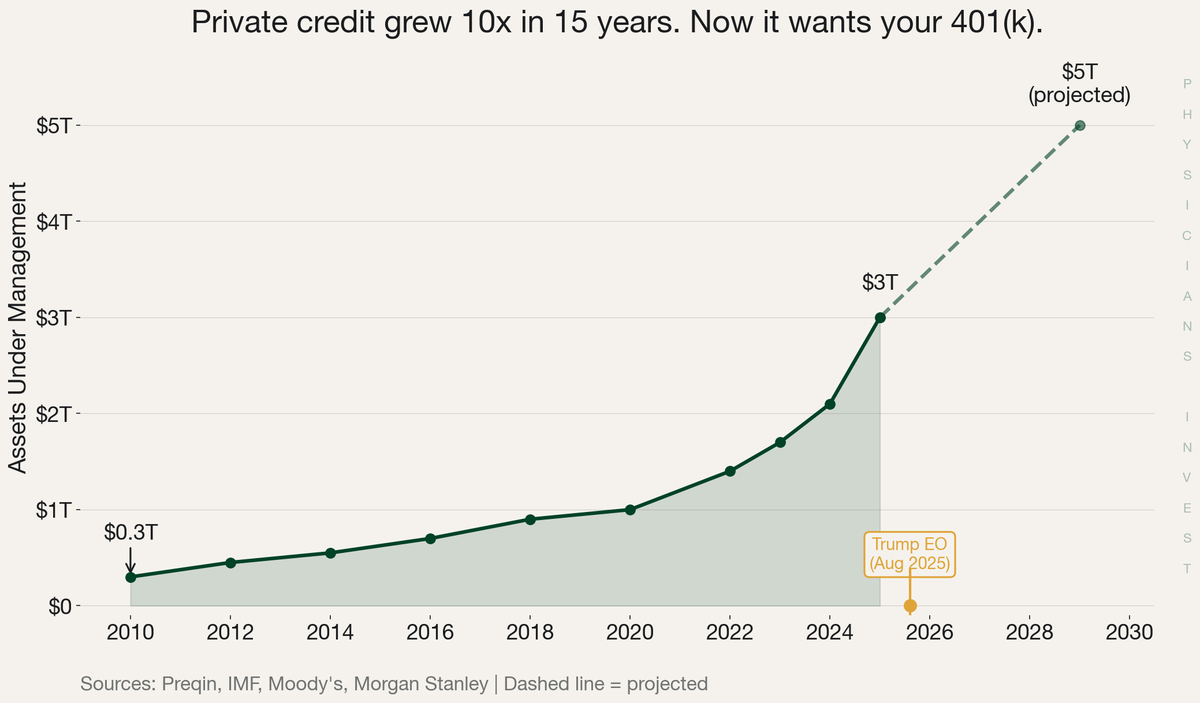

The $3 Trillion Push Into Your Retirement Account

Private credit was the exclusive playground of endowments and pension funds for decades. Then in August 2025, President Trump signed an executive order titled "Democratizing Access to Alternative Assets for 401(k) Investors." The DOL cleared the path. The SEC followed. Blackstone, KKR, Apollo, and Blue Owl all started building products for retirement plan menus.

Sources: Preqin, IMF, Moody's, Morgan Stanley

Sources: Preqin, IMF, Moody's, Morgan Stanley

If this investment is so good, why didn't institutions buy all of it? Big finance is not a charity in any sort of way. Follow the trail all the way back, and you're often the exit liquidity for a large institution that invested years ago and wants out.

The Pitch vs. The Reality

The pitch: 9.3% annualized returns with low volatility. But that number needs the skeptic's checklist.

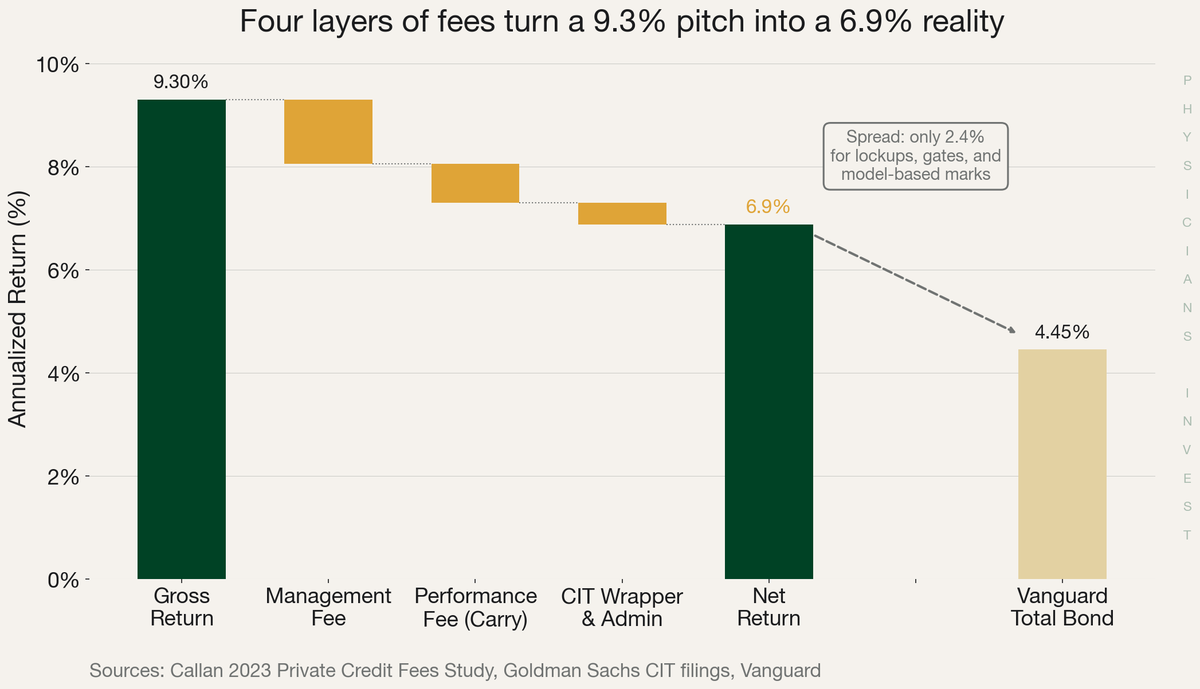

Is it gross or net of fees? Gross. The Cliffwater Direct Lending Index reports gross-of-fee returns. Net of fees, you're closer to 7.2%. And the fee structure is four layers deep.

Sources: Callan 2023 Private Credit Fees Study, Goldman Sachs CIT filings, Vanguard

Sources: Callan 2023 Private Credit Fees Study, Goldman Sachs CIT filings, Vanguard

| Fee Layer | Private Credit CIT | Vanguard Total Bond |

|---|---|---|

| Fund management | 1.25% | 0.04% |

| Performance fee (carry) | 0.75% | None |

| CIT/wrapper | 0.36% | None |

| Recordkeeper + admin | 0.06% | 0.01% |

| Total annual cost | ~2.4% | 0.05% |

Individual fee layers are representative and may vary by product. Sources: Callan 2023 Private Credit Fees Study, Goldman Sachs CIT filings, Vanguard

That's 48 times the cost of a Vanguard bond fund. Chasing sophistication for the sake of sophistication often leads to lower returns. (We see this constantly.)

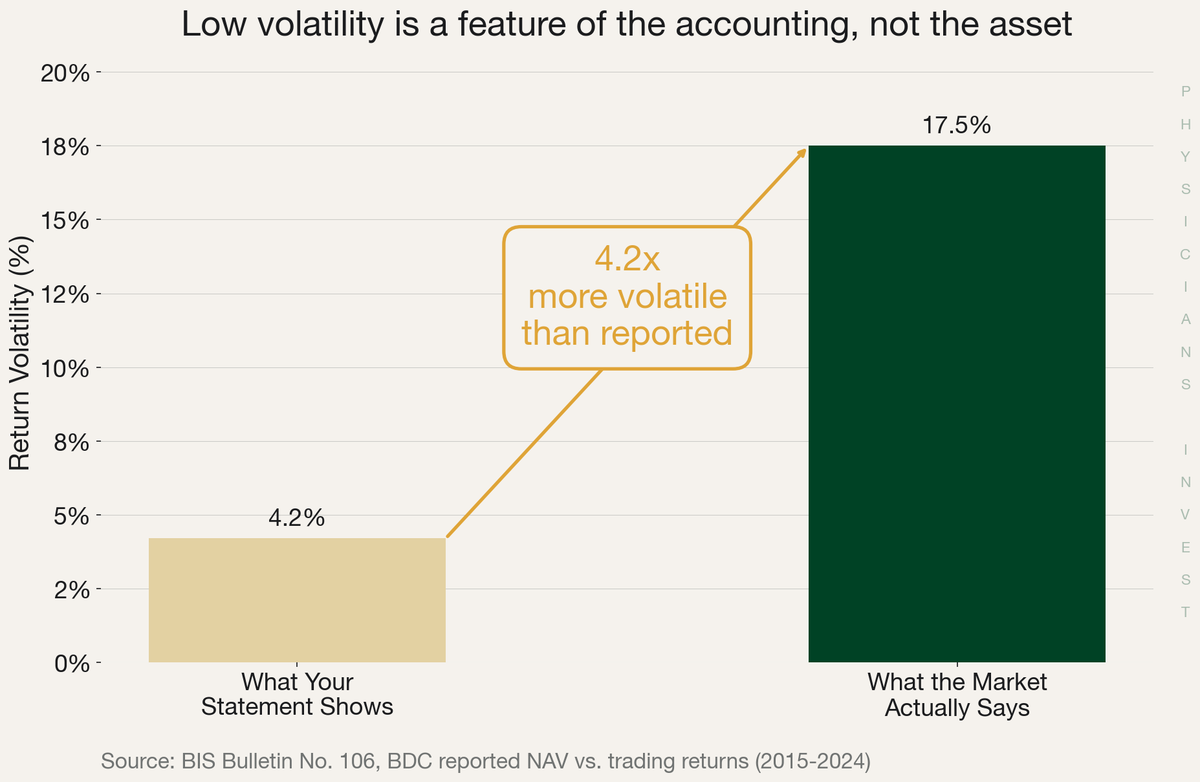

Is the price real? Private credit loans are not priced by a market. The fund manager sets the NAV using internal models. BIS Bulletin No. 106 found actual trading returns are 4.2 times more volatile than reported. That "low volatility" on your 401(k) statement? Laundered volatility.

Source: BIS Bulletin No. 106, BDC reported NAV vs. trading returns (2015-2024)

Source: BIS Bulletin No. 106, BDC reported NAV vs. trading returns (2015-2024)

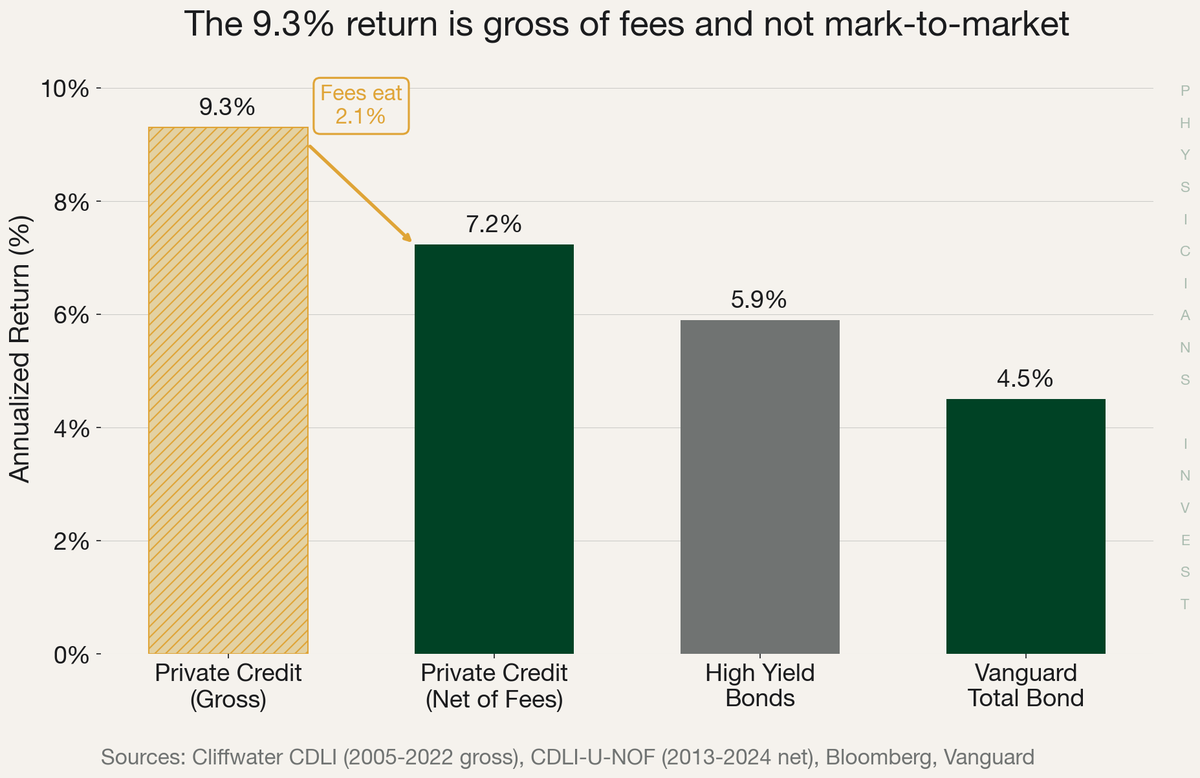

What about alternatives? After fees, private credit nets roughly 7%. High yield bonds give you 5.9% with daily liquidity and real market pricing. The spread for all that illiquidity? About 1.3 percentage points. We don't think that's enough.

Sources: Cliffwater CDLI (2005-2022 gross), CDLI-U-NOF (2013-2024 net), Bloomberg, Vanguard

Sources: Cliffwater CDLI (2005-2022 gross), CDLI-U-NOF (2013-2024 net), Bloomberg, Vanguard

| What They Say | What It Means |

|---|---|

| "9.3% annualized returns" | Gross of fees, based on internal models, not market prices |

| "Low volatility" | The fund manager sets the price. Of course it doesn't swing. |

| "Quarterly liquidity" | With 2-3 year lockups, 5% gates, and the right to suspend redemptions entirely |

| "Institutional quality" | Institutions negotiate better terms and lower fees than retail wrappers offer |

| "Senior secured lending" | To smaller, more leveraged companies that couldn't get a bank loan |

| "Diversification benefit" | Based on reported (model) correlations, not actual market behavior |

Why Physicians Are Especially Bad Candidates

Here's the angle nobody is talking about. Inflation is the enemy of any fixed-rate investment. When you lend money at a fixed rate, the dollars coming back to you in year 5 or year 10 buy less than the dollars you put in. The higher inflation runs, the worse the deal gets. We saw exactly this in 2022 when bonds sold off hard, not because borrowers defaulted, but because inflation made every future interest payment worth less in real terms. Private credit works the same way. Your return is capped at whatever rate was locked in at origination. If inflation runs hot, you eat the difference.

Now layer on the physician problem. Most high earners have a natural hedge against inflation. A lawyer raises rates. A tech founder raises prices. A business owner passes costs through. But physicians are handcuffed. Medicare reimbursements don't keep up with inflation. They've been flat or declining in real terms for years, and political leaders seem increasingly comfortable targeting 3% inflation rather than 2%. A physician making $350K watches practice costs climb while revenue stays stuck.

So you're already on the wrong side of inflation through your career. Private credit doubles that exposure by locking your investment returns into the same losing trade. And unlike public bonds, which you can sell any day if conditions change, private credit locks you in. You can't exit. You just watch.

We think this matters more for physicians than almost any other high-earning profession. If you're going to accept illiquidity, at least invest in something where the upside isn't capped at 7% net. Public equities. Venture capital. Private equity with an actual equity stake. Those give you a shot at real returns that outpace inflation.

| Factor | Private Credit | Public Bond ETF | Public Equity Index |

|---|---|---|---|

| Return potential | Capped (~7% net) | ~4.5% | Uncapped (historically ~10%) |

| Liquidity | Quarterly with gates | Daily | Daily |

| Transparency | Low (model-based NAV) | High (market prices) | High (market prices) |

| Fees | ~2.4% all-in | ~0.05% | ~0.03% |

| Inflation protection | Poor (fixed-rate loans) | Poor | Good (equity ownership) |

| Upside if things go right | Interest payments | Interest payments | Capital appreciation + dividends |

| Downside if things go wrong | Default, locked in | Sell anytime at market | Sell anytime at market |

The Blue Owl Warning

On February 19, 2026, Blue Owl Capital gated $1.7 billion in investor assets when redemption requests exceeded the 5% quarterly cap. The fund that promised "quarterly liquidity" switched to return-of-capital distributions. Shareholders can no longer request redemptions at all. This is exactly the structural mismatch Matt Levine has been writing about: illiquid assets in liquid wrappers work until they don't.

The Move

Run the skeptic's checklist:

- Is this return gross or net of fees?

- Is the price set by a market or by the fund manager's model?

- What's the volatility of a public-market equivalent (like HYG)?

- Who is selling their stake for me to buy, and why?

If you want alternatives to bonds: We'd look at liquid alternative ETFs first. If you want to go truly illiquid, we think the illiquidity premium should come with equity upside.

If you're in a 403(b): The INVEST Act (passed the House December 2025) would open access. Use the time to prepare your analysis before the pitch arrives.

If you're already in a private credit fund: Don't panic. One approach some investors use is hedging credit exposure with put options on a high-yield bond ETF (like HYG) as a public market proxy. Take the learnings and adjust going forward.

Sources

Data

- Cliffwater Direct Lending Index (2005-2024)

- BIS Bulletin No. 106

- Callan 2023 Private Credit Fees Study

- Goldman Sachs CIT filings

- Morgan Stanley Private Credit Outlook

Policy

- Executive Order, "Democratizing Access to Alternative Assets" (Aug 7, 2025)

- DOL Rescinds Private Equity Guidance (Aug 12, 2025)

- SEC ADI 2025-16 (Aug 15, 2025)

- INVEST Act (Dec 2025)

- DOL Proposed Rule (Jan 13, 2026)

Analysis