The 2-Minute Version

- Physician pay rose between 2.9% and 3.7% in 2024, depending on who you ask. Inflation ran higher either way. Your purchasing power dropped again.

- Medicare now pays physicians 33% less than in 2001 after inflation. A new "efficiency adjustment" cuts another 2.5% from procedural specialties.

- Where you practice matters as much as what you practice. And your savings account is not protecting you.

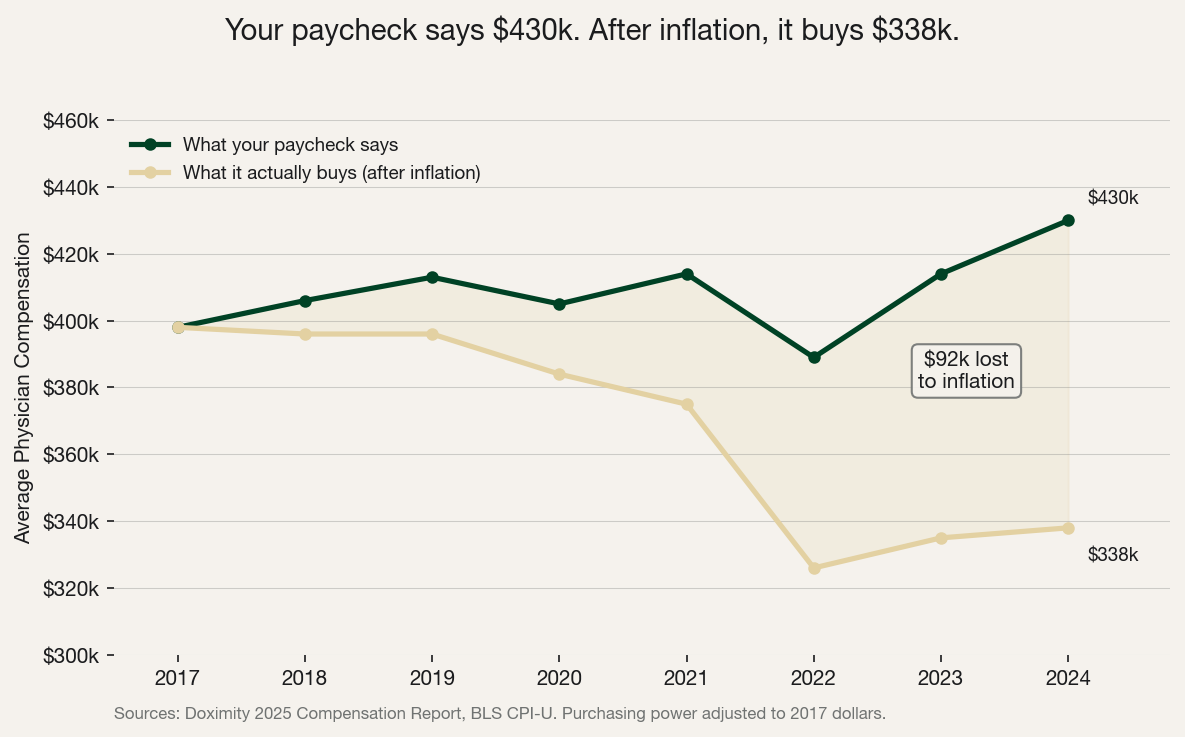

$430,000. That's the average physician salary in 2024 according to the Doximity 2025 Compensation Report, which pegs year-over-year growth at 3.7%. Medscape's 2025 report puts it lower at 2.9%. Either way, it didn't beat inflation. Adjust for CPI and you're looking at $338,000 in 2017 dollars. You're working harder, seeing more patients, and buying less with every paycheck.

The Squeeze Is Real

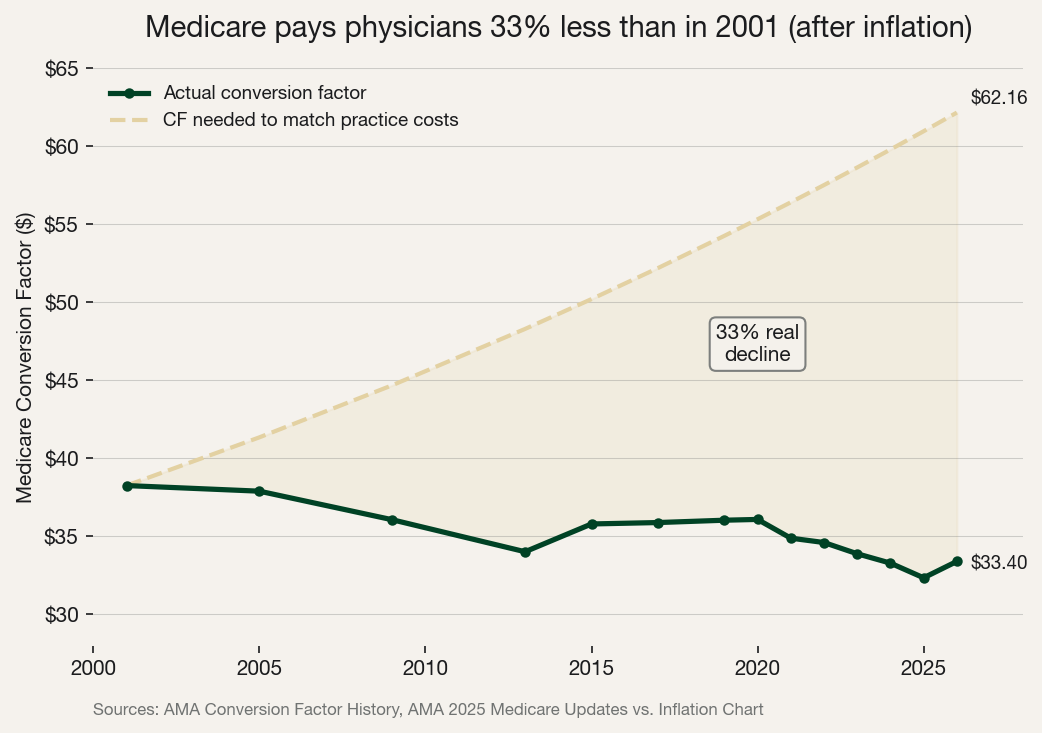

Here's how Medicare actually calculates your payment: take the RVUs for a service, multiply by the conversion factor ($33.40 in 2026), then adjust for your geographic area. That conversion factor peaked at $38.26 in 2001. Twenty-five years later, it's still lower. Meanwhile, the cost of running a practice rose 59% over the same period. 90% of medical groups reported higher operating costs in 2025, with the average increase hitting 11.1%.

Sources: Doximity 2025 Compensation Report, BLS CPI-U

Sources: Doximity 2025 Compensation Report, BLS CPI-U

Sources: AMA Conversion Factor History, AMA 2025 Medicare Updates vs. Inflation Chart

Sources: AMA Conversion Factor History, AMA 2025 Medicare Updates vs. Inflation Chart

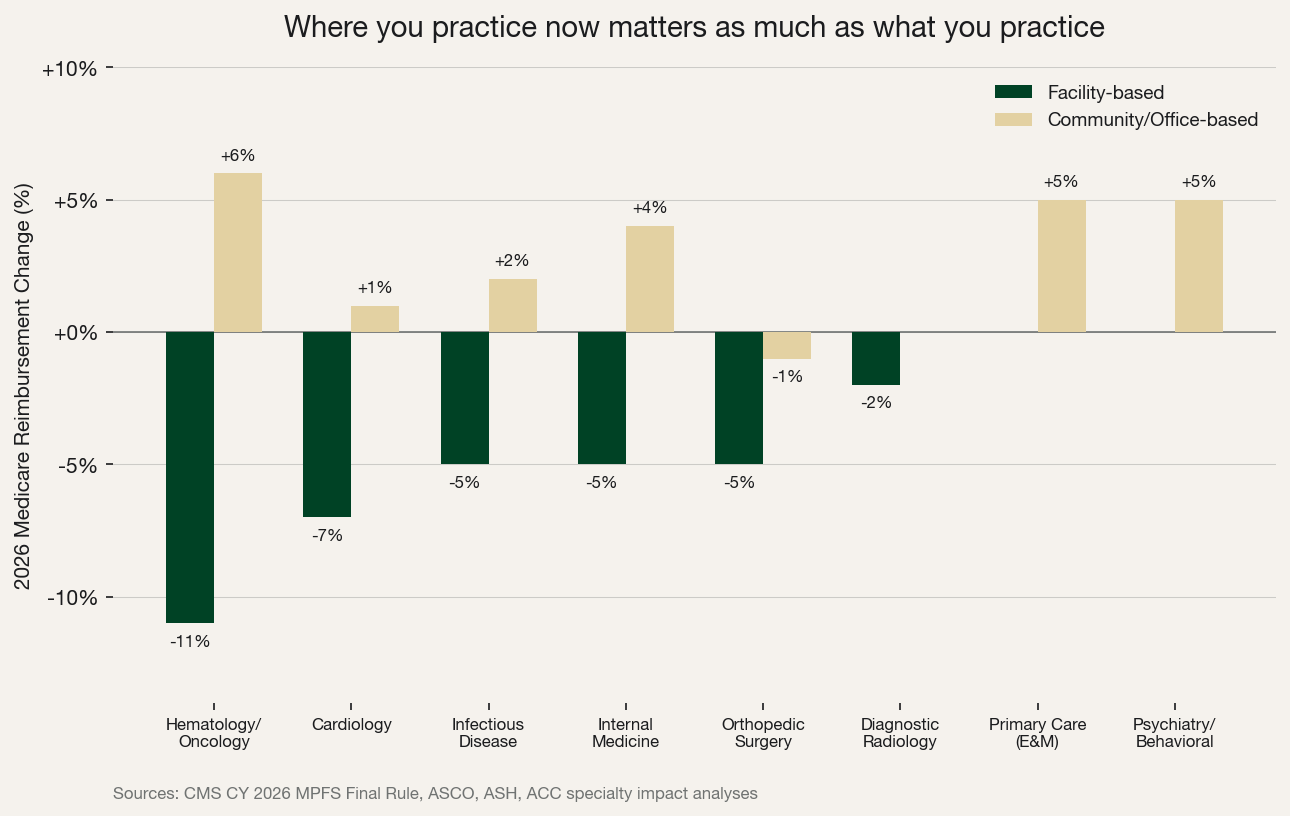

And it just got worse. CMS finalized an "efficiency adjustment" for 2026. A 2.5% cut to work RVUs across 7,000+ procedure codes. If your employment contract pays you per RVU (and most do), that's a direct pay cut. Congress passed a one-time 2.5% bump through the One Big Beautiful Bill Act (signed into law July 4, 2025), but that sunsets after December 2026.

The adjustment doesn't hit everyone equally. Facility-based oncologists face an 11% reimbursement cut. Community-based oncologists got a 6% bump. Cardiologists in hospitals: down 7%. In office settings: up 5%. Primary care E&M codes? Exempt entirely.

Sources: CMS CY 2026 MPFS Final Rule, ASCO, ASH, ACC

Sources: CMS CY 2026 MPFS Final Rule, ASCO, ASH, ACC

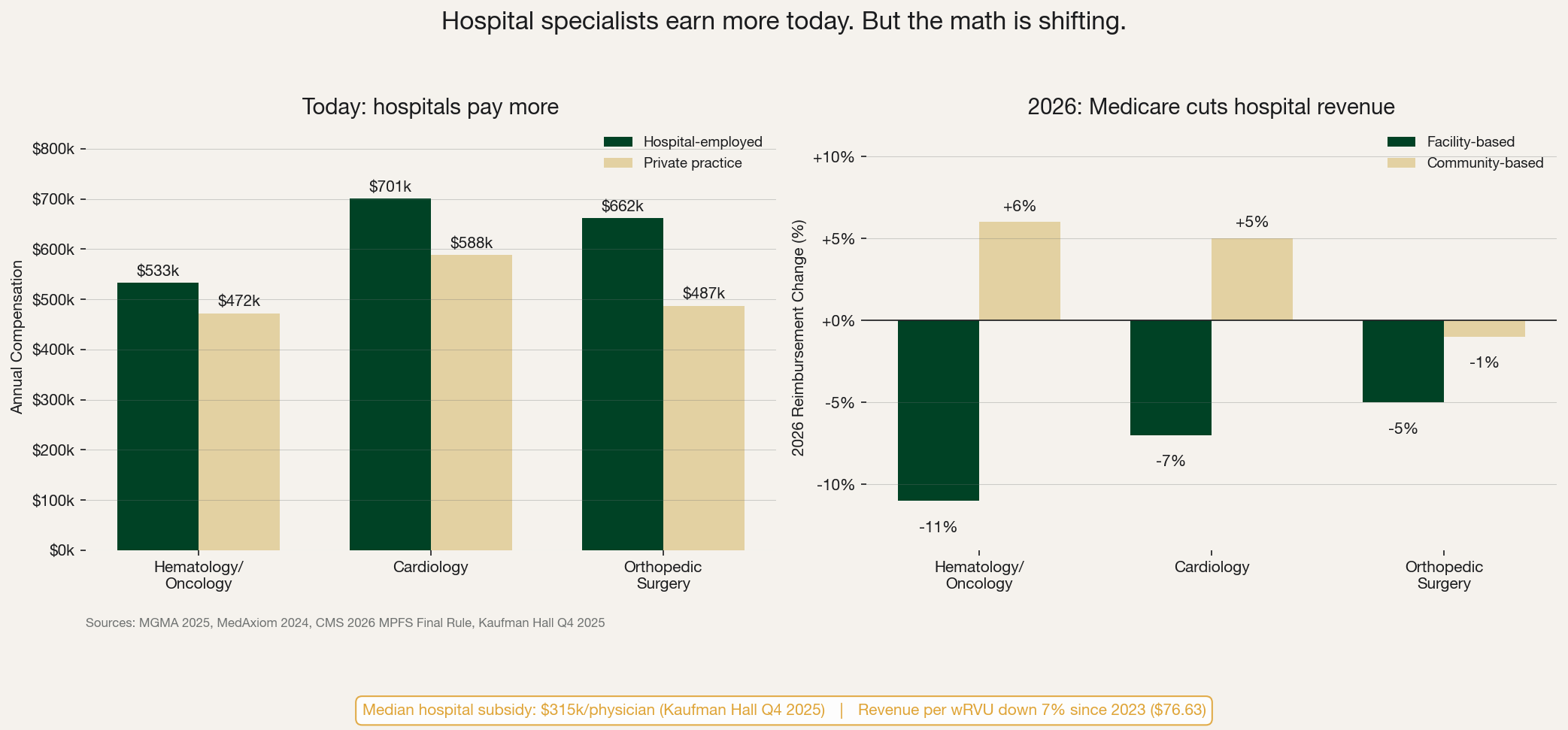

Hospital-employed oncologists currently earn $533k versus $472k in private practice. Cardiologists in hospitals make $701k versus $588k. Hospitals pay more right now. But they're absorbing 11% and 7% revenue hits respectively. The median hospital subsidy per physician hit $315,000 in Q4 2025 according to Kaufman Hall. Revenue per wRVU is down 7% since 2023, sitting at $76.63. When contracts come up for renewal, wRVU conversion rates will drop.

Sources: MGMA 2025, MedAxiom 2024, CMS 2026 MPFS Final Rule, Kaufman Hall Q4 2025

Sources: MGMA 2025, MedAxiom 2024, CMS 2026 MPFS Final Rule, Kaufman Hall Q4 2025

So where is all the money going? Healthcare spending reached a confirmed 18% of GDP ($5.3 trillion) in 2024, projected to hit 20.3% by 2033. The system spends more every year. But that money flows to insurance companies, hospital admin, mid-level providers, and pharma. Not to physicians. This will not change unless physicians aggregate together, understand their value, and stop accepting lower inflation-adjusted wages. There is strength in numbers.

What to Do About It

We think there are three moves every physician should make this year.

First, fix your investments. Physicians keep incredibly high cash balances. We see it on every physician community thread where people recommend high-yield savings accounts. The fact that they are even recommending a HYSA is the first issue. A bank savings account will pay less than short-term money markets or short-term treasuries, which are just as safe, if not safer because of FDIC limits (we've checked). Your attending salary has proven to be a poor inflation hedge. So your investments need to be. Physicians must accept the hard reality that they're going to have to take on some volatility. Hard assets with limited supply: real estate beyond your primary residence, commodities through dedicated hedge funds (timing commodities directly is a losing game), gold and bitcoin in self-custody. Stocks respond well to initial inflation shocks but do poorly over time. Don't assume your index fund is protecting you.

Second, know your numbers. Many physicians are leaking cash in areas they don't realize. This isn't about living a spartan life. That's miserable. It's about knowing your largest annual expenses by category so you can optimize thoughtfully. Know where your career path and your spouse's career path are heading. If you're in a facility-based specialty facing reimbursement cuts, that changes your savings rate calculation.

Third, join the fight. Physicians feel a need to keep up with peers who have been earning for years. That desire to keep up becomes a lot harder when your inflation-adjusted pay keeps shrinking. If enough physicians participate in organizations like Physicians Invest, there are enough numbers to start making waves in Washington. HR 7520 (the Efficiency Adjustment Delay Act), introduced February 12, 2026, already has 35+ medical organizations endorsing it. It's early stage. That's exactly why it needs physician voices now, not after the window closes.

For medical students and residents: you don't need to pick a specialty based on money. But understand the financial trajectory across specialties and practice settings before you commit.

Sources

Data

- Doximity 2025 Physician Compensation Report

- Doximity OpMed: Physician Pay Appears Higher Than Ever

- Medscape 2025 Physician Compensation Report

- MGMA: Medical Practice Operating Costs Still Rising in 2025

- MedAxiom 2024 Cardiovascular Compensation Survey

- PhysiciansThrive: Hematology/Oncology Salaries

- Health Affairs: National Health Expenditure Data

Analysis

- AMA Conversion Factor History

- AMA: Medicare Physician Pay Has Plummeted Since 2001

- AMA: Physicians Will See Medicare Payments Rise in 2026

- ASCO Post: Significant Medicare Reimbursement Changes for 2026

- ACC: 2026 Medicare Physician Fee Schedule Final Rule

- J. Taylor: The Growing Crisis of Physician Practice Losses

- Kaufman Hall Q4 2025 Physician Enterprise Report

Policy