The 2-Minute Version

- Real estate is an asset class with strong tax advantages, but Section 469 of the tax code means most W-2 attendings cannot actually use the tax shelter that many marketing decks lead with.

- REITs are not a true diversifier from a stock portfolio. They are ~70% correlated to the moves in the S&P 500 and sell off at the exact same time stocks do.

- We lay out the 9 most common real estate exposure paths with realistic return ranges for each. We also outline exposure by career stage, and four due diligence questions to run before you ever write a check for a private real estate investment.

The Dollar Math A poor investment in private real estate can cost you 100% of your investment, especially if the sponsor is using debt to finance some of the project. Avoid a $25,000 to $100,000 mistake by understanding the landscape and following some simple principles.

Real estate pitches, both the legit and the scammy, show up in a physician's inbox constantly. Why are physicians such targets for this? To be honest, it is largely self-induced because physicians, like most people, are looking for real estate exposure. The reasons for real estate always being top-of-mind for investors are below.

- It's tangible. You can drive past the property and point at it. You can also use it for yourself in the case of short-term rentals.

- It has unique tax advantages. Both short-term writeoffs and long-term ability to exchange into other investments (1031 exchange).

- It is inflation protected. Real estate keeps up with inflation over the long-term, which preserves purchasing power.

- The returns are decent and the investment cashflows monthly. With that said, total returns are not astronomically higher than equities and have limited upside compared to other opportunities like hedge funds, private equity, and venture capital.

We think real estate earns a place in a physician's portfolio around the $1M+ net-worth stage, but there are traps and pitfalls for which physicians need to be aware.

The Setup

Here are some things that typical real estate investment marketing often glosses over.

-

The "passive income" myth. Passive income with private real estate is really not a thing. Doing it right takes a significant amount of time and paperwork/record-keeping. That time comes out of family, friends, and the rest of your life.

-

Transaction costs. Equities trade with a one button press. Real estate transactions are long, slow, and expensive. Commissions, title work, and financing fees eat realized returns significantly.

-

The tax wall. Unless you use a few loopholes, physicians cannot offset their wage income with real estate depreciation.

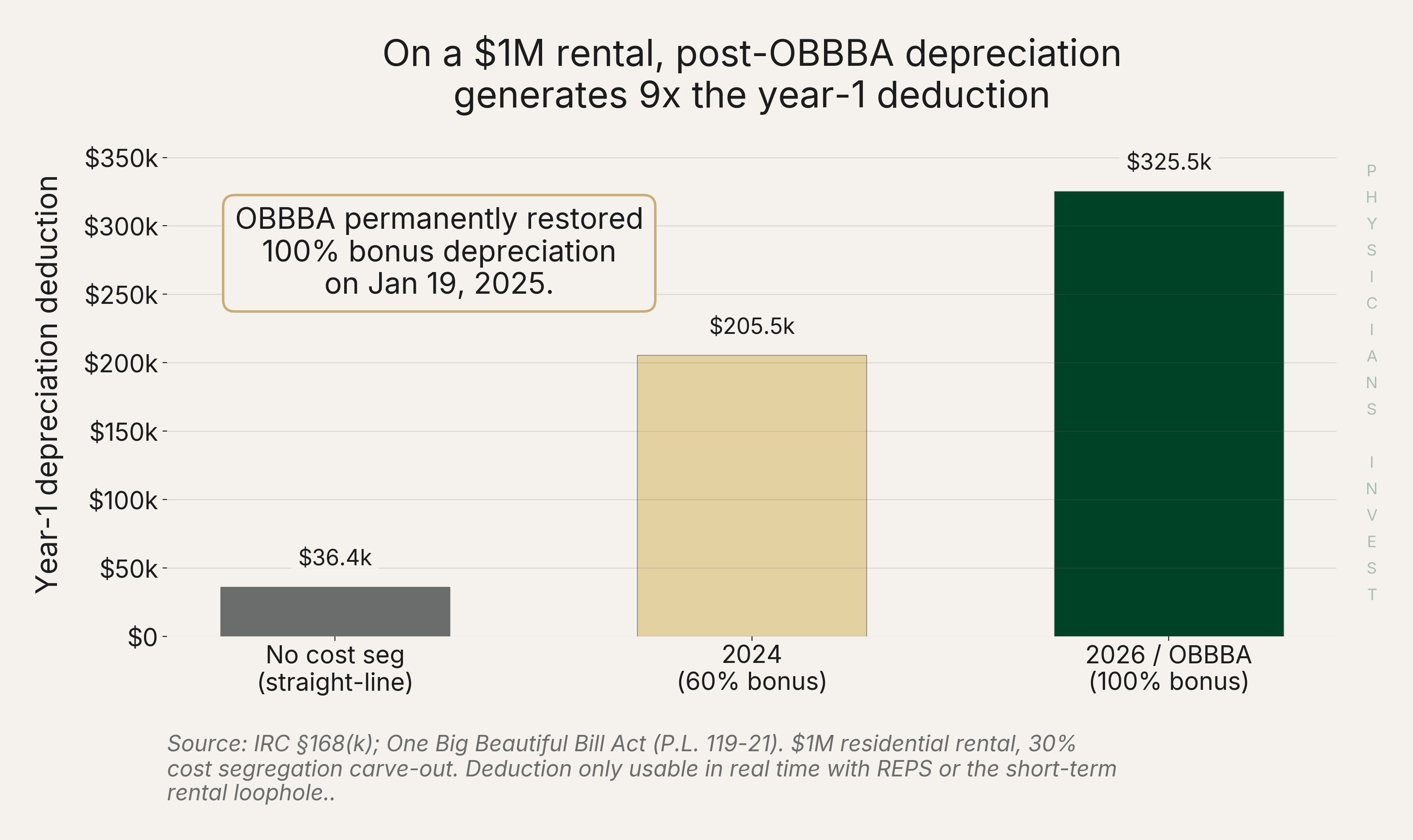

The good news: OBBBA, the One Big Beautiful Bill Act, permanently restored 100% bonus depreciation in 2025. With a cost segregation study (an engineering tax analysis focused on depreciation schedules), a $1 million rental throws off about $325,000 of Year-1 depreciation. Roughly nine times straight-line depreciation alone and almost 60% more than what was allowed before 2025.

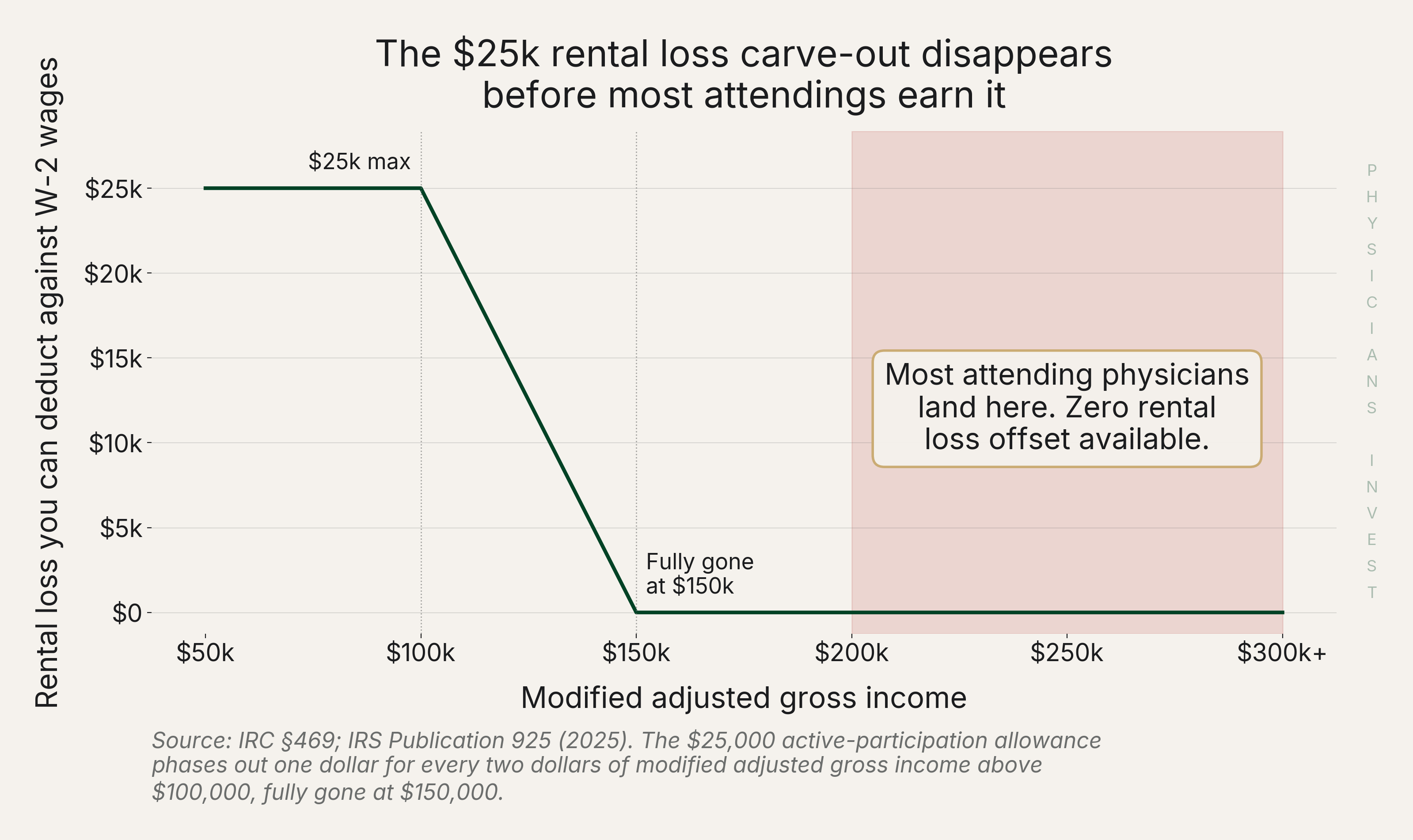

The bad news: Section 469 of the tax code makes rental real estate "passive per se." Rental losses cannot offset W-2 wages unless you take 2 courses of action. Qualify as a real estate professional (REPS, 750+ hours per year and more than half of your working time, only achievable by a non-working spouse or a truly part-time physician) or you run a short-term rental (STR) with an average customer stay of seven days or fewer. The $25,000 active-participation carve-out is pitched often in marketing but it phases out at $150,000 of modified adjusted gross income (MAGI). Most every attending crosses that threshold.

Without REPS or the STR loophole, that headline depreciation tax write-off sits on Form 8582 as a suspended carryforward. See the plots below to illustrate these points.

-

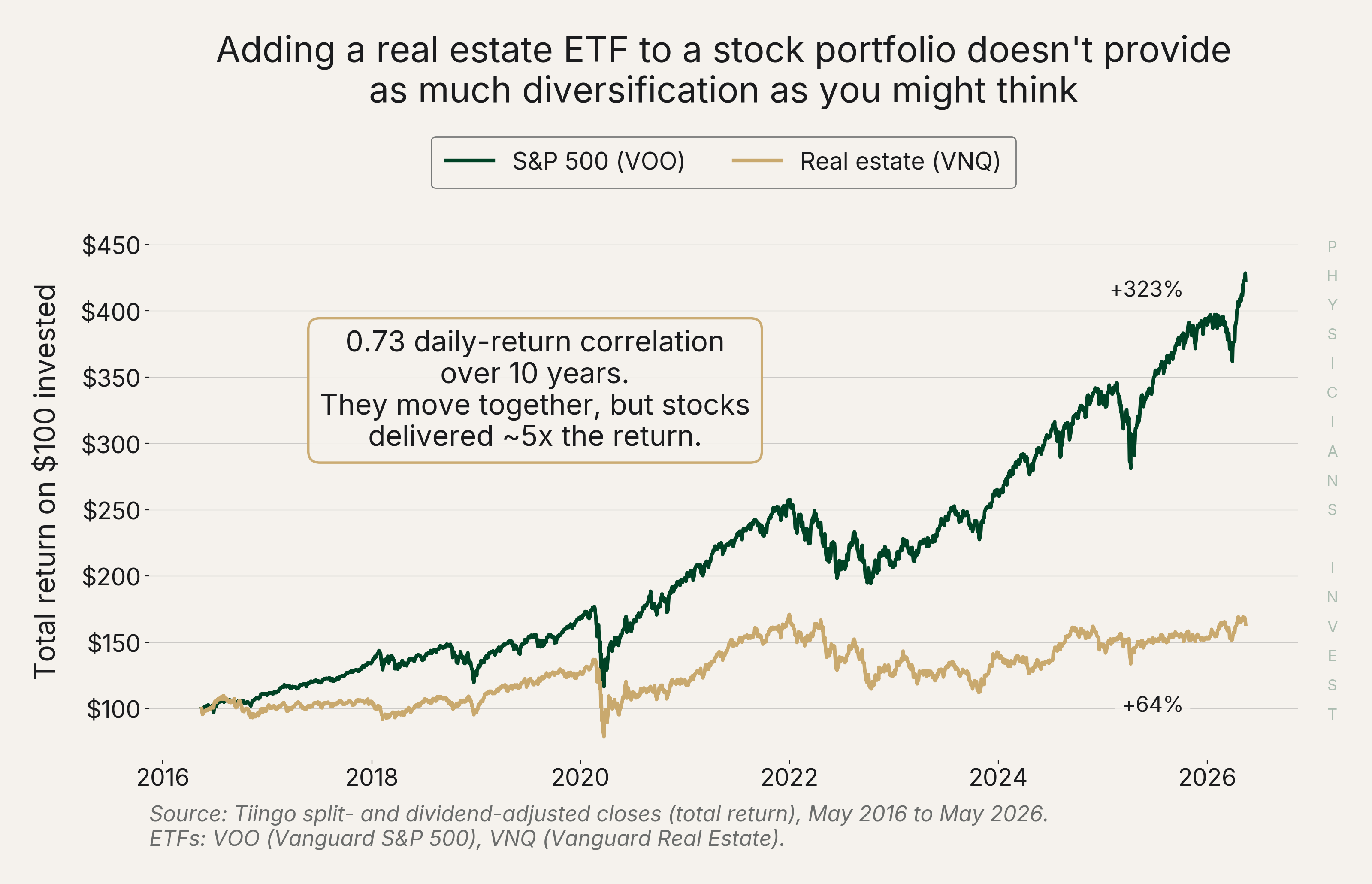

The diversification illusion. Adding a real estate ETF (exchange-traded fund, known as REITs, Real Estate Investment Trusts) to a stock portfolio does not diversify the way physicians often think. You must have private real estate exposure to get true diversification from the asset class.

REITs have a 0.73 daily-return correlation (a scale where 1.0 means they move in lockstep and 0.0 means they move independently) to the S&P 500 (author calculation from Tiingo price data, VNQ vs VOO). What does that mean? It means they move in a similar way, which is exactly the wrong way a diversifier should act. A true diversifier should have a correlation to the S&P 500 close to 0.0. With REITs, you are still exposed to a dangerous amount of market risk. They sell off at the exact same time as stocks, as the plot below over the last 10 years shows.

Cap Rates 101

Before we move on we need to discuss a piece of vocabulary that is always thrown around in real estate conversations.

Cap Rate.

Cap Rate = [Net Operating Income/Property Value]

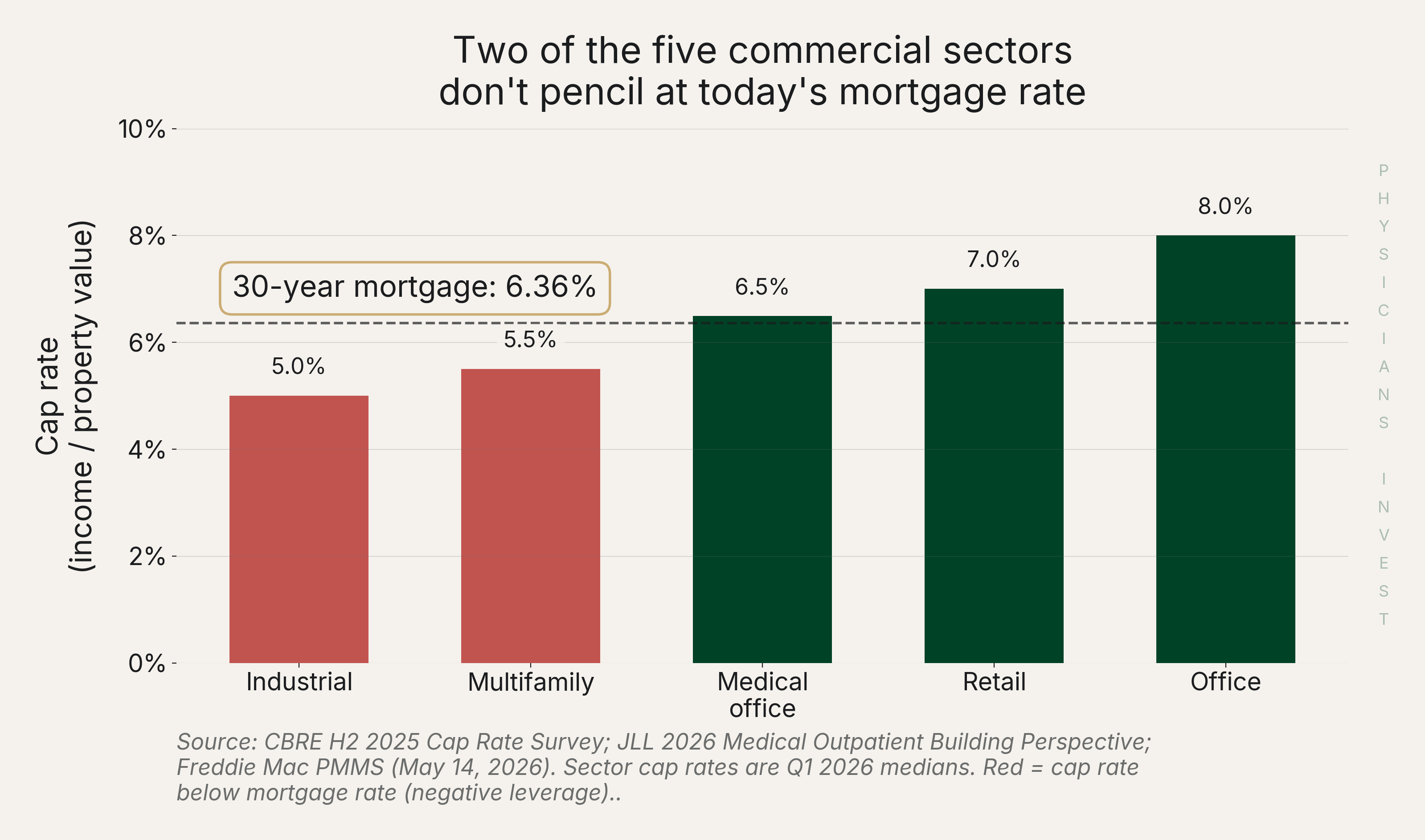

A cap rate is the unlevered cash yield on a property ("unlevered" just assumes that no debt is used). For example, a property generating $60,000 of net operating income at a $1 million price has a 6% cap rate. Lower cap rate equates to a more expensive asset. Higher cap rate equates to a cheaper asset. If you are buying real estate, you want high cap rates. If you are selling real estate, you want low cap rates. Cap rates are driven by the real estate market, as the denominator in the equation (property value) changes drastically based on market conditions.

The cap rate versus the mortgage rate tells you whether leverage (mortgage debt) helps or hurts.

- When cap rates are above the mortgage rate, leverage works and amplifies returns. This is the scenario when you hear from a friend how well their real estate investment did.

- When cap rates are below the mortgage rate, the property does not earn enough to cover its own debt and leverage amplifies losses. This is how real estate deals sometimes go bust.

Cap rate data from the CBRE H2 2025 Cap Rate Survey. Mortgage rate: Freddie Mac PMMS week ending May 14, 2026 (6.36%).

The Analysis

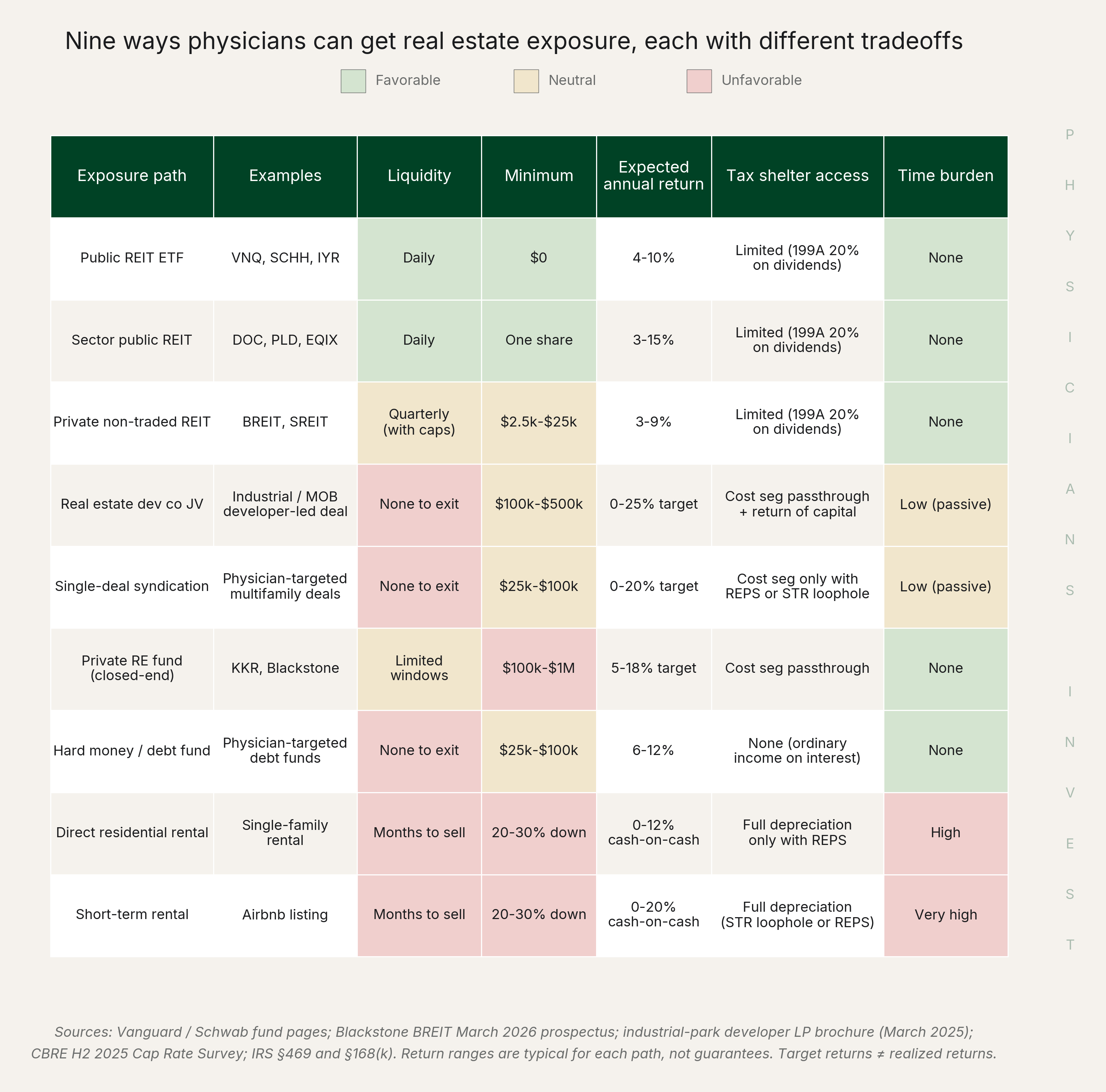

There are 9 common ways physicians invest in real estate. The table below shows these.

-

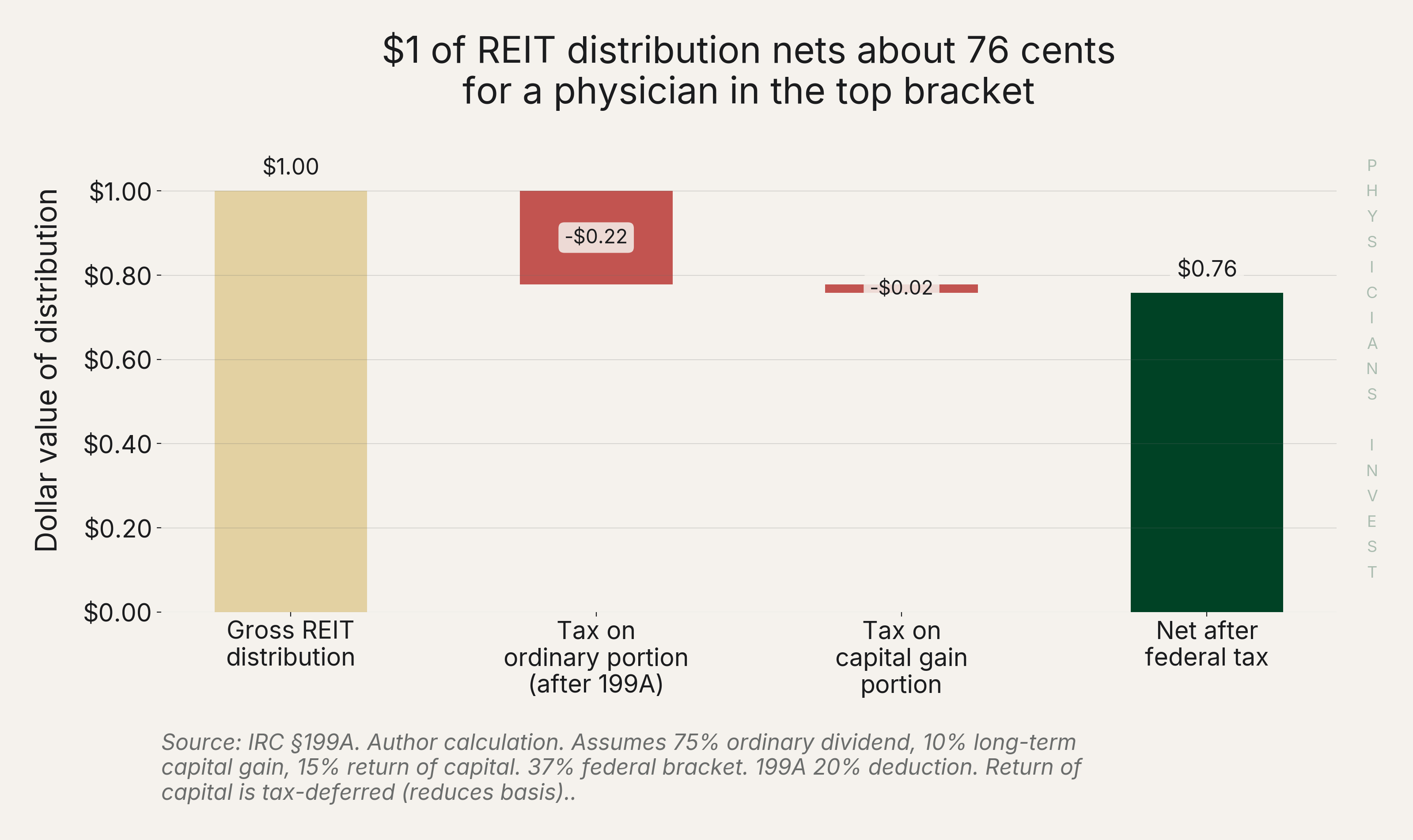

Public market REITs. These are ETFs (exchange-traded funds) like VNQ (0.13% annual expense ratio -- the fund's yearly cost as a percentage of assets -- with $69.9B in assets under management). Don't worry about the underlying mechanics, but these funds are required to distribute almost all of their income and must invest primarily in real estate. They are an easy way to get exposure to real estate but are more exposed to market risk than many investors think.

REITs tend to be most tax-efficient inside a retirement account because distributions don't get the same treatment as qualified dividends in a taxable brokerage. For most physicians that means considering them primarily for 401(k) or IRA allocations rather than a taxable account. REIT distributions tax as ordinary income with a limited 20% deduction under Section 199A of the tax code. That is materially worse than holding the broad market in a low-cost ETF where qualified dividends and long-term capital gains compound more efficiently. A REIT tax waterfall can be seen in the chart below.

-

Sector REITs. Sector REITs are just like public market REITs above but focus on a single sector of the real estate market like healthcare or data centers. These are for more advanced investors who know how to do market analysis or feel strongly that they want to "tilt" their portfolio toward a sector.

-

Private REITs. Private REITs are offered by private investment firms like Blackstone. They are less liquid than public market REITs and are somewhat of a middle ground between public market REITs and private real estate investments. They are typically well run and well diversified but don't offer high upside.

-

Real Estate Development Company. These companies offer exposure into full development projects, taking a property from pure dirt to a fully leased building. They can generate much higher returns than REITs by executing the full development cycle. They rarely offer cashflow and can be seen as more of an equity investment than an income investment. Because of the multi-step process of real estate development and because these firms use a fair amount of debt, they carry a wider range of outcomes than REITs.

-

Single-Deal Syndication. These are single projects that a sponsor puts together, raising private capital for one deal. This increases risk because investors are concentrated and not diversified. It is also illiquid, so investors cannot easily take their money out. The risk of losing your entire investment is real here. Tides Equities and Lurin Capital are recent examples of limited partners losing most or all of their principal in multifamily syndications. That risk also comes with some nice upside if the project works out.

-

Private Real Estate Fund. These investments are hard for physicians to access. They are open mostly to institutional investors and family offices and focus on large-scale developments that are often in prime locations. This is a great way to gain real estate exposure if you can get into funds like these: private, passive, and with institutional governance.

-

Hard-Money Real Estate Debt Fund. These funds lend money to private real estate developers. They offer consistent cash flow, which is why many people allocate to them, but they have three issues investors should know about.

- They are tax inefficient. All interest comes back as ordinary income. Because of this, these funds are most tax-efficient when held inside a tax-advantaged account. A self-directed IRA is one vehicle that can hold them.

- They don't have upside. Your returns are capped at typically 9-11% annually. For a private investment where your money is locked up for a long time, that is too low. For physicians who want income without the tax drag, investment-grade or high-yield public bond funds offer similar yield in a more liquid, tax-efficient wrapper.

- They are on the wrong side of inflation. Inflation is a headwind, not a tailwind, to the returns of this asset class. These investments act more like an illiquid bond than an inflation-hedged equity investment.

-

Private Long-Term Rental. This is your classic rental property where you own the asset yourself and rent it out. Very time intensive and it can come with headaches, but it comes with strong advantages. You own the property, you access tax loopholes if you or your spouse qualify for REPS, and you have strong upside. This requires significant time and paperwork to do correctly and is in no way "passive."

-

Private Short-Term Rental. This is the Airbnb asset class. It unlocks tax advantages with the STR loophole and can be a great long-term investment. With that said, it comes with ever-increasing regulatory risk and also requires the use of a dedicated property manager as the property is constantly turning over. These can be very lucrative investments when done correctly but are the biggest time commitment out of all the investment options.

The Move

Career stage playbook:

-

Resident or fellow: No need for real estate exposure. Avoid private real estate unless you purchase a property that is house-hack-able (rent rooms, cover the mortgage) and not over-levered.

-

Early-career attending: No need for real estate exposure. If a down payment on a home or a private investment is more than 25% of your investable assets, you should hold off. Focus on building equity exposure instead of real estate exposure at this stage.

-

Mid-career attending ($1M+ net worth): Start seriously evaluating real estate. Public REITs in retirement accounts only. Private deals with full diligence.

- Spouse who qualifies for REPS or runs STRs: The strongest legal path to offset high W-2 income. Worth the operational effort if your situation is configured for it.

-

Senior attending or partner ($5M+ net worth): Enough capital to spread across multiple real estate vehicles: short-term rentals, long-term rentals, real estate funds, and commercial deals. No single path needs to dominate.

-

Retirement: Real estate shifts from investment to estate-planning tool. Real estate has advantages and disadvantages when it comes to estate planning and it is worth talking to an estate planning expert on the best way to handle your real estate portfolio.

Four diligence questions before any private check goes out:

- What is the sponsor's full track record of realized exits? Ask for proof.

- Will three current limited partners let you call them? Investing in a private deal blind is dangerous.

- Does the deal pencil at the current rate environment, or only if rates fall?

- Is the fee structure tied to performance, or do the sponsors collect regardless?

Overall, real estate is a great investment but it needs to earn its place in your portfolio. It is not as easy as just buying a property and good things happening.

Sources

Policy

- IRC § 469 (Passive Activity Loss Rules), Cornell LII — statutory basis for rental real estate's "passive per se" classification

- IRS Publication 925 (2025) — $25,000 active-participation carve-out and phase-out at $150,000 MAGI

- One Big Beautiful Bill Act Provisions, IRS — permanent restoration of 100% bonus depreciation for property placed in service after January 19, 2025

- IRS Interim Guidance: Additional First-Year Depreciation, IRS (2026) — OBBBA transition rules

- IRS Finalizes Section 199A Safe Harbor for Rental Real Estate — 20% QBI deduction basis for REIT distribution tax math

Tax / Legal Analysis

- Real Estate Professional Status (REPS) Guide, The Real Estate CPA — 750-hour and more-than-half REPS qualification requirements

- REPS Tax Benefits, Cherry Bekaert — IRS audit scrutiny of REPS time logs

- Real Estate Professional Tax Benefits: 2025 IRS Rules, Anomaly CPA — married-filing-jointly REPS rules

- Short-Term Rental Tax Rules Explained, Cherry Bekaert — 7-day-or-fewer average customer stay rule converting STR from passive rental to trade or business

- Short-Term Rental Tax Loophole, WCG CPAs — material participation requirements for STR loophole

- Passive Activity Loss Rules, Nolo — $150,000 MAGI phase-out plain-language explanation

- OBBBA Impact on Real Estate, Citrin Cooperman — cost segregation + 100% bonus depreciation mechanics

- OBBBA Restores and Expands Bonus Depreciation, RSM — 5-, 7-, and 15-year cost-seg buckets eligible for 100% expensing

Data

- Freddie Mac Primary Mortgage Market Survey — 30-year fixed mortgage rate 6.36% (week ending May 14, 2026)

- CBRE H2 2025 U.S. Cap Rate Survey — cap rates by sector used in cap-rate vs mortgage-rate chart

- VNQ ETF Profile, Vanguard — VNQ expense ratio, yield, assets under management

- REIT Average & Historical Returns vs. U.S. Stocks, Nareit — long-run REIT vs equity return comparisons

- Tiingo Financial Data — VNQ and VOO daily price data; source for 0.73 correlation and 10-year return comparison (author calculations)

- Medscape Physician Wealth & Debt Report 2026 — 30% of physicians hold rental property as a non-retirement investment

- JLL 2026 Medical Outpatient Building Perspective — MOB 92.3% occupancy, cap rate compression to 6.49%, 78% Q1 2026 investment volume surge

Industry / News

- Tides Equities Principals Sued for $40M, The Real Deal (May 2025) — Tides and Lurin as examples of LP principal loss in single-deal syndications

- Inside Lurin Capital's Syndication Mess, The Real Deal (January 2026) — Lurin Capital syndication unwind

- Starwood Freezes SREIT Redemptions, The Real Deal (May 2026) — private REIT liquidity risk: SREIT outright redemption freeze

- BREIT March 2026 Prospectus Supplement, SEC — BREIT 2% monthly / 5% quarterly repurchase cap

- How High-Earners Use REPS to Slash Tax Bills, Wall Street Journal via DNYUZ (Feb 2026) — REPS strategy current news coverage