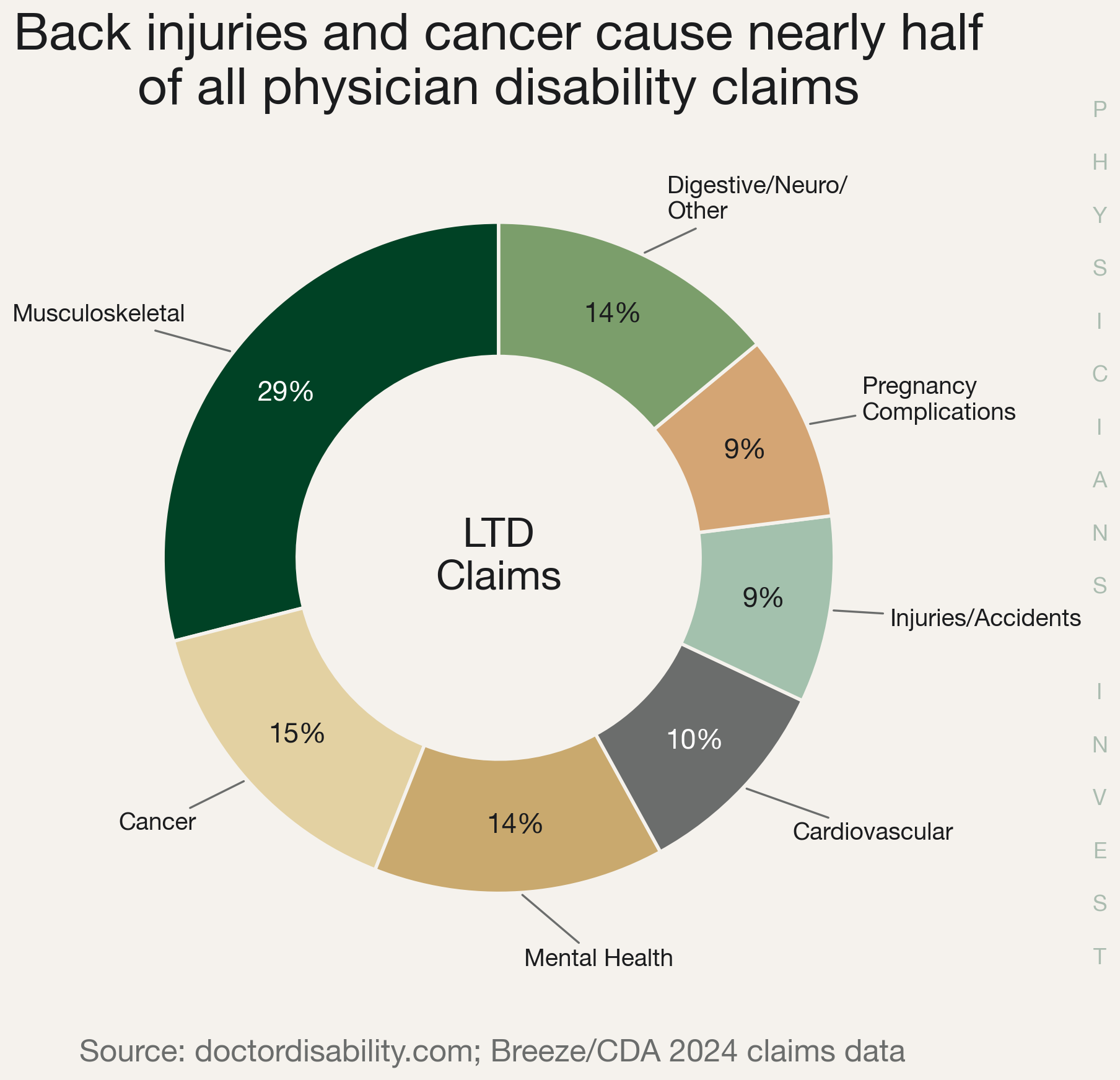

The 2-Minute Version

- Your employer's group LTD probably replaces only 24% of your income after taxes. That's a problem.

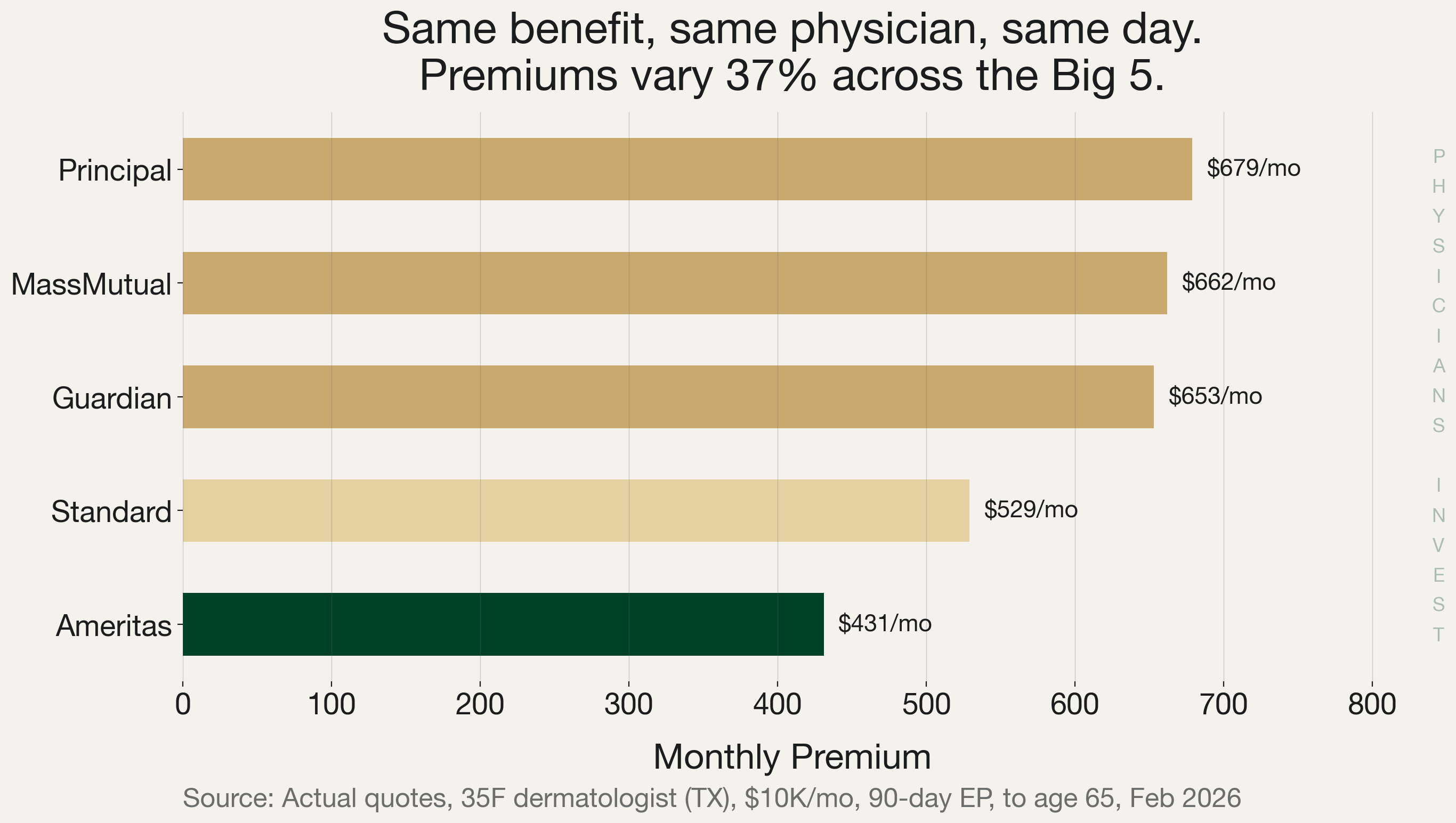

- We got real quotes from all Big 5 carriers for the same physician. Premiums varied 37% for similar benefit.

- Five settings are universal. Everything else depends on your specialty, savings, and family situation.

Most physicians assume their employer's disability coverage is enough. It's an easy assumption to make. But the gap between what employer group LTD actually pays and what you'd need to maintain your life is bigger than most attendings realize. We shopped own-occupation disability insurance across all five major carriers for the same physician on the same day. What we found should change how you think about this product.

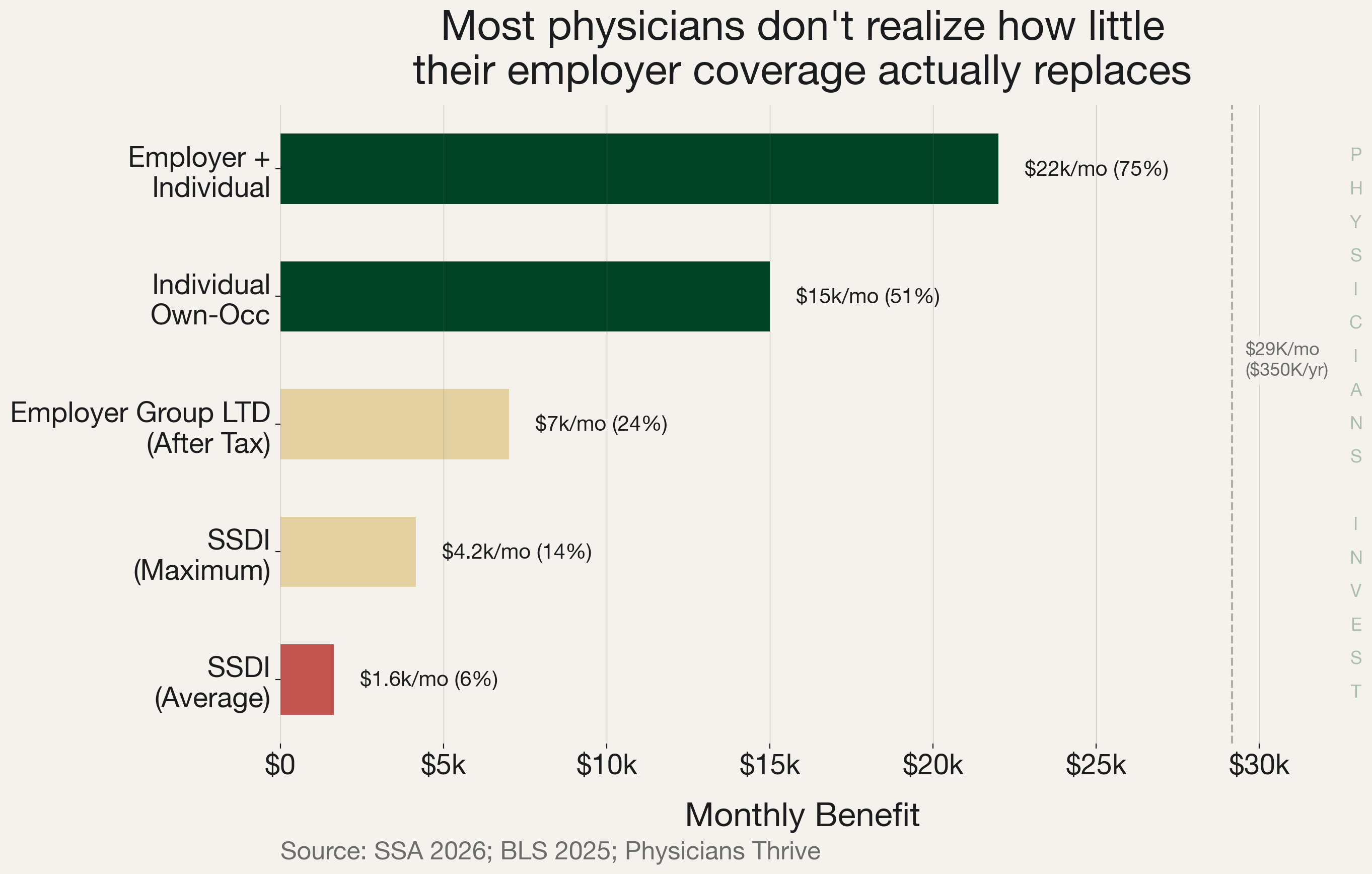

Here's the gap. Social Security Disability Insurance (SSDI) is a federal program available at any working age, not just 65+, that pays benefits to workers who can no longer perform "any substantial gainful activity." The average monthly benefit? $1,630. That's 6% of a $350K salary.

Your employer's group LTD caps at maybe $10,000/month, uses an "any occupation" definition -- meaning a surgeon who can teach gets nothing -- and the benefit is taxable if your employer pays the premiums. After taxes, roughly $7,000/month. That's 24%.

An individual own-occupation policy fills that gap. True own-occ means a dermatologist who can't perform procedures but could do telemedicine still collects the full benefit AND earns income in the new role. It is the most physician-specific financial product on the market.

The industry is priced to win

These are billion-dollar insurance companies. Guardian alone manages $80 billion in assets. Every carrier employs actuaries with massive datasets, and every policy, every rider, every "golden window" discount is priced so the insurer comes out ahead.

That's the business model.

The people who offer insurance are not charities. That reframes every decision you make here. Insurance is catastrophe prevention. Full stop. If a scenario wouldn't be financially catastrophic, you don't need to insure it.

What we found when we actually shopped it

We got quotes from all five major carriers for the same physician -- 35-year-old female dermatologist in Texas, $10,000/month benefit, 90-day elimination period, coverage to age 65. Same benefit. Same day. Same broker. Premiums ranged from $431/month at Ameritas to $679/month at Principal.

$248/month spread. Almost $3,000 a year for the same base benefit; over a 30-year career, that's nearly $90,000 in premium difference. The gap isn't mainly about policy quality. It's about occupation class -- the risk tier each carrier assigns to your specialty. Ameritas classified this dermatologist as 6M, their lowest-risk medical tier. Guardian classified the exact same physician as 4M, a higher-risk tier. The carrier's internal classification drove more of the price gap than any difference in actual coverage.

Ordering off the own-occupation disability insurance menu is like going to the Cheesecake Factory. So many options that after 30 minutes of menu flipping you still don't know what you want. A plethora of decisions creates indecision. So we built a simpler framework.

Turn your brain off for these five things

| Setting | Default | Why |

|---|---|---|

| Definition | True own-occupation (not modified, not transitional, not any-occ) | Modified own-occ pays you to NOT work. True own-occ lets you work in another role and still collect. |

| Cancelability | Noncancelable + guaranteed renewable | Premiums locked for life. |

| Elimination period | 90 days | 30-day costs nearly double. 180-day saves $10-$20/mo. Not worth it. |

| Benefit period | To age 65 | Shorter periods save little. |

| Carrier | Big 5 only | Guardian, MassMutual, Standard, Principal, Ameritas. Everyone else has weaker definitions. |

Everything else depends on your specialty, your savings, whether your spouse works, and your loan situation. That's where the real decisions live. And yes, the cheapest carrier (Ameritas) has weaker financial ratings than Guardian or MassMutual. But there's a threshold of not being good versus being good, and all five are above it.

When to stop paying

No insurer talks about this because the answer hurts insurance sales. But at some point, your net worth makes disability insurance unnecessary. If your invested assets cover 15x your annual spending and your loans are paid off, a disability wouldn't be catastrophic. It would be a lifestyle adjustment. At $200K in annual spending, that's $3M invested -- enough to generate $120K/year at a 4% withdrawal rate. Combine that with what you could still earn in a different capacity (true own-occ lets you work), and you're covered.

The math changes with a working spouse, young kids, or a practice with overhead. But the principle holds: reassess every few years. The right policy at 32 might be an unnecessary expense at 50.

The Move

- Get a specific broker recommendation. Ask a physician colleague or use a vetted list from WCI or Physicians Invest. Don't Google it and land in a quagmire.

- Read up before the call. You want to ask pointed questions about occupation class, mental health limitations, and FIO terms. Going in blind means you'll nod along.

- Lock in the five defaults above. Don't debate these.

- Size your benefit to your actual spending. Your emergency fund covers the 90-day elimination period. Your benefit covers what you'd actually need monthly.

- Reassess at every career milestone. New job, new savings milestone, kids leaving. Your need changes; your policy should too.

One more thing. The often-cited "1 in 7 physicians will become disabled" statistic has no verifiable primary source. Every article cites it... yet nobody can trace it. We tried. The closest verifiable number comes from the SSA: "a 20-year-old worker has a 1-in-4 chance of becoming disabled before reaching full retirement age." But that's the general population, and we think physicians as a demographic are healthier and more proactive. The insurance industry has every incentive to make the number sound scarier than it is.

Buy disability insurance. Buy it because a catastrophic disability with $300K in loans and two young kids would be devastating. Buy it with clear eyes about what you're buying and from whom. And plan to stop buying it someday.

Sources

Data

- SSA 2026 Disability Facts

- SSA SSDI Benefits Chart (2026)

- BLS Employee Benefits Survey 2025

- Milliman 2025 IDI Market Survey

- Breeze/CDA Disability Statistics

- IRS: Disability Insurance Tax Treatment

Physician-Specific

- White Coat Investor: Best DI Companies

- White Coat Investor: Elimination Period

- Guardian: Own-Occupation DI

- Student Loan Planner: Occupation Class

- Physicians Thrive: Group Disability

- DoctorDisability.com: Statistics

Proprietary

- Actual carrier quotes obtained February 2026 via DoctorDisability.com for a 35F dermatologist in Texas