The 2-Minute Version

- Only three financial credentials matter: CFA, CFP, and CPA. Everything else is noise.

- Credential stacking is a red flag, not a strength. Nobody at Goldman or Blackstone lists four designations.

- Evaluate your current advisor. Either go DIY for average, or pay up for truly exceptional. The worst spot is paying for average you could get yourself.

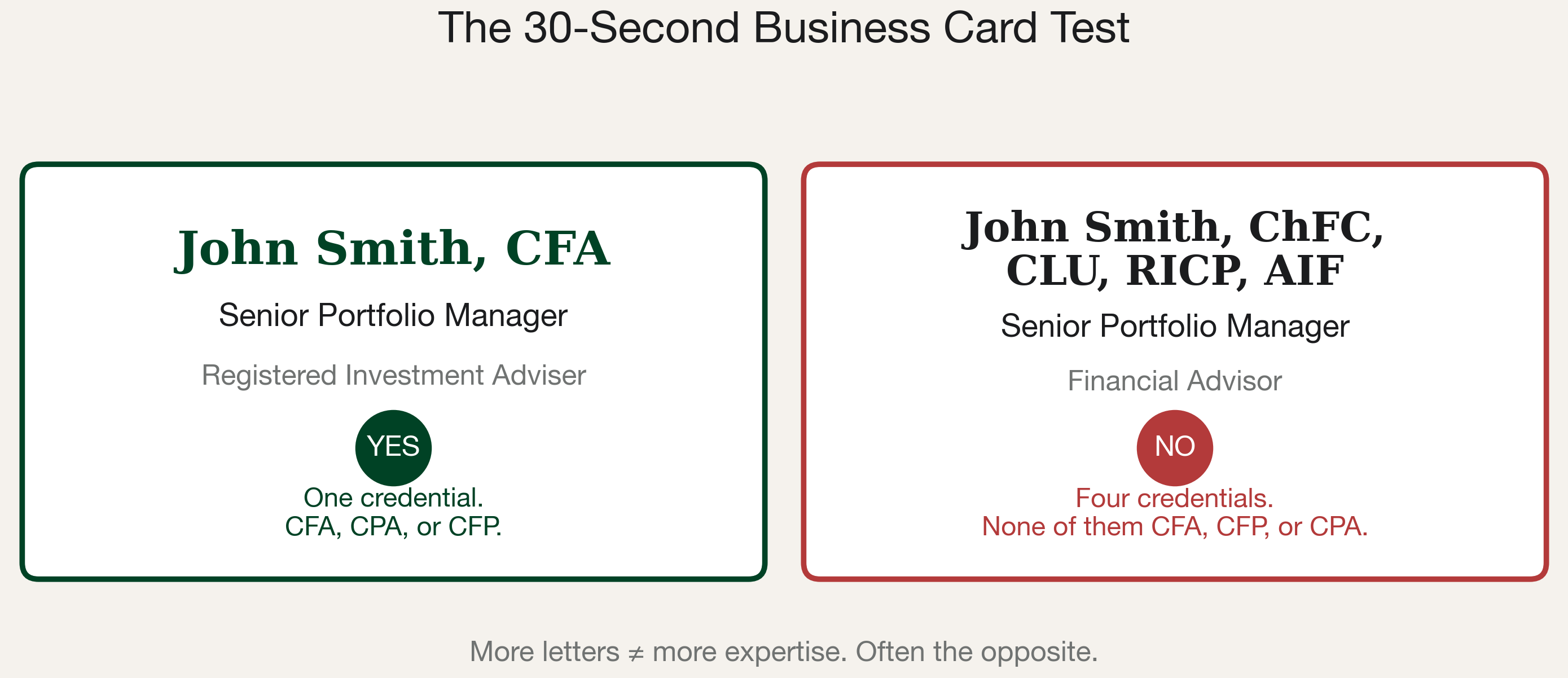

You're at a physician financial planning dinner. The advisor hands you a business card: "John Smith, ChFC, CLU, RICP, AIF." Four credentials. None of them CFA, CFP, or CPA.

That should bother you.

The Alphabet Soup Problem

FINRA tracks over 250 financial designations. That's up 45% from a decade ago. More than half include "certified" or "accredited" in the title. The part that should make you uncomfortable: the titles "Financial Advisor," "Financial Consultant," and "Wealth Manager" are completely unregulated. Anyone can use them. No exam. No license. No oversight.

You trained for 11 to 16 years. Passed three USMLE steps. Survived residency. Got board certified. When you see "Certified" on a business card, you instinctively assign it the same weight as your own credentials. That instinct is being exploited.

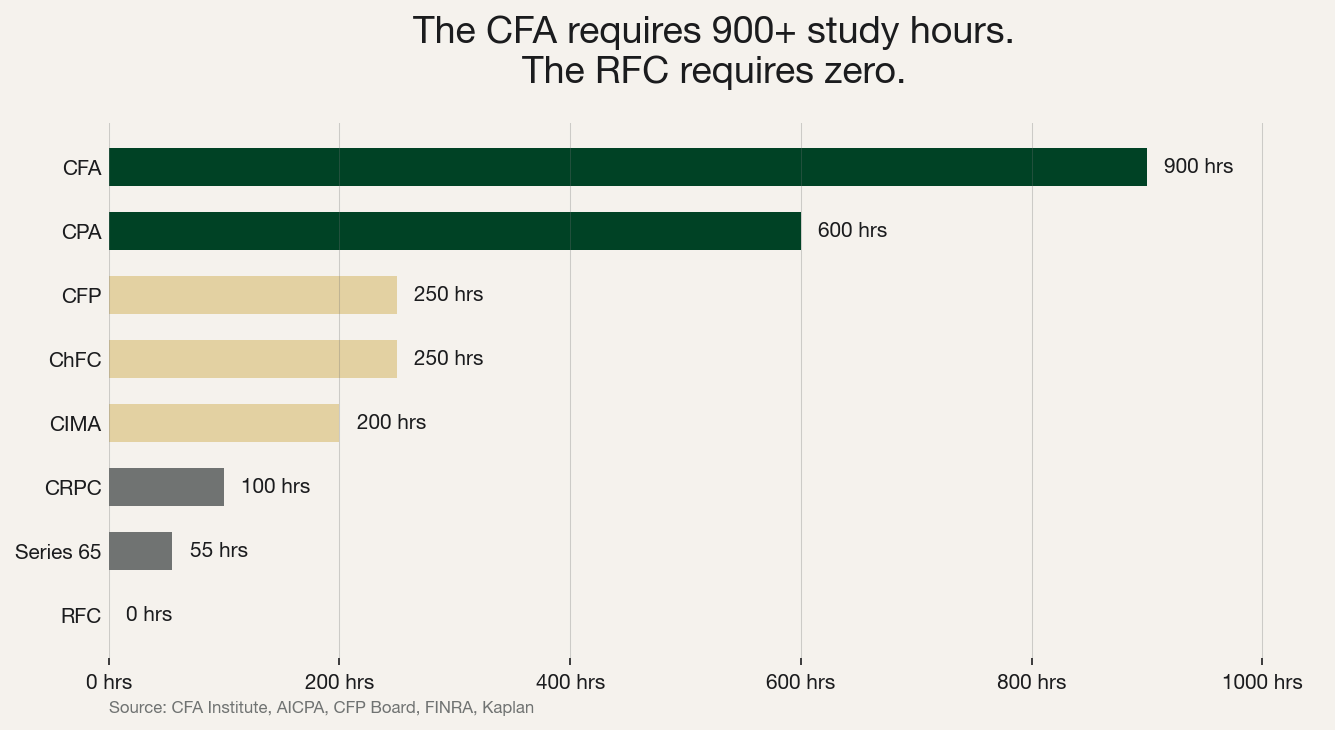

The CFA requires 900+ hours of study across three exams over 3+ years, with a 44% pass rate per level. The RFC requires zero hours, zero exams, and $350. Both can call themselves "financial advisors." (Yes, really.)

Source: CFA Institute, AICPA, CFP Board, FINRA, Kaplan

Source: CFA Institute, AICPA, CFP Board, FINRA, Kaplan

What Actually Matters

We think there are exactly three credentials worth respecting: CFA, CPA, and CFP. In that order.

The CFA is the gold standard. The competitive fellowship of finance. Designed to keep people out. The CPA is your boards. Four-part exam, state licensing, continuing education. Essential if your advisor touches anything tax-related. The CFP is graduating medical school. Baseline competence. Table stakes for a financial planner. Not the ceiling.

Here's the tell nobody talks about: credential stacking is inversely correlated with quality. Look at the top firms in the country. Blackstone. Bridgewater. Goldman Sachs. The people there might list CFA or CPA. Nothing beyond that. It's people at less reputable firms with less experience who stack four or five designations. Ask yourself: have they spent all their time getting credentials rather than truly learning their craft?

Here's the full breakdown. Save this.

| Credential | Study Hours | Medical Equivalent | Verdict |

|---|---|---|---|

| CFA | 900+ | Completing a competitive fellowship. Three grueling exams over 3+ years. | Gatekeeper. The gold standard. |

| CPA | 600 | Passing your boards. Four-part exam, state licensing, continuing education. | Gatekeeper. Essential for tax-focused advice. |

| CFP | 250 | Graduating medical school. Baseline competence. Residency is what makes you good. | Table stakes. Minimum for a financial planner. |

| CAIA | 400 | Subspecialty fellowship. Two exams, alternatives-focused. | Solid specialist. Alternative investments only. |

| ChFC | 250 | An accredited residency program. Different path, same effort as CFP. | Solid specialist. Same issuer as CLU. |

| CLU | 250 | Completing a pathology residency, then advising on surgery. Deep insurance training. | Solid for insurance. Red flag if they're selling you investments. |

| CIMA | 200 | Subspecialty certificate. Focused, respectable, narrow. | Solid specialist. Investment management only. |

| CRPC | 110 | A weekend CME course. You attended. You got a certificate. | Moderate. No prerequisites. |

| Series 7 | 80 | Getting your medical license. Permission to practice, not proof of expertise. | Entry-level license. The broker's ticket to sell securities. |

| Series 65 | 55 | Passing USMLE Step 1 and stopping. You cleared the minimum bar. | Entry-level license. Necessary, not sufficient. |

| RFC | 0 | Buying a white coat on Amazon. | Noise. $350 and a signature. Run. |

Sources: CFA Institute, AICPA, CFP Board, CAIA Association, FINRA, Kaplan

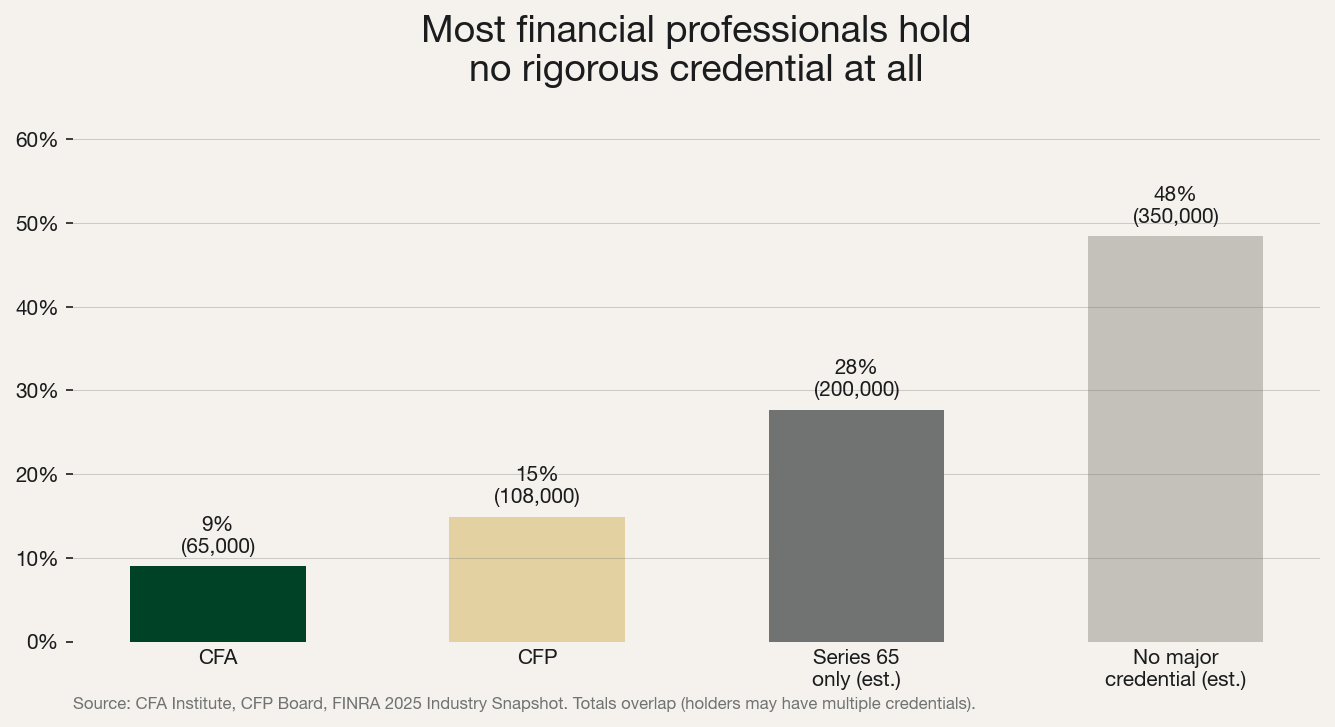

Only 9% of registered financial professionals hold a CFA. Just 15% hold a CFP. Nearly half hold no rigorous credential at all, per the FINRA 2025 Industry Snapshot. The person managing your money is more likely to have zero meaningful credentials than to hold either of the two that matter most. Let that sink in.

Source: CFA Institute, CFP Board, FINRA 2025 Industry Snapshot

Source: CFA Institute, CFP Board, FINRA 2025 Industry Snapshot

The Move

Be a skeptic. Many of the people in this industry hold themselves out to be much smarter or much more talented than they actually are.

Here's what we'd do:

First, look up your current advisor on FINRA BrokerCheck and the SEC's Investment Adviser Public Disclosure database. Check their credentials against the cheat sheet in this issue.

Second, decide what you're paying for. If you're getting average service, you're smart enough to get average on your own for almost nothing. The worst spot is paying for average when you could have done it yourself.

Third, if you have the net worth and connections to access a truly top-tier wealth management firm (one that treats your finances like a single family office), have the conversation. The best plastic surgeon in the world doesn't charge what a new grad charges. That dynamic exists in finance too.

Rip the Band-Aid off if you need to. Your financial future is too important to outsource to someone whose most impressive credential took a weekend to earn.

Sources

Data

- FINRA Professional Designations Database

- FINRA 2025 Industry Snapshot

- CFA Institute Exam Overview

- CFP Board: Milestone Year Topping 100K Certificants

- CFA Pass Rates and Study Hours

Analysis

Tools