The 2-Minute Version

- Most physician income levels phase them out of being able to directly contribute to Roth IRAs. The backdoor method becomes necessary if you want to make a Roth IRA contribution but it introduces a few complexities.

- One old pre-tax IRA (traditional, rollover, SEP, or SIMPLE) can turn your "tax-free" backdoor Roth IRA conversion into a highly taxed trap.

- The fix: roll your pre-tax IRA money into a 401(k) or 403(b) first, then perform the backdoor Roth IRA conversion.

- If you are late career or early retirement and carry a large pre-tax balance, we will show you the calculus on if it is worth paying the taxes to convert into Roth IRAs.

The Dollar Math Let's assume a physician has $100,000 in pre-tax IRA accounts, like a Traditional IRA. When they make a contribution to their Roth IRA through the backdoor method they will still be taxed on the large majority of that contribution due to the pro-rata rule. This would cost that physician over $2,000 in taxes that year and for each subsequent year that they do the same thing. By rolling the Traditional IRA to an "employer" account, they will save 100% of those tax dollars they would have otherwise paid.

You were told to do a backdoor Roth IRA contribution by a well-meaning friend but they forgot to mention the aggregation rule. You follow the online guides and contribute $7,500 after-tax dollars to a Traditional IRA, convert it the next day into a Roth IRA, and expect zero tax. Then you find out that the $100,000 sitting in an old Traditional IRA just made 93% of that Roth conversion taxable. I ran into this exact trap early on in my career, before I knew about the rule, which was frustrating and annoying to re-correct.

The Setup

First, why bother converting from a Traditional IRA to a Roth IRA at all? Don't I want the tax write-off of the Traditional IRA today when my income is high? This thought process assumes you will make much less in retirement than you do today but my hope is that all physicians are making top tax bracket income for the entirety of their retirement life due to sound investing, financial decisions, and business ownership. A Traditional IRA buys you a write-off today at a guaranteed high bracket, on the bet that your rate will be lower later. I don't believe that bet. US taxes are likely higher down the road, and most physicians should structure their financial lives where they keep generating real income deep into their retirement years. A seven-figure Traditional IRA throws off forced taxable withdrawals starting at age 73 (known as RMDs, required minimum distributions). Under current law, a Roth IRA protects you from tax indefinitely, and it has no required distributions. My case for Roth IRA over Traditional IRA is simple: eliminate the possibility of any sort of tax forever rather than betting on your financial life being mediocre in retirement.

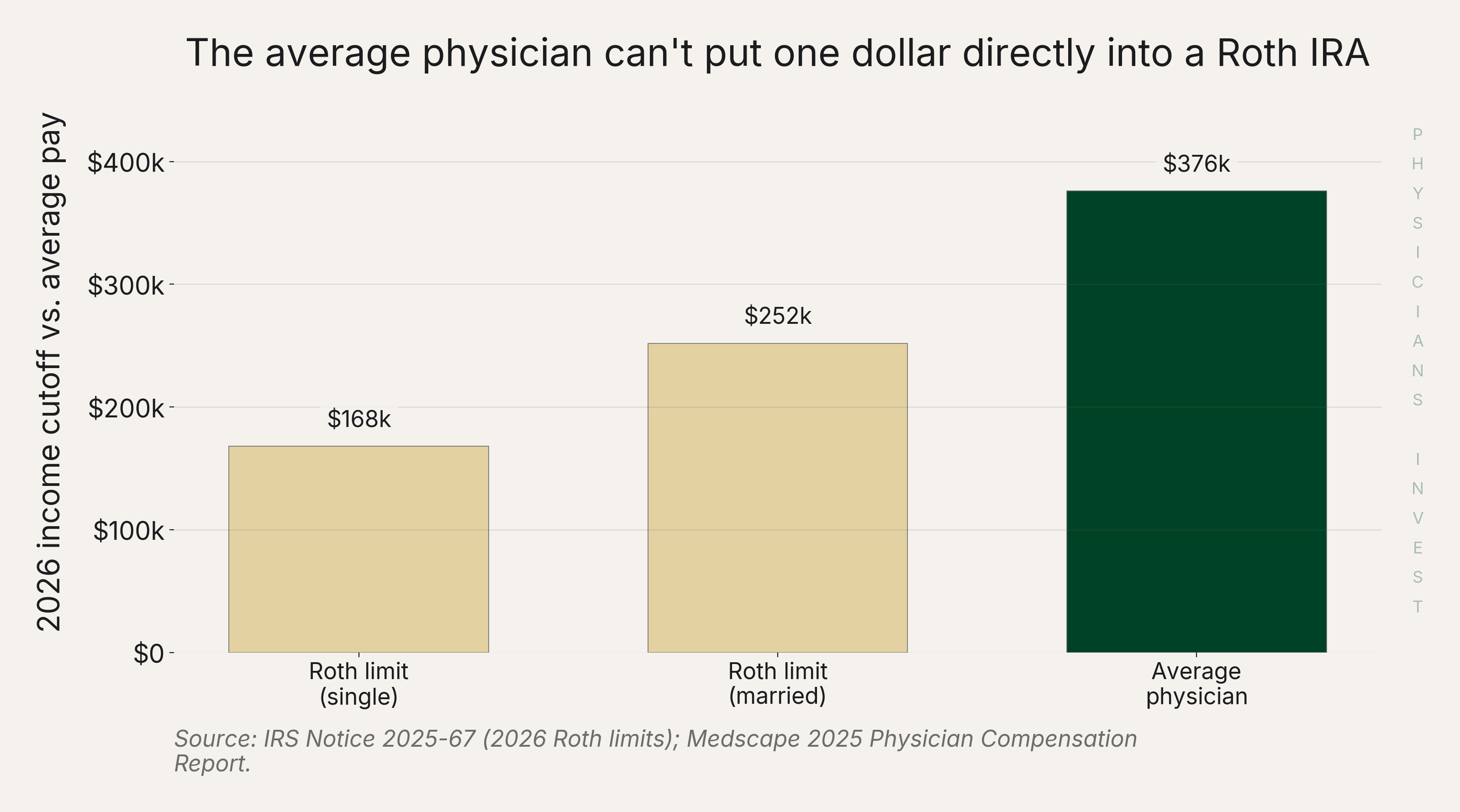

The problem with Roth IRAs is that pretty much every physician is phased out of being able to allocate because they exceed the upper income threshold. Per IRS Notice 2025-67, a direct Roth contribution phases out at $168,000 of income (technically modified adjusted gross income, or MAGI) for a single filer and $252,000 for a married couple in 2026. The Medscape 2025 Physician Compensation Report puts the average physician at about $376,000. You can see the disparity visually in the chart below.

Source: IRS Notice 2025-67; Medscape 2025 Physician Compensation Report

Source: IRS Notice 2025-67; Medscape 2025 Physician Compensation Report

This makes the backdoor Roth IRA contribution method the only door physicians can use. The process is to contribute after-tax dollars to a nondeductible Traditional IRA, then, as soon as it settles, convert it to Roth IRA within your platform, then you're done. By the way, all the major custodians of IRAs make this process easy but if you need help, please reach out to us. The issue with this simple method arises if you have any account balance in any pre-tax IRAs and it makes the tax on the conversion brutal when it should otherwise be tax-free.

The Analysis

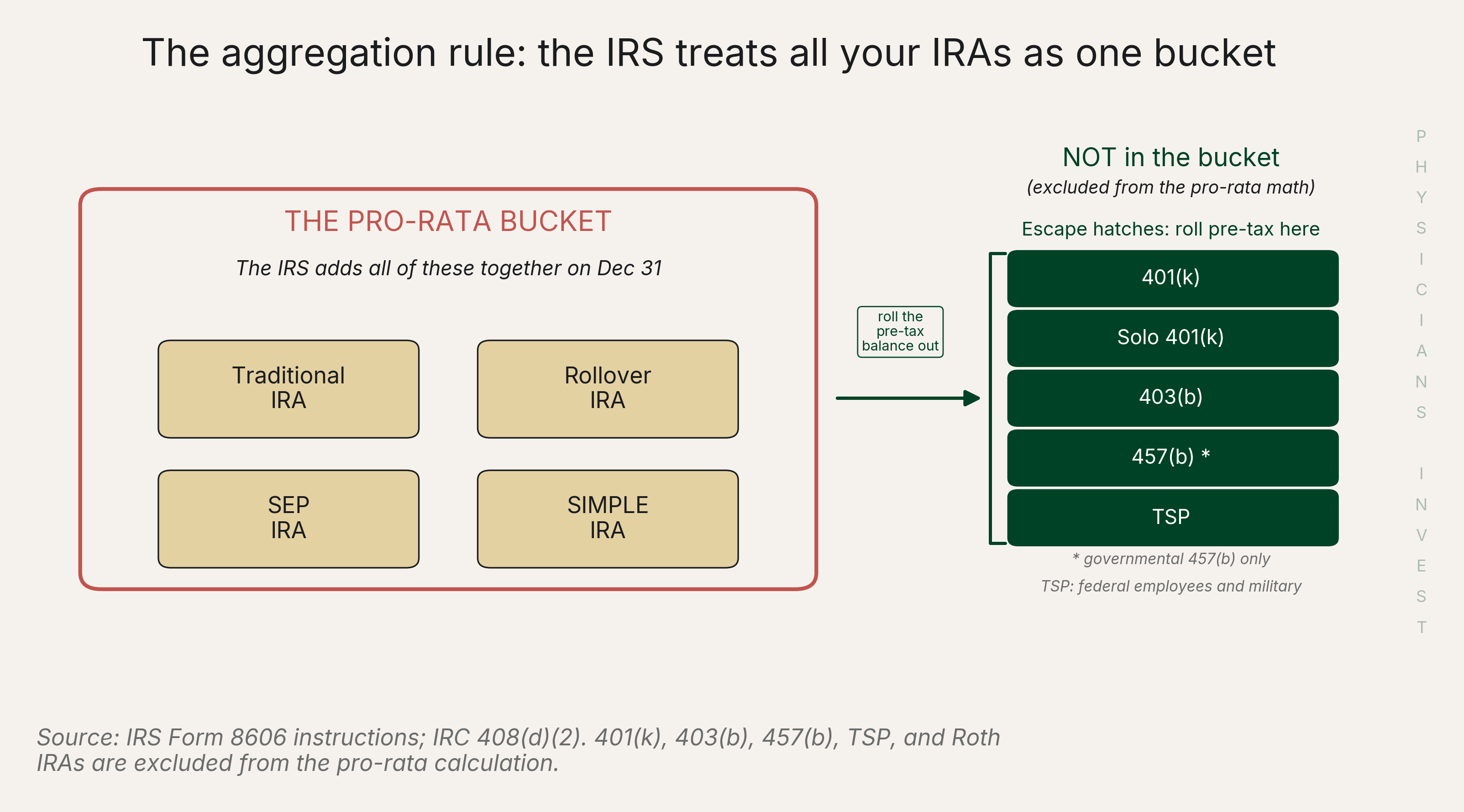

The IRS sees all your IRAs as one bucket

The big hiccup in all this is a thing called the "Aggregation Rule" that then trips the "Pro-Rata Rule". What do all these rules mean? Let's start with the Aggregation Rule. It's called "aggregation" because the IRS views the balance of all of your IRAs (except Roth IRA) together (ie. "in aggregate") in order to determine tax implications. On December 31 each year, the IRS treats all traditional, rollover, SEP, and SIMPLE IRAs as a single pool for tax purposes, aggregated under IRC §408(d)(2). Your Roth IRAs and your employer plans [401(k), 403(b), 457(b), TSP] sit outside that pool and don't count towards the total. The graphic below displays this visually.

Source: IRS Form 8606 instructions; IRC 408(d)(2)

Source: IRS Form 8606 instructions; IRC 408(d)(2)

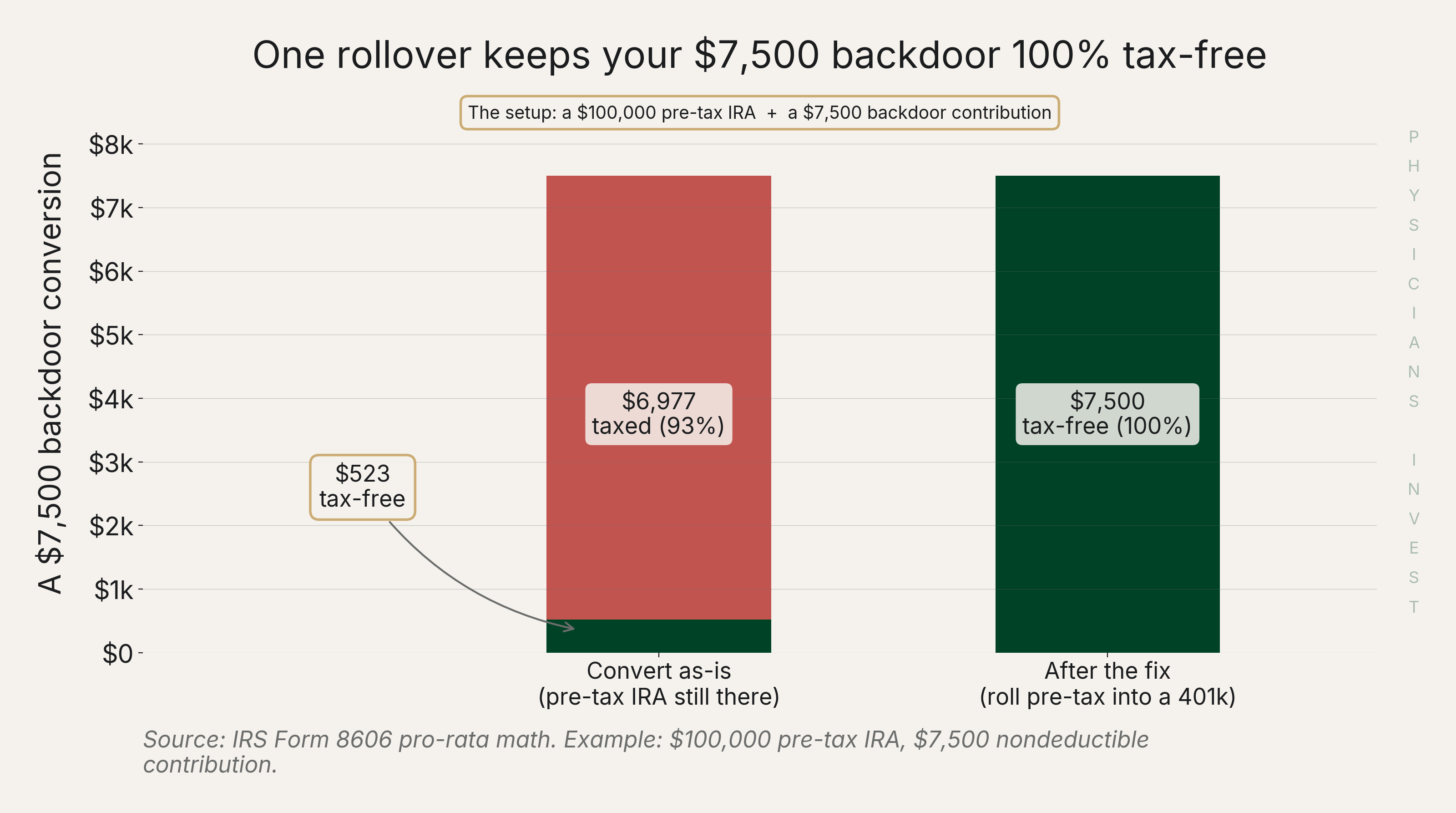

What about the "Pro-Rata Rule"? The aggregate pooling that we just mentioned drives the pro-rata rule which is the way the IRS calculates the tax implications. The IRS makes every dollar you convert the same blend as the whole pool of IRAs you control. That's confusing in sentence form so let's look at an example:

Let's assume $100,000 of pre-tax IRA money in the "aggregated" bucket and you want to make a $7,500 backdoor Roth IRA conversion. When you transfer dollars into the Traditional IRA and then convert those dollars immediately to a Roth IRA only about 7% comes out tax-free. The other 93% gets taxed as ordinary income because of the balance held in pre-tax IRA accounts. At a 35% bracket, that is roughly $2,400 of tax that could have been avoided. See the sequence below for the math:

- $100k existing Traditional IRA

- $7.5k backdoor Roth IRA conversion added to Traditional first and then converted to Roth IRA

- Total Traditional IRA dollars before conversion = $100k + $7.5k = $107.5k

- $7.5k / $107.5k = 0.0698 = 7%

- Therefore only 7% of your conversion is considered tax-free

- The other 93% you must pay ordinary income tax on at time of conversion

See the math graphically below:

Source: IRS Form 8606 pro-rata math

Source: IRS Form 8606 pro-rata math

It's not just Traditional IRAs that poison the conversion. Many physicians hold other pre-tax IRAs that all count toward the aggregation rule. For example, a SEP-IRA (Simplified Employee Pension IRA) from locums or moonlighting income, a rollover IRA from an old training-program 403(b), or a SIMPLE IRA (Savings Incentive Match Plan for Employees, another employer-sponsored pre-tax account) from a small practice all count towards the aggregate total. A meaningful balance in any one of those will create this massive tax issue.

The fix: empty the bucket to ZERO

The fix is straightforward but not necessarily easy for most people. You must get the pre-tax dollars out of every IRA and into some sort of employer plan (employer plans are ignored by the aggregation rule) in order to reduce your pre-tax balance across all IRA accounts to $0. If your employer doesn't allow rollovers then try to find a way to set up a Solo 401(k) for yourself using some side income, Solo 401(k)s still count as employer accounts even though you fully control it. Once that is accomplished, every after-tax dollar converted to Roth via the backdoor method is fully tax-free as long as your pre-tax IRA balance stays at $0 on December 31 and you file Form 8606 (the annual IRS tax form that tracks after-tax IRA contributions and calculates the taxable portion of any Roth conversion) each year.

Note: per the IRS Rollover Chart and IRC §408(d)(3), only pre-tax money is allowed to roll into a 401(k) or 403(b), so your after-tax basis is forced to stay behind in the IRA, but those are exactly the dollars you then convert to Roth tax-free anyway.

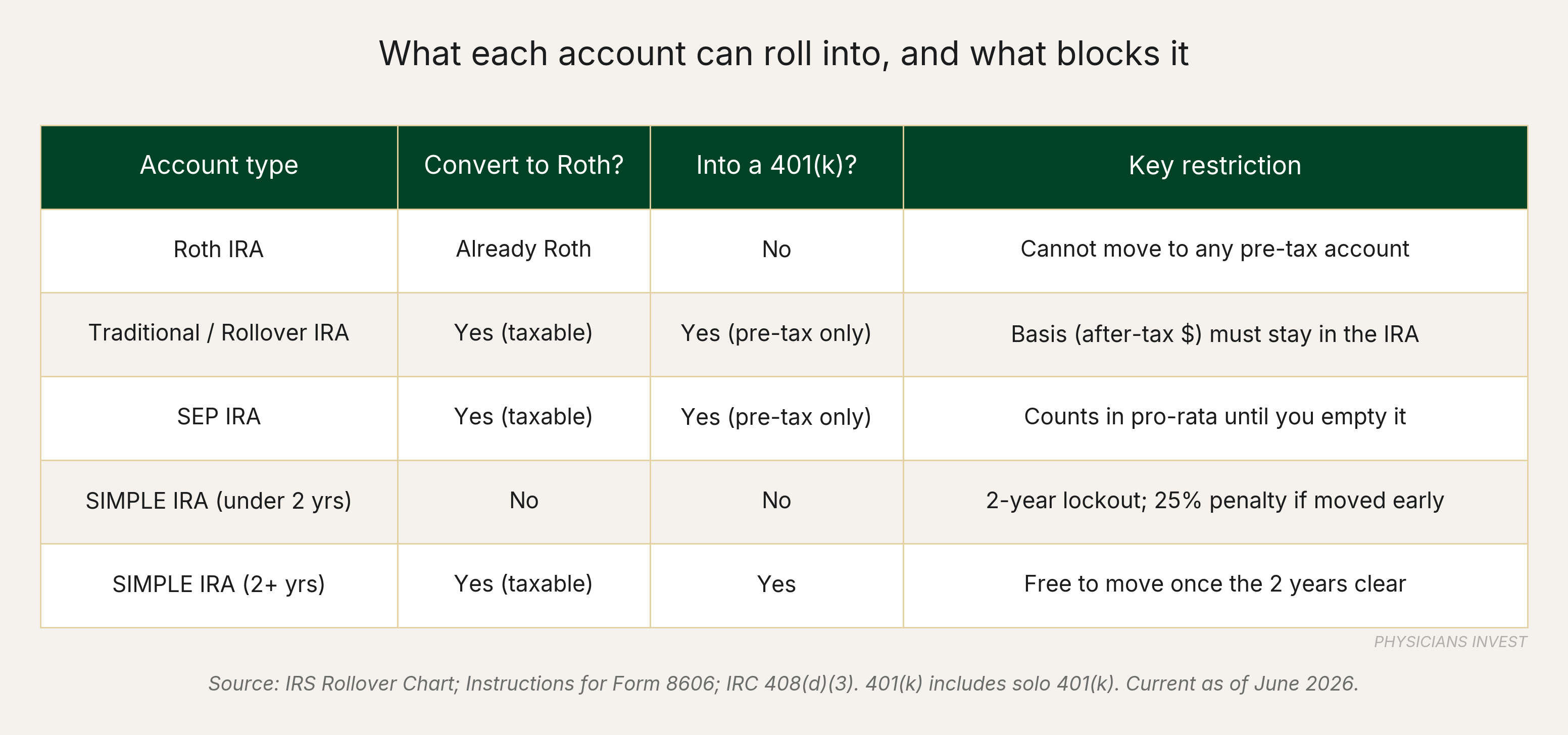

Below is a table showing some of the mechanics and restrictions by account type.

| Account type | Convert to Roth? | Into a 401(k)? | Key restriction |

|---|---|---|---|

| Roth IRA | Already Roth | No | Cannot move to any pre-tax account |

| Traditional / Rollover IRA | Yes (taxable) | Yes (pre-tax only) | Basis (after-tax $) must stay in the IRA |

| SEP IRA | Yes (taxable) | Yes (pre-tax only) | Counts in pro-rata until you empty it |

| SIMPLE IRA (under 2 yrs) | No | No | 2-year lockout; 25% penalty if moved early |

| SIMPLE IRA (2+ yrs) | Yes (taxable) | Yes | Free to move once the 2 years clear |

Source: IRS Rollover Chart; Instructions for Form 8606; IRC 408(d)(3). 401(k) includes solo 401(k). Current as of June 2026.

Source: IRS Rollover Chart; Instructions for Form 8606; IRC 408(d)(3)

Source: IRS Rollover Chart; Instructions for Form 8606; IRC 408(d)(3)

Some common cases:

- If you're a W-2 physician and your employer's 401(k) accepts incoming rollovers, roll your pre-tax IRAs into it

- If you have any 1099 income at all (moonlighting, locums, expert witness work, telehealth, a directorship), open a solo 401(k) and roll your pre-tax IRAs into it. That's the route we used ourselves once we realized the problem.

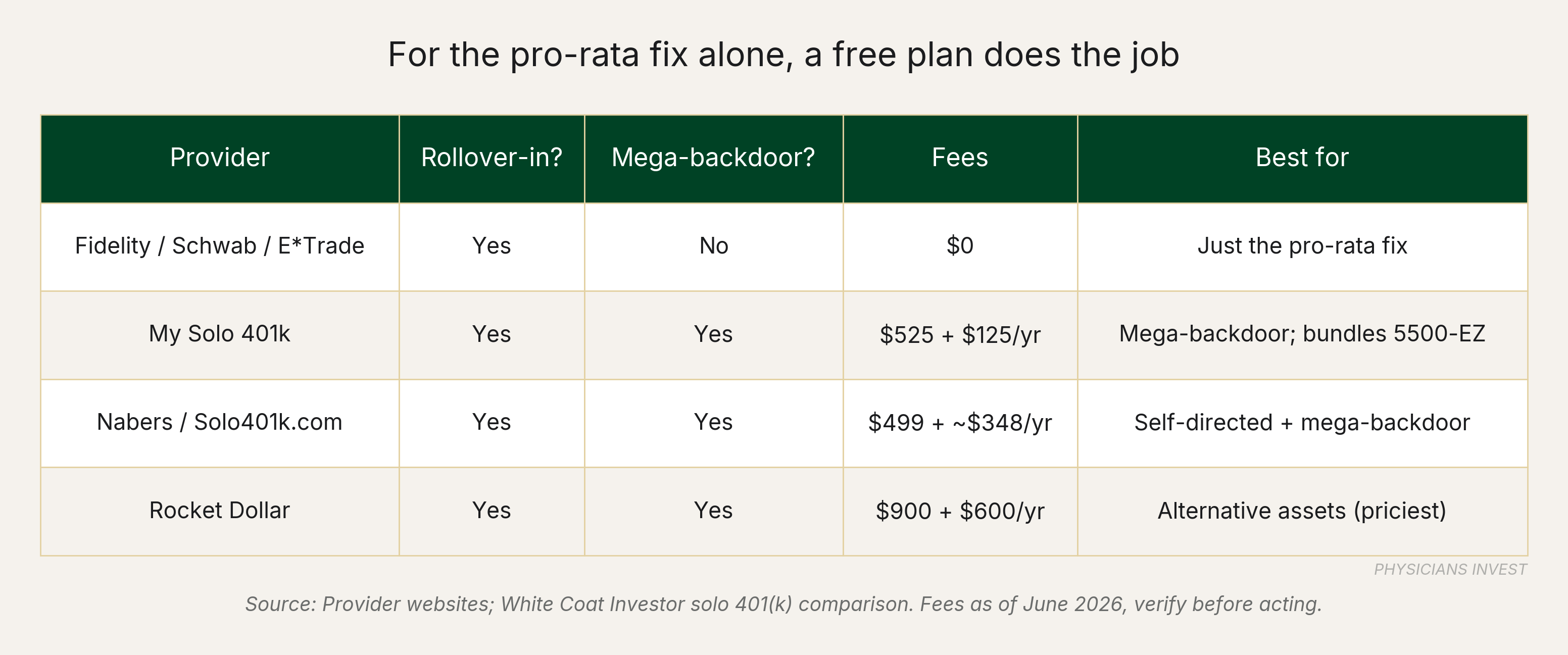

One caution. Solo 401(k)'s can introduce quite a bit of complexity. For most, using a platform like Schwab or Fidelity makes sense because it is low cost and paperwork will be handled mostly for you. For extra functionality, like mega-backdoor Roth capability (a strategy that lets you contribute after-tax dollars beyond the standard IRA limit inside a 401(k) and convert them to Roth), you will need to use a more tailored service such as My Solo401k. We can help guide you here if ever needed.

| Provider | Rollover-in? | Mega-backdoor? | Fees | Best for |

|---|---|---|---|---|

| Fidelity / Schwab / E*Trade | Yes | No | $0 | Just the pro-rata fix |

| My Solo 401k | Yes | Yes | $525 + $125/yr | Mega-backdoor; bundles 5500-EZ |

| Nabers / Solo401k.com | Yes | Yes | $499 + ~$348/yr | Self-directed + mega-backdoor |

| Rocket Dollar | Yes | Yes | $900 + $600/yr | Alternative assets (priciest) |

Fees as of June 2026. Confirm current pricing before opening an account.

Source: Provider websites. Fees as of June 2026, verify before acting.

Source: Provider websites. Fees as of June 2026, verify before acting.

Tip: never use a SEP-IRA for your side income. It recreates the very pro-rata problem you're trying to escape.

The big legacy balance is a different problem

A completely different problem with IRAs comes up mostly for late career or early retired individuals. If you're sitting on a $500,000 or seven-figure traditional IRA and you want it in a Roth account to protect from future tax and required distributions (RMDs, which force taxable withdrawals starting at age 73), run the decisions below in order:

-

Separate the goals. Rolling your Traditional IRA balance into a Solo 401(k) clears the pro-rata path, but the money is still pre-tax. Getting it into Roth means converting and paying tax. The only game is converting at the lowest tax rate year that you can.

-

Will you be in a top bracket for all foreseeable future years? Big required withdrawals and heavy passive income may keep you in your Traditional IRAs no matter what and converting may hurt you. Figuring out the math requires a detailed Excel model or advisor software.

-

Are you charitably inclined? A traditional IRA is ideal for qualified charitable distributions at age 70½, or QCDs (direct gifts from your IRA to a charity that satisfy your required withdrawal but stay out of your taxable income), because you can give to charity tax-free. No need to convert if you are using distributions for charity anyway.

-

Convert to Roth IRA in your low-income years. A gap year, a sabbatical, or the early-retirement window before withdrawals and Social Security start (retire at 62 and withdrawals beginning at 73 give a decade to convert chunk by chunk). Watch the cliffs: Medicare premium surcharges (IRMAA, income-related adjustments that kick in above certain thresholds, with a 2-year lookback on your income), the 3.8% net investment income surtax (which applies to passive income above $200K single / $250K married), and state tax. Wait until after a move from a high-tax state to a no-tax one to do a big conversion.

These decisions get complicated fast, so model them with a CPA before pulling the trigger. We're building a full decision flowchart for this late career scenario. For now, the order above is the playbook.

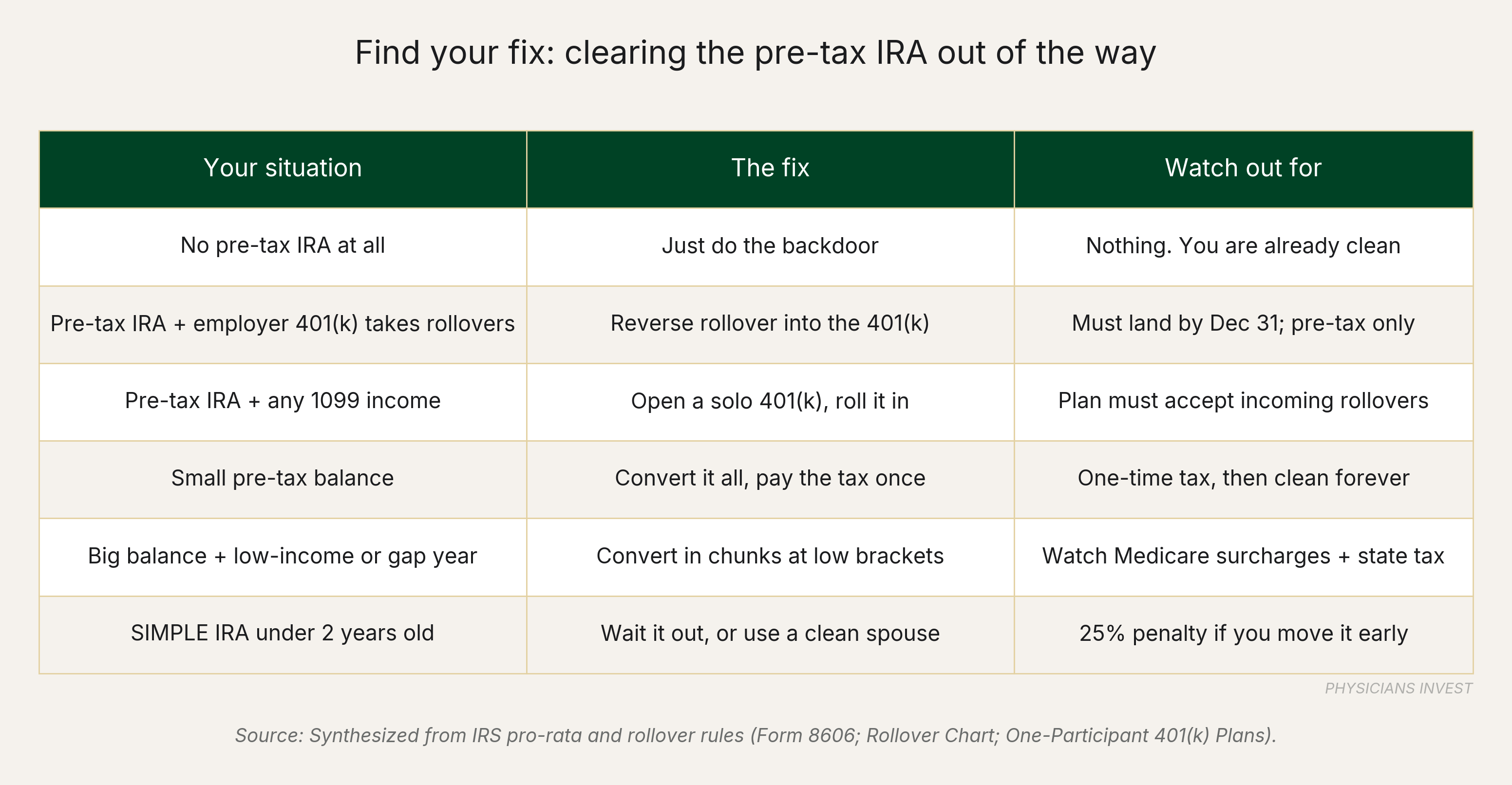

The Move

Find your situation in the chart below to have a good understanding of your path forward. Remember, the goal is always the same: a $0 pre-tax IRA balance on December 31 in any year you make backdoor Roth IRA contributions.

Source: IRS Form 8606; Rollover Chart; One-Participant 401(k) Plans

Source: IRS Form 8606; Rollover Chart; One-Participant 401(k) Plans

-

Add up every traditional, rollover, SEP, and SIMPLE IRA. If it's $0, you're clear. Good to do the backdoor Roth IRA conversion.

-

If there's any pre-tax balance, roll it into an employer 401(k) (if allowed by employer plan) or a Solo 401(k) (requires 1099 income). The roll must land by December 31, so plan to execute beginning of December or earlier in the year.

-

Once step 2 is done, contribute $7,500 nondeductible (just means after-tax) to a Traditional IRA and convert promptly to a Roth IRA. File Form 8606 every year.

-

Are you married? Run this same playbook per spouse. IRAs of one spouse don't block a clean backdoor on the other. IRA stands for "Individual Retirement Account" and each spouse is considered a separate "individual" even if you file jointly.

-

Do you hold a big legacy IRA that you want in Roth? Convert it in your lowest-income years and chunk by chunk to not trip higher tax brackets.

Sources

Data

- IRS Notice 2025-67 -- 2026 IRA and Roth phase-out limits -- 2026 contribution limit ($7,500) and Roth MAGI phase-outs ($168K single / $252K MFJ); issued Nov 2025

- IRS IR-2025-111 -- 2026 retirement contribution limits -- confirms IRA limit $7,500 and 401(k) deferral $24,500 for 2026

- Medscape 2025 Physician Compensation Report -- average physician total compensation ~$376,000 (2024 earnings)

Policy / Rules

- IRS Instructions for Form 8606 -- pro-rata rule mechanics, aggregation of all traditional/SEP/SIMPLE IRAs, Dec 31 measurement date (line 6), annual Form 8606 filing requirement

- IRS Rollover Chart -- confirms pre-tax IRA to 401(k)/403(b) rollover is permitted; after-tax basis cannot roll to employer plan (IRC §408(d)(3))

- IRS One-Participant 401(k) Plans -- solo 401(k) eligibility: requires self-employment income, no full-time common-law employees

- IRS SIMPLE IRA withdrawal and transfer rules -- 2-year lockout; 25% early-distribution penalty if SIMPLE IRA moved within 2 years of first participation

- IRS Required Minimum Distribution FAQs -- RMD age 73 for traditional IRAs

- IRS Qualified Charitable Distributions -- QCDs available at age 70½ from traditional IRAs